Is the settlement of a lawsuit taxable?

The general rule of taxability for amounts received from the settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61, which states that all income is taxable “unless a specific exception exists from whatever source derived unless exempted by another section of the code.”

Are personal injury settlements taxable in New York?

The IRS does NOT tax settlement awards from personal injury lawsuits if these cases demonstrate “observable bodily harm”. So, if the injuries are visible, the IRS considers settlement money that was awarded because of those injuries, tax-free.

Are damages from a personal injury claim taxable?

In general, damages from a physical injury are not considered taxable income. However, if you’ve already deducted, say, your medical expenses from your injury, your damages will be taxable. You can’t get the same tax break twice.

Is representation in a civil lawsuit taxable?

Representation in civil lawsuits doesn’t come cheap. In the best-case scenario, you’ll be awarded money at the end of either a trial or a settlement process. But before you blow your settlement, keep in mind that it may be taxable income in the eyes of the IRS.

What type of legal settlements are not taxable?

Settlement money and damages collected from a lawsuit are considered income, which means the IRS will generally tax that money. However, personal injury settlements are an exception (most notably: car accident settlements and slip and fall settlements are nontaxable).

How can I avoid paying taxes on a settlement?

How to Avoid Paying Taxes on a Lawsuit SettlementPhysical injury or sickness. ... Emotional distress may be taxable. ... Medical expenses. ... Punitive damages are taxable. ... Contingency fees may be taxable. ... Negotiate the amount of the 1099 income before you finalize the settlement. ... Allocate damages to reduce taxes.More items...•

Are ADA awards taxable?

IRS Says Disability Discrimination Award Was Taxable as Income. While in court to enter the settlement, Ms. Beckett asked her civil court judge whether the $19,000 disability discrimination award was taxable as income. The judge told her no, because the lawsuit was based on her seizures.

Do I have to report personal injury settlement to IRS?

The compensation you receive for your physical pain and suffering arising from your physical injuries is not considered to be taxable and does not need to be reported to the IRS or the State of California.

What do I do if I have a large settlement?

– What do I do with a large settlement check?Pay off any debt: If you have any debt, this can be a great way to pay off all or as much of your debt as you want.Create an emergency fund: If you don't have an emergency fund, using some of your settlement money to create one is a great idea.More items...•

How can you avoid paying taxes on a large sum of money?

Research the taxes you might owe to the IRS on any sum you receive as a windfall. You can lower a sizeable amount of your taxable income in a number of different ways. Fund an IRA or an HSA to help lower your annual tax bill. Consider selling your stocks at a loss to lower your tax liability.

Can the IRS take my settlement money?

If you have back taxes, yes—the IRS MIGHT take a portion of your personal injury settlement. If the IRS already has a lien on your personal property, it could potentially take your settlement as payment for your unpaid taxes behind that federal tax lien if you deposit the compensation into your bank account.

Can you deduct lawsuit settlement payments?

This means that, generally, monies paid pursuant to a court order or settlement agreement with a government entity are not deductible. However, the 2017 Tax Cuts and Jobs Act (TCJA) amended § 162(f) to allow deductions for payments for restitution, remediation, or those paid to come into compliance with a law.

Are damages for emotional distress taxable?

Compensation for emotional distress is generally taxable. However, if there is a physical injury that led to emotional distress and the physical injury was the origin of the claim, then both the physical injury and emotional stress claim should be tax free.

What is the tax rate on settlement money?

It's Usually “Ordinary Income” As of 2018, you're taxed at the rate of 24 percent on income over $82,500 if you're single. If you have taxable income of $82,499 and you receive $100,000 in lawsuit money, all that lawsuit money would be taxed at 24 percent.

Are settlements tax deductible?

Generally, if a claim arises from acts performed by a taxpayer in the ordinary course of its business operations, settlement payments and payments made pursuant to court judgments related to the claim are deductible under section 162.

Do you get a 1099 for insurance settlement?

If you do have to pay taxes on an insurance claim, you'll receive a 1099 form to help you file.

What is a tax-free structured settlement annuity?

A structured settlement annuity (“structured settlement”) allows a claimant to receive all or a portion of a personal injury, wrongful death, or workers' compensation settlement in a series of income tax-free periodic payments.

Are settlement annuities taxable?

A structured settlement annuity offers flexible payment design, guaranteed payments, and no overhead or annual fees. Both the principal and growth are income tax-free if the money used to purchase the annuity came from a personal injury, workers' compensation, or wrongful death case.

Why are lost wages taxable?

Lost wages are considered taxable because wages are income that would have been taxed if it were received without interruption. Not only will income tax be added, but these wages are also subject to social security taxes and Medicare tax.

Is a car accident settlement in West Palm Beach taxable?

Any of the major claims a West Palm Beach car accident lawyer settles will almost always be nontaxable. Cases handled by personal injury lawyers are an exception to any settlement awards that considered income.

Does the IRS collect taxes on lawsuits?

Most money awarded as a result of a lawsuit claim will be subject to taxes. The IRS is a governing body that exists to collect taxes, and that’s exactly what they do best: they collect taxes!

Is a lawsuit settlement considered income?

Settlement money and damages collected from a lawsuit are considered income, which means the IRS will generally tax that money, although personal injury settlements are an exception ( most notably: car accident settlement and slip and fall settlements are nontaxable). Lawsuit settlements and damages are generally separated into two categories: ...

Is a lawsuit settlement taxable?

Lawsuit settlements and damages are generally separated into two categories: taxable and nontaxable. There are exceptions to every rule and each lawsuit claim is unique. Again, we suggest seeking advice from an account where possible.

Can contingency fees be taxed?

Remember, if a lawyer chooses to work for contingency fees (where the attorney collects fees after winning a case), those fees can be taxed. However, that is not the case with car accident cases or many other personal injury cases like slip and fall or workers compensation [2]. Those contingency fees will not be taxed!

Is emotional distress taxable?

Emotional Distress Awards Are Nontaxable. Any settlement money received for emotional distress is nontaxable if and only if the distress or anguish originated from the physical injury or sickness caused by the accident.

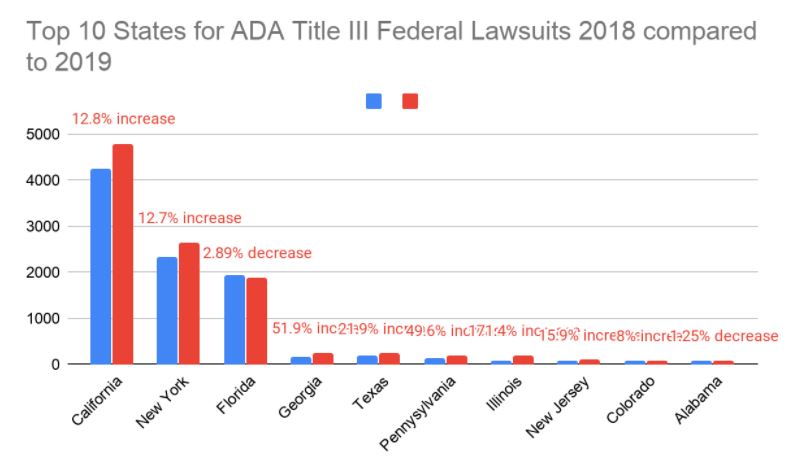

Why are ADA lawsuits not taxable?

A surprising number of plaintiffs in ADA/accessibility lawsuits claim that the payments made to settle those lawsuits are not their income, because they are paid to another individual or firm. Despite receiving thousands of dollars from each suit they file, some do not report this income as taxable because they do not want to lose income-related disability benefits, while others seek waivers of court filing fees and service costs, etc. Of course, taxpayers pay more whenever those who are required to report income fail to do so.

Who is required to report ADA settlement?

If you have been sued in an ADA/accessibility lawsuit, you may have a duty to report the settlement payment to both the plaintiff who sued you and their attorney (on separate IRS Form 1099's), as well as any other parties who have received payments in connection with the lawsuit, such as organizations, experts and other service providers.

Do you need to file a 1099 for a lawsuit?

Many plaintiffs have used a variety of tactics to discourage defendants from reporting the income from these lawsuits as required by law (generally, a 1099 should be issued to both the plaintiff and the attorney representing them, for the full amount of the settlement payment, but always consult qualified tax and legal advisors to make sure).

Is ADA claim reportable?

Generally, it is our understanding that the financial proceeds of ADA/accessibility lawsuits are reportable to the human plaintiffs who are making the claims, even if some organization is included in the lawsuit or receives the funds; basically, since only a human being is entitled to claim discrimination, it appears that the profitable discrimination claims are immediately vested in them and the income relating to those claims will generally be attributable to them, even if they make complex arrangements for the checks to be paid to someone else.

What is the tax rule for settlements?

Tax Implications of Settlements and Judgments. The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code. IRC Section 104 provides an exclusion ...

What is employment related lawsuit?

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example lost wages, business income and benefits, are not excludable form gross income unless a personal physical injury caused such loss.

What is the exception to gross income?

For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury.

Is emotional distress excludable from gross income?

96-65 - Under current Section 104 (a) (2) of the Code, back pay and damages for emotional distress received to satisfy a claim for disparate treatment employment discrimination under Title VII of the 1964 Civil Rights Act are not excludable from gross income . Under former Section 104 (a) (2), back pay received to satisfy such a claim was not excludable from gross income, but damages received for emotional distress are excludable. Rev. Rul. 72-342, 84-92, and 93-88 obsoleted. Notice 95-45 superseded. Rev. Proc. 96-3 modified.

Is a settlement agreement taxable?

In some cases, a tax provision in the settlement agreement characterizing the payment can result in their exclusion from taxable income. The IRS is reluctant to override the intent of the parties. If the settlement agreement is silent as to whether the damages are taxable, the IRS will look to the intent of the payor to characterize the payments and determine the Form 1099 reporting requirements.

Is emotional distress taxable?

Damages received for non-physical injury such as emotional distress, defamation and humiliation, although generally includable in gross income, are not subject to Federal employment taxes. Emotional distress recovery must be on account of (attributed to) personal physical injuries or sickness unless the amount is for reimbursement ...

Does gross income include damages?

IRC Section 104 explains that gross income does not include damages received on account of personal physical injuries and physical injuries.

Who pays attorney fees and court costs?

The attorney fees and court costs may be paid by you or on your behalf in connection with the claim for unlawful discrimination, the claim against the United States government, or the claim under section 1862 (b) (3) (A) of the Social Security Act.

Is attorney fees included in gross income?

Attorney fees and costs (including contingent fees) where the underlying recovery is included in gross income. Do not include in your income compensatory damages for personal physical injury or physical sickness (whether received in a lump sum or installments).

What percentage of a personal injury settlement is taxed?

If your attorney represents you in a personal injury lawsuit on a contingency fee basis, you may pay taxes on 100 percent of the money recovered by you and your attorney.

What is a settlement in a lawsuit?

Types of Lawsuit Settlements. As to terminology, a judgment refers to a formal court resolution of a dispute, in which the court may order one party to pay money damages to another. Settlement refers to a mutual agreement between litigants. Settlements are a different process than adjudication by a court, binding arbitration, ...

How to exclude a payment from income?

To exclude a payment from income on account of physical illness or injury, keep all evidence related to the claim and any proof that the defendant was aware of the claim and considered it in making payment. Medical records can help establish that the defendant caused the injury or caused it to worsen. Declarations from the treating doctors, as well as medical experts, can prove helpful. All of this evidence is useful when dealing with an IRS query or audit.

What is the purpose of a settlement agreement?

Part of your settlement agreement provides that the at-fault party pays you compensation for your losses. You can’t wait to receive money to cover the cost of your injuries and make plans for the future, but do you have to pay taxes on the money you receive ...

Do you have to pay taxes on a personal injury settlement?

Every case is different, but depending on the nature of the claim and other circumstances, you may have to pay taxes on the settlement payout that you receive. Here are some general tax guidelines; however you may need to consult a tax expert regarding your case because the IRS has determined that lawsuit settlements are taxable under certain, complicated circumstances. Read on for more information regarding the tax requirements of personal injury settlements.

Is settlement of lawsuits taxable?

The general rule of taxability for amounts received from the settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61, which states that all income is taxable “unless a specific exception exists from whatever source derived unless exempt ed by another section of the code.”.

Is a recovery taxable?

If your recovery is taxable, the situation is more complicated. For example, if you settle a lawsuit for emotional distress. Your settlement awards you $200,000. If your attorney fee is $80,000, you take home $120,000. Logically, you might think that you have $120,000 of income to claim on your taxes. However, the IRS says you must claim the entire $200,000.

What was the settlement agreement between the medical center and the taxpayer?

Pursuant to the terms of the settlement agreement, the medical center agreed to pay the taxpayer $350,000 “as noneconomic damages and not as wages or other income.” In 2005, the taxpayer received a $34,000 payment from the medical center and treated it as nontaxable under Section 104 (a) (2). The IRS examined the return and disagreed that the $34,000 payment fell under the exclusion of Section 104 (a) (2).

What did the taxpayer claim against the medical center?

The taxpayer filed a lawsuit against the medical center and two of its employees. In his complaint in federal district court, the taxpayer alleged that the medical center had violated the American with Disabilities Act of 1990 (ADA) by failing to accommodate his severe coronary artery disease. He also asserted common law claims of intentional infliction of emotional distress and invasion of privacy by two employees who worked at the medical center. His ADA claims were subsequently dismissed as untimely, resulting in the taxpayer filing a separate complaint in Maryland against the medical center and the two employees alleging the same common law claims that he had asserted in the federal suit.

Why is the $16,933 settlement ambiguous?

The taxpayer contended that the payment should be excluded under Section 104 (a) (2) because she received the payment due to her physical injuries and/or physical sickness associated with MS. Conversely, the IRS argued that the settlement payment was ambiguous— i.e., that the payor’s intent could not be determined and therefore the payment should be presumed to be taxable as ordinary income.

Why are federal taxes a mere afterthought?

Indeed, in most cases, federal taxes are a mere afterthought because the taxpayer wants to end the litigation and receive the settlement payment as quickly as possible. However, with the highest marginal income tax rates hovering at 37%, this may be a huge mistake. As discussed above, federal courts and the IRS will generally respect allocations made in a settlement agreement, provided the terms of the agreement are clear regarding the allocation. If the taxpayer’s attorney can have opposing counsel agree on an express allocation of the payment to Section 104 (a) (2) damages and not emotional distress, the taxpayer can generally walk away with a better chance of more of a recovery.

Why did the IRS settle the $16,933?

Based on the separate payments and the information reporting of the nonprofit, the Tax Court concluded that an inference could be made that the payment at issue was due to the taxpayer’s physical injuries and/or physical sickness. More specifically, the Tax Court concluded:

What is proper federal tax treatment?

The proper federal tax treatment for any given settlement payment is something of an enigma. Generally, federal courts (and thus, the IRS) respect the terms of a settlement agreement if the terms are clear and the parties expressly allocate the settlement payment or payments to one or more of the underlying claims or causes of action at issue. But, if one or more of these requirements are not present, federal courts are left searching through other evidence in an attempt to determine the payor’s intent, which, absent an express allocation, generally governs the tax characterization of the payment.

Can opposing counsel refuse to agree on an allocation?

In some cases, opposing counsel may flat-out refuse to agree on an allocation. Here, it may be helpful for the taxpayer to engage a tax attorney to: (1) better explain to opposing counsel why the allocation should be made in this manner; or (2) alternatively, to have the tax attorney tinker with the settlement agreement language to put the taxpayer in the best possible position for later contending on a tax return that the payments represent non-taxable Section 104 (a) (2) damages and not taxable emotional distress damages. Moreover, tax attorneys can work with opposing counsel in ensuring that proper information returns ( e.g., Forms 1099, etc.) are either issued or not issued to avoid future headaches come tax reporting time.

What happens if you get a settlement from a lawsuit?

You could receive damages in recognition of a physical injury, damages from a non-physical injury or punitive damages stemming from the defendant’s conduct. In the tax year that you receive your settlement it might be a good idea to hire a tax accountant, even if you usually do your taxes yourself online. The IRS rules around which parts of a lawsuit settlement are taxable can get complicated.

What to do if you have already spent your settlement?

If you’ve already spent your settlement by the time tax season comes along, you’ll have to dip into your savings or borrow money to pay your tax bill. To avoid that situation, it may be a good idea to consult a financial advisor. SmartAsset’s free toolmatches you with financial advisors in your area in 5 minutes.

What can a financial advisor do for a lawsuit?

A financial advisor can help you optimize a tax strategy for your lawsuit settlement. Speak with a financial advisor today.

Can you get damages for a non-physical injury?

You could receive damages in recognition of a physical injury, damages from a non-physical injury or punitive damages stemming from the defendant’s conduct. In the tax year that you receive your settlement it might be a good idea to hire a tax accountant, even if you usually do your taxes yourself online.

Is a lawsuit settlement taxable?

The tax liability for recipients of lawsuit settlements depends on the type of settlement. In general, damages from a physical injury are not considered taxable income. However, if you’ve already deducted, say, your medical expenses from your injury, your damages will be taxable. You can’t get the same tax break twice.

Is representation in a civil lawsuit taxable?

Representation in civil lawsuits doesn’t come cheap. In the best-case scenario, you’ll be awarded money at the end of either a trial or a settlement process. But before you blow your settlement, keep in mind that it may be taxable income in the eyes of the IRS. Here’s what you should know about taxes on lawsuit settlements.

Is emotional distress taxable?

Although emotional distress damages are generally taxable, an exception arises if the emotional distress stems from a physical injury or manifests in physical symptoms for which you seek treatment. In most cases, punitive damages are taxable, as are back pay and interest on unpaid money.

What does it mean to pay taxes on a $100,000 case?

In a $100,000 case, that means paying tax on $100,000, even if $40,000 goes to the lawyer. The new law generally does not impact physical injury cases with no punitive damages. It also should not impact plaintiffs suing their employers, although there are new wrinkles in sexual harassment cases. Here are five rules to know.

Can you sue a building contractor for damages to your condo?

But if you sue for damage to your condo by a negligent building contractor, your damages may not be income. You may be able to treat the recovery as a reduction in your purchase price of the condo. The rules are full of exceptions and nuances, so be careful, how settlement awards are taxed, especially post-tax reform. 2.

Do you have to pay taxes on a lawsuit?

Many plaintiffs win or settle a lawsuit and are surprised they have to pay taxes. Some don't realize it until tax time the following year when IRS Forms 1099 arrive in the mail. A little tax planning, especially before you settle, goes a long way. It's even more important now with higher taxes on lawsuit settlements under the recently passed tax reform law . Many plaintiffs are taxed on their attorney fees too, even if their lawyer takes 40% off the top. In a $100,000 case, that means paying tax on $100,000, even if $40,000 goes to the lawyer. The new law generally does not impact physical injury cases with no punitive damages. It also should not impact plaintiffs suing their employers, although there are new wrinkles in sexual harassment cases. Here are five rules to know.

Is there a deduction for legal fees?

How about deducting the legal fees? In 2004, Congress enacted an above the line deduction for legal fees in employment claims and certain whistleblower claims. That deduction still remains, but outside these two areas, there's big trouble. in the big tax bill passed at the end of 2017, there's a new tax on litigation settlements, no deduction for legal fees. No tax deduction for legal fees comes as a bizarre and unpleasant surprise. Tax advice early, before the case settles and the settlement agreement is signed, is essential.

Is attorney fees taxable?

4. Attorney fees are a tax trap. If you are the plaintiff and use a contingent fee lawyer, you’ll usually be treated (for tax purposes) as receiving 100% of the money recovered by you and your attorney, even if the defendant pays your lawyer directly his contingent fee cut. If your case is fully nontaxable (say an auto accident in which you’re injured), that shouldn't cause any tax problems. But if your recovery is taxable, watch out. Say you settle a suit for intentional infliction of emotional distress against your neighbor for $100,000, and your lawyer keeps $40,000. You might think you’d have $60,000 of income. Instead, you’ll have $100,000 of income. In 2005, the U.S. Supreme Court held in Commissioner v. Banks, that plaintiffs generally have income equal to 100% of their recoveries. even if their lawyers take a share.

Is $5 million taxable?

The $5 million is fully taxable, and you can have trouble deducting your attorney fees! The same occurs with interest. You might receive a tax-free settlement or judgment, but pre-judgment or post-judgment interest is always taxable (and can produce attorney fee problems).

Is punitive damages taxable?

Tax advice early, before the case settles and the settlement agreement is signed, is essential. 5. Punitive damages and interest are always taxable. If you are injured in a car crash and get $50,000 in compensatory damages and $5 million in punitive damages, the former is tax-free.

IRC Section and Treas. Regulation

- IRC Section 61explains that all amounts from any source are included in gross income unless a specific exception exists. For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury. IRC Section 104explains that gross income does not include damages received on account of personal phys…

Resources

- CC PMTA 2009-035 – October 22, 2008PDFIncome and Employment Tax Consequences and Proper Reporting of Employment-Related Judgments and Settlements Publication 4345, Settlements – TaxabilityPDFThis publication will be used to educate taxpayers of tax implications when they receive a settlement check (award) from a class action lawsuit. Rev. Rul. 85-97 - The …

Analysis

- Awards and settlements can be divided into two distinct groups to determine whether the payments are taxable or non-taxable. The first group includes claims relating to physical injuries, and the second group is for claims relating to non-physical injuries. Within these two groups, the claims usually fall into three categories: 1. Actual damages re...

Issue Indicators Or Audit Tips

- Research public sources that would indicate that the taxpayer has been party to suits or claims. Interview the taxpayer to determine whether the taxpayer provided any type of settlement payment to any of their employees (past or present).