How much debt should I have before I file bankruptcy?

The amount of debt that would justify a bankruptcy filing depends on many factors, for example:

- How much does the debtor earn?;

- What is the likelihood that the amount of money that the debtor is earning will increase enough within a reasonable time to pay off their debt?;

- What are the minimum payments that they debtor is currently paying? ...

Should I file bankruptcy or Dig Myself Out of debt?

“When you look at bankruptcy as the only legal option to eliminate your debt and get protection from your creditors, you can see it in a whole new light. There is no doubt that in most situations, filing bankruptcy is the fastest way out of debt for the least amount of money.” [ 1] The truth is, bankruptcy isn’t the end of the world.

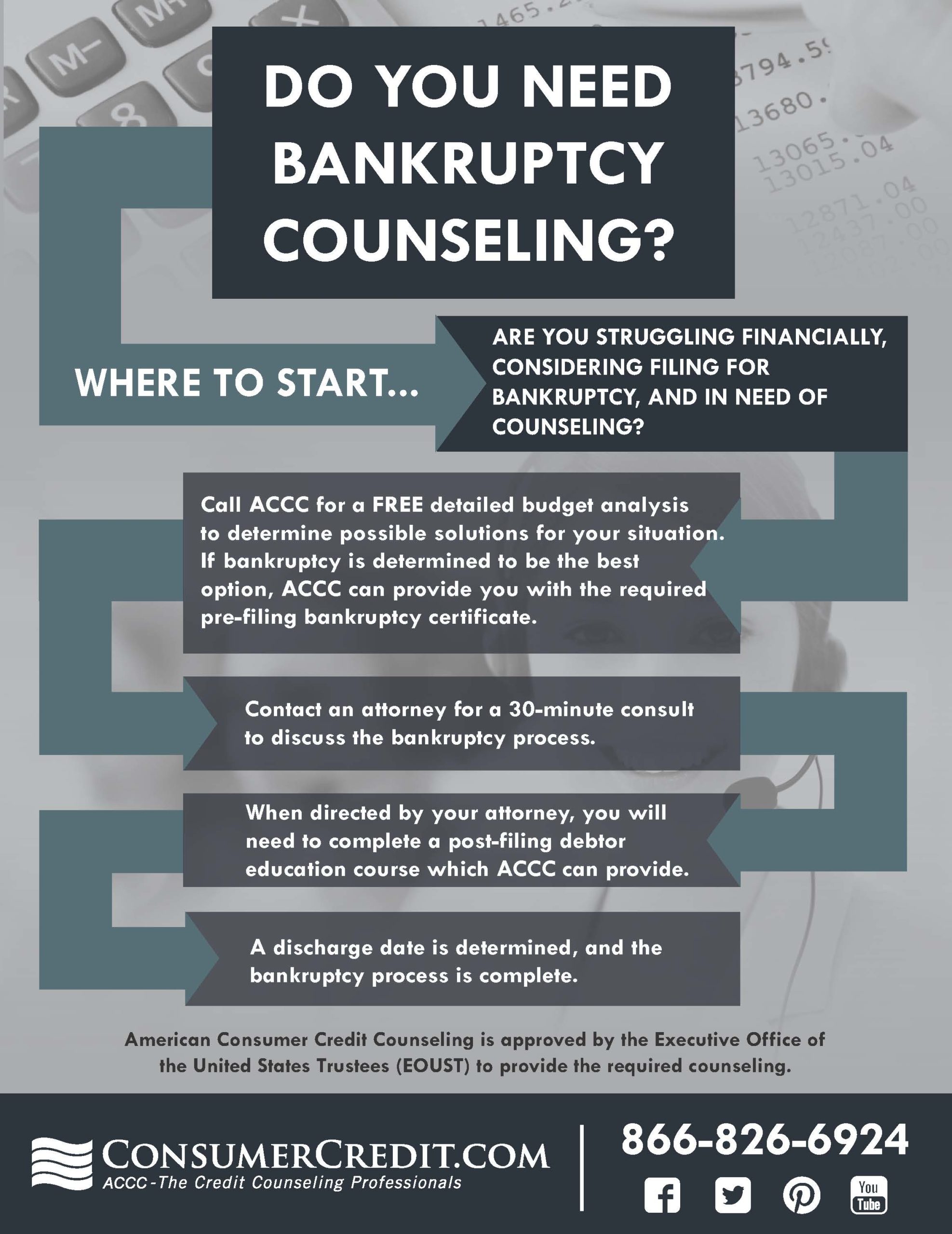

Should I consolidate my debt before filing for bankruptcy?

You may be recommended to try a different debt relief program, like debt management or even debt settlement before filing for bankruptcy. You must take care of this 180 days before you file. You must take care of this 180 days before you file.

Can I repay any debts before filing bankruptcy?

The short answer is no – absolutely not. You should avoid any new debts at least 90 to 180 days before filing bankruptcy. If you purposely take out debt before bankruptcy, knowing you may not pay it back, you could be accused of committing fraud. It could ruin your chances of getting your debt eliminated by the bankruptcy court.

What is Upsolve for bankruptcy?

2 minute read • Upsolve is a nonprofit tool that helps you file bankruptcy for free. Think TurboTax for bankruptcy. Get free education, customer support, and community. Featured in Forbes 4x and funded by institutions like Harvard University so we'll never ask you for a credit card. Explore our free tool

Why do you need a debt management plan?

Your credit counselor may have recommended that you try a debt management plan in order to avoid a bankruptcy filing. A debt management plan is based on an agreement between you and your creditors, who will work with your credit counselor to create a plan for paying off your debts. Not all debts can be included in a debt management plan.

Can I file bankruptcy if I’m in a debt management plan?

Not all debts can be included in a debt management plan. If you’re in a DMP and you can’t afford to continue making the payments you agreed to make as part of the plan, you can file bankruptcy to get immediate and lasting debt relief. If your total payments to a single creditor in the 90 days before filing exceed $600, the trustee can still recover these funds. But, as with a bankruptcy following a debt settlement, your obligation to pay the debts will still be discharged. Once your bankruptcy petition has been filed, you will no longer have to make your monthly DMP payments.

What does preference avoidance mean in bankruptcy?

A preference avoidance just means that the funds you paid to this creditor will be divvied up among your other unsecured creditors .

What is debt consolidation?

Debt consolidation is a popular way for folks to try and get out of the financial hole they find themselves in. This is especially true as folks with a high debt load often end up getting multiple offers for consolidation loans or balance transfers in the mail every week.

Can you file bankruptcy after consolidating debt?

After all, they just paid off all of your debts and wouldn’t have given you the loan to pay off all of your debts if they knew you were about to file for Chapter 7 bankruptcy. You can’t incur new debt knowing that you’ll be filing bankruptcy soon. That is a version of bankruptcy fraud and you won’t be able to eliminate your liability on the debt.

Can Bank Z discharge debt?

If you file bankruptcy shortly after consolidating your debts with a new loan, Bank Z has the right to object to the discharge of your debt. After all, they just paid off all of your debts and wouldn’t have given you the loan to pay off all of your debts if they knew you were about to file for Chapter 7 bankruptcy.

Can domestic support be discharged under Chapter 7 bankruptcy?

It is also stated under some sections of the bankruptcy law that some domestic support obligations may not be discharged under a chapter 7 bankruptcy or a chapter 13 bankruptcy. As a matter of fact, most domestic support obligations must be caught up when chapter 13 bankruptcy. PNB Parivar. Payments must be current in order to receive a discharge.

Is domestic support discharged in Chapter 7?

In a chapter 7 bankruptcy, a domestic support obligation will likely not be discharged. Section 5 indicates that a debt is not dischargeable if it is owed to a child, a former spouse or a spouse in the course of a separation or divorce. Chapter 13 bankruptcy is different from chapter 7 bankruptcy. It does not have the same limitations. Section 5 does not apply to chapter 13. Therefore, a property settlement debt maybe discharged like any other debt. The court will look at the following factors to make a determination.

Can you file Bankruptcy on Divorce Settlement?

At the same time, there are exceptions to this. Plus, there are ways to protect a non-filing spouse during bankruptcy proceedings.

How Can Debt Resolution Attorneys Help Stay Out Of Bankruptcy?

Working with a lawyer might give you leverage and show them that bankruptcy is on the table as an option if you’re facing creditor pressure. Many creditors are willing to negotiate if they know someone’s considering it — this way, their investment in loans can still be recovered somewhat even after lending money has been spent down by negotiating pay-offs at debt settlement negotiations which could end up costing pennies per dollar owed!

Is Your Consumer Debt Rising?

Even if it’s not , we can help with debt relief and discuss strategies that might work for you: including Consumer Proposal

What is debt settlement?

Debt settlement is when you or a third party negotiates with creditors and lenders to pay less than what you owe. Bankruptcy is a legal process in which you petition a bankruptcy court to discard your debt or create a manageable payment plan. Learn more about the differences to figure out which option is right for you.

What is Chapter 7 bankruptcy?

That’s why Chapter 7 is also referred to as “liquidation” bankruptcy. Bankruptcy courts allow Chapter 7 filings if your income is below the state median income. If your income is higher than that, the court will apply a “means test” that analyzes your income and expenses for the past five years. 1.

What are the least desirable routes toward financial recovery for those overwhelmed with unsecured debt?

Debt settlement and bankruptcy are the two least desirable routes toward financial recovery for those overwhelmed with unsecured debt. But if you’re in deep enough, one of these solutions could help you get your finances back in order.

What is the meaning of bankruptcy?

Bankruptcy. An agreement between a borrower and a creditor to reduce the amount of debt owed. When someone claims they can’t afford to pay their debt obligations and asks a bankruptcy court to discharge what they owe. Slightly less damaging to your credit than bankruptcy. Long-term negative impact on credit scores and credit report.

How long does bankruptcy stay on your credit report?

On the other hand, filing for bankruptcy removes the pressure of debt collectors, but it will become a part of your public record and remain on your credit report for up to 10 years.

How long does debt settlement stay on credit report?

Debt settlement is slightly less damaging to your credit than bankruptcy: Though debt settlement can cause your credit score to take a massive hit during the months that you stop paying your bills, once your debt is settled, it will remain on your credit report for seven years —shorter than the 10 years for Chapter 7 bankruptcy. 3

How long does bankruptcy affect credit?

Long-term negative impact on credit scores and credit report: Bankruptcies remain on your credit report for up to 10 years, and the immediate hit that your score will take will be drastic. Once your debt is discharged, however, your score can begin to improve again—assuming all other payment behaviors remain positive. 4.

What is debt settlement?

Debt settlement is a common option for consumers seeking debt relief, especially when it comes to credit card debt. It’s all about paying less than what you owe. Either on your own or with the help of a debt settlement company, you can get settlement agreements with your various creditors that allow you to create a payment plan to repay a smaller percentage of what you owe.

Why is liquidation bankruptcy called liquidation?

It’s commonly called liquidation bankruptcy because it involves selling available assets that don’t qualify for an exemption for a lump sum payment for settling your debts. If you don’t have assets or your assets qualify for the exemption, you can get out of debt for close to nothing.

How is Chapter 13 bankruptcy different from Chapter 13 bankruptcy?

The biggest difference is that Chapter 13 bankruptcy terms are decided by the courts, not negotiated between you and your lender or creditor.

How to contact Debt.com?

By Debt.com. Free Debt Analysis. Contact us at (800)-810-0989. If you’re considering either option, it’s important to learn the truth about how they work and how they are different. They have different effects on the amount you owe, your credit score, credit reports, and financial future.

Is it better to settle debt or pay off debt?

So far, settlement probably sounds great. Before you choose to settle, make sure you know the cons to this method of debt relief. Yes, debt settlement is faster and cheaper. But it can also leave a negative mark on your credit score that could stay there for 7 years. It’s also likely that your credit score will drop.

Can you get out of debt with Chapter 13?

Both could get you out of debt relatively quickly, although with both a debt settlement program and Chapter 13 bankruptcy you will still make monthly payments for a period of time.

Is it better to settle debt or file bankruptcy?

There are many positive aspects of settlement. First, it’s usually the fastest way to get out of debt without filing Chapter 7 bankruptcy. It’s also usually the cheapest option. On average, people who choose debt settlement pay only 48% of what they owe. So far, settlement probably sounds great. Before you choose to settle, make sure you know the cons to this method of debt relief. Yes, debt settlement is faster and cheaper. But it can also leave a negative mark on your credit score that could stay there for 7 years. It’s also likely that your credit score will drop. The settlement industry is also highly prone to scams, so you have to be careful.

What is the purpose of filing bankruptcy?

When an individual files a bankruptcy, the most basic reason is to eliminate debts by receiving a discharge. In a Chapter 7, the individual eliminates unsecured debts (such as medical and credit card debt) and keeps property that is exempt. In a Chapter 13, the debtor proposes a plan to pay back certain types of debt over a three to five year period, can catch up delinquent loans on secured property, and can keep non-exempt property. In either a Chapter 7 or 13, the debtor receives an order at the conclusion of a successful case that discharges (eliminates) any remaining debt. However, some debts may be non-dischargeable, and high among the non-dischargeable debts are debts related to divorce.

What happens if a spouse is obligated to pay a divorce debt?

If a spouse is obligated to pay a divorce-related debt, the indemnification language would make it near irrefutable that the non-filing spouse has legal standing to challenge the treatment and classification and dischargeability of a debt included in the filing spouse’s bankruptcy.

What is a hold harmless debt?

Hold-Harmless Debts. When an order or agreement contains language that orders Spouse A to hold harmless or indemnify the Spouse B for a debt that Spouse A is to pay, the Court is creating a potentially non-dischargeable debt – the indemnification debt from Spouse A to Spouse B.

Why was Giddens' debt not dischargeable?

The court denied some of the grounds but ultimately, agreed that Giddens debt was not dischargeable because it was procured through fraud. More specifically, the court found that at the time Giddens entered into the marital settlement agreement, he had no intention of living up to his obligation to pay and transfer property to Morales.

How to protect a client in a divorce agreement?

Another way to protect a client in a divorce agreement or order is to reserve the issue of alimony for failure to abide by the orders of the court, including payment of the debts.

How to determine if a divorce debt is dischargeable?

The primary question that needs to be asked when determining whether a divorce-related debt is dischargeable is if the debt is a Domestic Support Obligation (DSO). The Bankruptcy Code defines the domestic support obligation at 11 U.S. Code § 101 (14A). The simple version is any child support, alimony, or any other payment that is “in the nature of alimony, maintenance, or support” will be a DSO. The Bankruptcy Court will look to federal law to make this determination, and will look past any labels that may have been used in the divorce agreement or order. The determination is a case-specific determination of whether the intent of the parties or the divorce court was for the obligation to be the nature of support.

What is non-dischargeable debt in Chapter 7?

However, some debts may be non-dischargeable, and high among the non-dischargeable debts are debts related to divorce.

What happens after bankruptcy?

After the sale, any outstanding debt is discharged and you are no longer responsible for paying it. No property is sold in a Chapter 13 bankruptcy. Instead, a repayment plan is put into place based on your income, to be paid over time.#N#Read More: What Happens After Bankruptcy Discharge?

Can you discharge debts in Chapter 7 bankruptcy?

Federal law provides specific exceptions to discharge for marital debts. In a Chapter 7 bankruptcy, if the bill was either incurred during a divorce or separation or in connection with a marital settlement agreement, divorce decree or other court order, it is not dischargeable. This covers most bills and includes unsecured debt, such as credit cards, which are normally dischargeable. By contrast, this exception does not apply to Chapter 13 bankruptcy filings, which does allow discharge of unsecured marital debts, even those incurred during the divorce.

Does indemnification protect against discharge of co-signed debt?

This means that the indemnification provision would not protect against discharge of a co-signed debt. In fact, the only recourse a spouse has in this instance is to participate in the case and try to persuade the court that the debt is either a DSO or the repayment plan must include the debt to ensure the total amount to be repaid equals or exceeds that which would be recovered in Chapter 7 liquidation.

What Effect Does Bankruptcy Have On Judgments

A judgment is a court order indicating that you owe a balance to your creditors. In the event that you cannot pay your debt on time, your creditors can use judgments to try to collect your personal property or garnish your wages to satisfy the debt.

Will Filing For Bankruptcy Stop A Civil Lawsuit Or Get Rid Of A Court Judgment

Filing for bankruptcy will stop some civil lawsuits in their tracks, which can be great if youre facing uncomfortable discovery, like testifying at a deposition. But filing earlier rather than later has other benefits, too. Its much easier to take care of a debt in bankruptcy before you lose a lawsuit and receive a money judgment.

What To Do About A Judgement Against You For Credit Card Debt

If and when a credit card company gets a court judgment against you for unpaid credit card debt, you need to prepare yourself for the creditors attempts to collect the judgment. Know that a credit card judgment is not a criminal matter.

How Bankruptcy Stops Collection Actions Against You

If a creditor decides to sue you for the debt you owe them, the court;will enter a judgment against you for the amount of the debt, attorneys fees, and other costs. The creditor may be able to use the judgment to garnish your wages or your bank account, or even attempt to seize your property.

How Are Judgments Treated Differently In Bankruptcy

While;you may be able to wipe out debt underlying a judgment if it qualifies as;dischargeable;debt, you;may still not be in the clear.

If You Are The Administrator Of A Deceased Estate

If you are the administrator of the deceased individual’s estate, to bankrupt them you must:

What Personal Property Can Be Seized In A Judgment

Sometimes clients want to know if their tangible personal property can be seized to collect a judgment in Florida. A judgment creditor can try to seize a debtors home furnishings.

Chapter 7 and Chapter 13 Bankruptcy Information

Obligations Related to Domestic Support

- The question of domestic support is a common one when filing bankruptcy. Domestic support is considered alimony and child support, or any monies related to maintenance of the family. The court will take a look at federal law in order to determine what debts related to divorce are dischargeable. It is a case specific determination. It also is dependent on the intent of the partie…

Property Settlement

- In a chapter 7 bankruptcy, a domestic support obligation will likely not be discharged. Section 5 indicates that a debt is not dischargeable if it is owed to a child, a former spouse or a spouse in the course of a separation or divorce. Chapter 13 bankruptcy is different from chapter 7 bankruptcy. It does not have the same limitations. Section 5 do...

The Way The Court Looks at Debt

- If there is a situation where the ex-wife still lives in the house and the husband has moved out, the husband would then be responsible to make the mortgage payments. The court would interpret this as a domestic support obligation. This domestic support application would not be dischargeable under a chapter 7 bankruptcy or a chapter 13 bankruptcy. If the husband was to p…