If a judgment or settlement agreement involving beneficial interests in a decedent’s estate is respected for tax purposes, estate assets passing to the various parties to the dispute will generally be treated as transfers by decedent.

Do you have to pay taxes on a settlement?

Tax Implications of Settlements and Judgments The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code.

What is the difference between the estate tax and income tax?

The estate tax is effectively a one-time tax. On the other hand, the income tax is assessed on the earnings (net of allowable deductions) of the estate or trust. Income and deductions up to the date of death are reported in the deceased person’s (“decedent”) final individual income tax return.

What are the tax obligations of estates?

Estates, like individuals, must file income tax forms. They may owe taxes, too, often in interest payments on accounts. The estate may pay the taxes due or distribute the taxable income to the heirs.

What happens if an estate does not pay taxes?

Also, in instances where the estate has failed to pay income tax prior to distribution, the U.S. government may attach limited beneficiary taxes to distributions. As is true for an individual, an estate must use an income tax return to report an income.

What type of settlements are not taxable?

Settlement money and damages collected from a lawsuit are considered income, which means the IRS will generally tax that money. However, personal injury settlements are an exception (most notably: car accident settlements and slip and fall settlements are nontaxable).

Do you have to report inheritance money to IRS?

Inheritances are not considered income for federal tax purposes, whether you inherit cash, investments or property. However, any subsequent earnings on the inherited assets are taxable, unless it comes from a tax-free source.

How much can you inherit without paying federal taxes?

There is no federal inheritance tax—that is, a tax on the sum of assets an individual receives from a deceased person. However, a federal estate tax applies to estates larger than $11.7 million for 2021 and $12.06 million for 2022. The tax is assessed only on the portion of an estate that exceeds those amounts.

Is income from an estate taxable?

There are two kinds of taxes owed by an estate: One on the transfer of assets from the decedent to their beneficiaries and heirs (the estate tax), and another on income generated by assets of the decedent's estate (the income tax).

Do I have to pay taxes on a $10 000 inheritance?

For example, if you only inherited $10,000, you may be exempt and not have to pay a tax. Additionally, if you are married to the person who passed away, you will not have to pay an inheritance tax. However, if these exceptions do not apply, you will have to pay an inheritance tax.

Do beneficiaries pay taxes on inherited money?

Beneficiaries generally don't have to pay income tax on money or other property they inherit, with the common exception of money withdrawn from an inherited retirement account (IRA or 401(k) plan). The good news for people who inherit money or other property is that they usually don't have to pay income tax on it.

Is there a difference between estate tax and inheritance tax?

estate taxes. Inheritance tax and estate tax are two different things. Inheritance tax is what the beneficiary — the person who inherited the wealth — must pay when they receive it. Estate tax is the amount that's taken out of someone's estate upon their death.

Which states have an inheritance tax?

But 17 states and the District of Columbia may tax your estate, an inheritance or both, according to the Tax Foundation. Eleven states have only an estate tax: Connecticut, Hawaii, Illinois, Maine, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont and Washington. Washington, D.C. does, as well.

Which states have estate taxes?

The following are the 13 states that levy state estate tax and their threshold minimums: Connecticut ($3,600,000), District of Columbia ($5,600,000), Hawaii ($5,500,000), Illinois ($4,000,000), Maine ($5,600,000), Maryland ($5,000,000), Massachusetts ($1,000,000), Minnesota ($2,700,000), New York ($5,000,000), Oregon ...

How much can you inherit without paying taxes in 2022?

$12.06 millionIn 2022, an individual can leave $12.06 million to heirs and pay no federal estate or gift tax, while a married couple can shield $24.12 million. For a couple who already maxed out lifetime gifts, the new higher exemption means that there's room for them to give away another $720,000 in 2022.

Who pays the estate tax?

The executor, administrator, beneficiaries or heirs are the ones paying for the estate taxes. Transferring property to heirs or beneficiaries will not be executed unless the estate tax is paid. 1.

How do I close an estate with the IRS?

For those who wish to continue to receive estate tax closing letters, estates and their authorized representatives may call the IRS at (866) 699-4083 to request an estate tax closing letter no earlier than four months after the filing of the estate tax return.

How does the IRS know if you inherited money?

These documents can include the will, death certificate, transfer of ownership forms and letters from the estate executor or probate court. Contact your bank or financial institution and request copies of deposited inheritance check or authorization of the direct deposit.

Do you get a 1099 for inheritance?

This means that when the beneficiary withdraws those monies from the accounts, the beneficiary will receive a 1099 from the company administering the plan and must report that income on their income tax return (and must pay income taxes on the sum).

How much can you inherit without paying taxes in 2022?

$12.06 millionIn 2022, an individual can leave $12.06 million to heirs and pay no federal estate or gift tax, while a married couple can shield $24.12 million. For a couple who already maxed out lifetime gifts, the new higher exemption means that there's room for them to give away another $720,000 in 2022.

How can I avoid paying taxes on inheritance?

8 ways to avoid inheritance taxStart giving gifts now. ... Write a will. ... Use the alternate valuation date. ... Put everything into a trust. ... Take out a life insurance policy. ... Set up a family limited partnership. ... Move to a state that doesn't have an estate or inheritance tax. ... Donate to charity.

Why No Estate Tax?

The history of the estate tax in the U.S. has been fraught with controversy. It was often derided by its opponents as a "death tax." 6

What happens if the executor fails to pay taxes?

If the estate executor has failed to pay income tax prior to distributing the inheritance, the beneficiaries may owe some tax. The estate may pay the taxes due or distribute the taxable income to the heirs.

How many states have inheritance tax in 2021?

As of 2021, 17 states have an estate or inheritance tax. Five states have only an inheritance tax, and these are Iowa, Kentucky, Nebraska, New Jersey, and Pennsylvania. However, none of those states taxes inheritances that go to the spouse or children of the deceased.

How much is estate tax in 2021?

As of 2021, the estate tax, which the estate itself pays, is levied only on amounts above $11.7 million. 1 The amount for 2020 is $11.58 million.

How to avoid estate tax?

One of the more popular methods of avoiding any estate tax is to give away portions of the estate in advance to family members. Another is to create an irrevocable life insurance trust. 9

How many Americans are subject to estate tax?

It is estimated that about 2,000 Americans a year are subject to estate taxes under the latest law, and they generally employ accountants who are adept at finding ways to avoid or minimize the estate tax.

Do beneficiaries owe taxes on inheritance?

While beneficiaries don't owe income tax on money they inherit, if their inheritance includes an individual retirement account (IRA) they will have to take distributions from it over a certain period and, if it is a traditional IRA rather than a Roth, pay income tax on that money. The IRS explains the rules in Publication 590-B .

What is the tax rule for settlements?

Tax Implications of Settlements and Judgments. The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code. IRC Section 104 provides an exclusion ...

What is employment related lawsuit?

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example lost wages, business income and benefits, are not excludable form gross income unless a personal physical injury caused such loss.

What is the exception to gross income?

For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury.

Is emotional distress excludable from gross income?

96-65 - Under current Section 104 (a) (2) of the Code, back pay and damages for emotional distress received to satisfy a claim for disparate treatment employment discrimination under Title VII of the 1964 Civil Rights Act are not excludable from gross income . Under former Section 104 (a) (2), back pay received to satisfy such a claim was not excludable from gross income, but damages received for emotional distress are excludable. Rev. Rul. 72-342, 84-92, and 93-88 obsoleted. Notice 95-45 superseded. Rev. Proc. 96-3 modified.

Is a settlement agreement taxable?

In some cases, a tax provision in the settlement agreement characterizing the payment can result in their exclusion from taxable income. The IRS is reluctant to override the intent of the parties. If the settlement agreement is silent as to whether the damages are taxable, the IRS will look to the intent of the payor to characterize the payments and determine the Form 1099 reporting requirements.

Is emotional distress taxable?

Damages received for non-physical injury such as emotional distress, defamation and humiliation, although generally includable in gross income, are not subject to Federal employment taxes. Emotional distress recovery must be on account of (attributed to) personal physical injuries or sickness unless the amount is for reimbursement ...

Does gross income include damages?

IRC Section 104 explains that gross income does not include damages received on account of personal physical injuries and physical injuries.

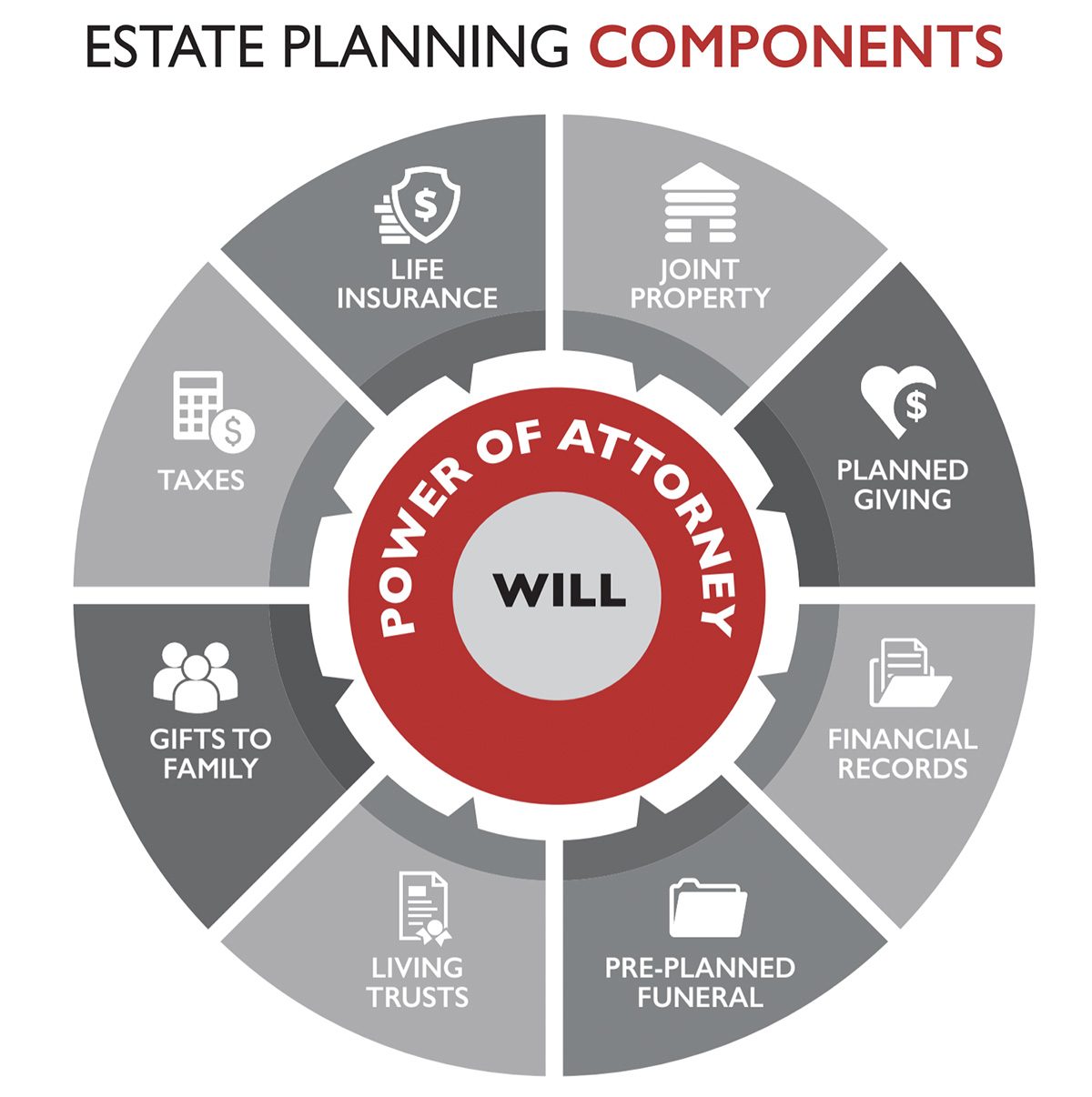

What is estate tax?

Estate Tax. The Estate Tax is a tax on your right to transfer property at your death. It consists of an accounting of everything you own or have certain interests in at the date of death ( Refer to Form 706 PDF (PDF)).

What deductions are allowed in taxable estate?

These deductions may include mortgages and other debts, estate administration expenses, property that passes to surviving spouses and qualified charities.

Do you have to file an estate tax return?

Most relatively simple estates (cash, publicly traded securities, small amounts of other easily valued assets, and no special deductions or elections, or jointly held property) do not require the filing of an estate tax return.

How Long Does an Executor of a Will have to Settle an Estate?

In short, an Executor generally has as long as he or she needs to settle an estate, provided all statutory deadlines are met.

Do I need an EIN to Settle an Estate?

You need an EIN (Employee ID Number), also known as a Tax ID number, to settle an estate. The EIN is used to file taxes on the estate’s behalf.

How to Settle an Estate without a Will?

When it happens, the resolution of the estate will depend on how big it is, how complex it is and how many heirs claim to have rights to a piece of it. State law comes heavily into play in these cases, and the courts would determine who should be appointed to administer and settle the estate.

What happens if a deceased person has a will?

If the deceased only had a Will, it’s likely the estate will have to go through what’s known as probate. What is probate? Probate is the court proceeding that validates a Will. Keep in mind, not all estates will need to go through probate - probate laws can vary significantly depending on what state you’re in and the size of the estate. If there was a Trust set up, or if the estate is very small in value, it may avoid probate all together.

How much is a probate estate worth?

The baseline number to qualify for a simplified probate can range anywhere from $20,000 to up to $150,000 or more.

What is the first step in settling an estate?

The first step (and one of the most important ones) in the process of settling an estate is getting organized . You’ll want to keep track of both your expenses and all the time you spend working on settling the estate, as you’re entitled to be compensated. You should look for a Will.

What do you do after a letter of administration?

After you have what’s known as the Letters of Administration (which are granted by the courts and appoint one person or people authority to deal with an estate), you’ll want to set up a bank account. Use this account to collect money that may be owed to the deceased person (i.e. any final wages or insurance benefits).

What is the impact of estate taxes on settlements?

Recipients of very large settlements or those who are otherwise wealthy should consider the impact of estate taxes on their structured settlement if some payments are scheduled to continue after death. In 2018, this tax issue is only a problem if the decedent’s gross estate exceeds $11,200,000. The present value of any payments remaining after the death of the measuring life will be included in his or her gross estate. IRC Section 2039 states in part: “The gross estate shall include the value of an annuity … receivable by any beneficiary by reason of surviving the decedent under any form of contract … , if … an annuity or other payment was payable to the decedent … for his life or for any period not ascertainable without reference to his death or for any period which does not in fact end before his death.” Inclusion in the estate can cause a liquidity problem. Commutation riders arranged at the time of settlement allow for the conversion of guaranteed future payments, providing immediate funds to pay any applicable estate taxes.

What is gross estate in IRC?

IRC Section 2039 states in part: “The gross estate shall include the value of an annuity … receivable by any beneficiary by reason of surviving the decedent under any form of contract … , if … an annuity or other payment was payable to the decedent … for his life or for any period not ascertainable without reference to his death or ...

What Is the Estate Tax Rate?

On a state level, the tax rate varies by state, but 20% is the maximum rate for an inheritance that can be charged by any state.

How Can I Avoid Estate Taxes?

Keeping your estate under the $11.70 million threshold is one way to avoid paying taxes. Other methods include setting up trusts, such as an intentionally defective grantor trust (IDGT), which separates income tax from estate tax treatment, transferring your life insurance policy, so it won't be counted as part of your estate, and making strategic use of gifting.

How to reduce estate tax exposure?

One way to reduce estate tax exposure is to use an intentionally defective grantor trust (IDGT)— a type of irrevocable trust that allows a trustor to isolate certain trust assets so as to separate income tax from estate tax treatment on those assets. The grantor pays income taxes on any revenue generated by the assets but the assets can grow tax-free. As such, the grantor's beneficiaries can avoid gift taxation .

What happens to an estate when someone dies?

When a person dies, their assets could be subject to estate taxes and inheritance taxes, depending on where they lived and how much they were worth. While the threat of estate taxes and inheritance taxes is real, in reality, the vast majority of estates are too small to be charged ...

What is inheritance tax?

As with estate tax, an inheritance tax, if due, is applied only to the sum that exceeds the exemption. Above those thresholds, tax is usually assessed on a sliding basis. Rates typically begin in the single digits and rise to between 15% and 18%.

What is the federal estate tax for 2021?

For the tax year 2021, the Internal Revenue Service (IRS) requires estates with combined gross assets and prior taxable gifts exceeding $11.70 million to file a federal estate tax return and pay the relevant estate tax. 1 . The portion of the estate that’s above the $11.70 million threshold will ostensibly be taxed at ...

What is the tax rate in Connecticut?

The tax rate is typically 10% or so for amounts just over the threshold, and it rises in steps, usually to 16%. 2 The tax is lowest in Connecticut, where it begins at 10% and rises to 12%, and highest in Washington State, where it tops out at 20%. 5 6 .

Are legal settlements tax-deductible for defendants?

Up till now, we’ve been discussing legal settlements from a plaintiff’s perspective: what they’re taxed on, and what forms the proceeds will be reported on.

What to report on 1099-MISC?

What to Report on Your Form 1099-MISC. If you receive a court settlement in a lawsuit, then the IRS requires that the payor send the receiving party an IRS Form 1099-MISC for taxable legal settlements (if more than $600 is sent from the payer to a claimant in a calendar year). Box 3 of Form 1099-MISC identifies "other income," which includes ...

How much is a 1099 settlement?

What You Need to Know. Are Legal Settlements 1099 Reportable? What You Need to Know. In 2019, the average legal settlement was $27.4 million, according to the National Law Review, with 57% of all lawsuits settling for between $5 million and $25 million.

Why should settlement agreements be taxed?

Because different types of settlements are taxed differently, your settlement agreement should designate how the proceeds should be taxed—whether as amounts paid as wages, other damages, or attorney fees.

How much money did the IRS settle in 2019?

In 2019, the average legal settlement was $27.4 million, according to the National Law Review, with 57% of all lawsuits settling for between $5 million and $25 million. However, many plaintiffs are surprised after they win or settle a case that their proceeds may be reportable for taxes. The Internal Revenue Service (IRS) simply won't let you collect a large amount of money without sharing that information (and proceeds to a degree) with the agency.

What is compensatory damages?

For example, in a car accident case where you sustained physical injuries, you may receive a settlement for your physical injuries, often called compensatory damages, and you may receive punitive damages if the other party's behavior and actions warrant such an award. Although the compensatory damages are tax-free, ...

What form do you report lost wages on?

In this example, you'll report lost wages on a Form W-2, the emotional distress damages on a Form 1099-MISC (since they are taxable), and attorney fees on a Form 1099-NEC. As Benjamin Franklin said after the U.S. Constitution was signed, "in this world nothing can be said to be certain, except death and taxes.".

IRC Section and Treas. Regulation

- IRC Section 61explains that all amounts from any source are included in gross income unless a specific exception exists. For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury. IRC Section 104explains that gross income does not include damages received on account of personal phys…

Resources

- CC PMTA 2009-035 – October 22, 2008PDFIncome and Employment Tax Consequences and Proper Reporting of Employment-Related Judgments and Settlements Publication 4345, Settlements – TaxabilityPDFThis publication will be used to educate taxpayers of tax implications when they receive a settlement check (award) from a class action lawsuit. Rev. Rul. 85-97 - The …

Analysis

- Awards and settlements can be divided into two distinct groups to determine whether the payments are taxable or non-taxable. The first group includes claims relating to physical injuries, and the second group is for claims relating to non-physical injuries. Within these two groups, the claims usually fall into three categories: 1. Actual damages re...

Issue Indicators Or Audit Tips

- Research public sources that would indicate that the taxpayer has been party to suits or claims. Interview the taxpayer to determine whether the taxpayer provided any type of settlement payment to any of their employees (past or present).