How to pay for closing costs?

- Present A Strong Offer: The easiest way to get the other party to cover closing costs is to present them with a strong offer. ...

- Offer A Quick Close: Truly great real estate deals favor both parties. ...

- Make Fewer Demands: No seller appreciates too many demands. ...

How much are closing costs for the buyer?

What are the typical real estate closing costs for buyers?

- Closing costs for buyers. Here is a quick breakdown of home buyer closing costs.

- Appraisal fees. ...

- Credit report fees. ...

- Mortgage origination fee. ...

- Title insurance policy fees. ...

- Escrow fees. ...

- Home inspection fee. ...

- Attorney fees. ...

- Documentation fees. ...

- Loan discount point fees. ...

What is the average closing cost for a buyer?

New data reveals the average closing costs are $6,693 across all home buyers, and slightly less for first-time buyers. You may be able to negotiate part of your closing costs.

Are closing costs negotiable?

Some closing costs are negotiable: attorney fees, commission rates, recording costs, and messenger fees. Check your lender’s good-faith estimate (GFE) for an itemized list of fees. You can also use your GFE to comparison shop with other lenders.

What is cost settlement?

Settlement costs (also known as closing costs) are the fees that the buyer and/or seller have to pay to complete the sale of the property. Depending on the lender, these may include origination fees, credit report fees, and appraisal fees, as well as property taxes and recording fees.

What is the difference between settlement and closing?

A closing is often called "settlement" because you, as buyer, along with your lender and the seller are "settling up" among yourselves and all of the other parties who have provided services or documents to the transaction.

How much are closing costs in Colorado?

Average closing costs by stateStateAverage home sale priceAverage closing costs with taxesColorado$424,479$3,672Georgia$231,593$3,658Maine$259,925$3,654Arizona$296,978$3,63147 more rows•Sep 28, 2020

Who pays closing costs in Indiana?

In Indiana, you'll pay about 0.8% of your home's final sale price in closing costs, not including realtor fees. Keep in mind that this is only an estimate. While closing costs will always have to be paid, your real estate agent can often negotiate who pays them — you or the buyer.

What not to do after closing on a house?

What Not To Do While Closing On a HouseAvoid Big Charges on a Credit Card. Do not rack up credit card debt. ... Be Careful with Trends. ... Do Not Neglect Your Neighbors. ... Don't Miss Tax Breaks. ... Keep Your Real Estate Agent Close. ... Save That Mail. ... Celebrate!

How long is settlement usually?

Settlement is the process of paying the remaining sale price and becoming the legal owner of a home. At settlement, your lender will disburse funds for your home loan and you'll receive the keys to your home. Generally, settlement takes place around 6 weeks after contracts are exchanged.

Who pays closing cost?

Typically, buyers and sellers each pay their own closing costs. A home buyer is likely to pay between 2% and 5% of their loan amount in closing costs, while the seller could pay 5% to 6% of the sale price to their real estate agent.

Does seller pay closing costs in Colorado?

In Colorado, sellers typically pay for title and closing fees, owner's title insurance, and recording fees.

Can closing costs be included in loan?

Including closing costs in your loan — or “rolling them in” — means you are adding the closing costs to your new mortgage balance. This is also known as financing your closing costs. Lenders may refer to it as a “no-cost refinance.” Financing your closing costs does not mean you avoid paying them.

How do you get closing costs waived?

7 strategies to reduce closing costsBreak down your loan estimate form. ... Don't overlook lender fees. ... Understand what the seller pays for. ... Think about a no-closing-cost option. ... Look for grants and other help. ... Try to close at the end of the month. ... Ask about discounts and rebates.

Does seller pay closing costs?

The real estate commission or the broker's fee has to be paid by the seller at the time of closing. And the rest of the charges and expenses are the buyer's responsibility. Unless the terms of the deal dictate otherwise, it is the responsibility of the buyers to pay the closing costs.

What are average closing costs in Indiana?

According to data from ClosingCorp, the average closing cost in Indiana is $2,100.62 after taxes, or approximately 0.7% to 1.05% of the final home sale price.

Is closing date and settlement date the same?

"Settlement date" and "closing date" are synonymous terms referring to the date when a property's seller and buyer meet to finalize the deal. At this time, the deed to the property is transferred from the seller to the buyer and all pertinent paperwork is completed.

What does settlement mean when buying a house?

What is settlement? Property settlement is a legal process that is facilitated by your legal and financial representatives and those of the seller. It's when ownership passes from the seller to you, and you pay the balance of the sale price. The seller sets the settlement date in the contract of sale.

How soon after settlement can you move in?

You'll have to vacate prior to settlement day unless another arrangement has been negotiated. Buyers are generally keen to get in the day after settlement, so you'll want everything ready to go the day before.

Is settlement date the day you move in?

Settlement day is the day you assume legal ownership of your new home. Picture: iStock.

What is settlement fee?

In real estate, a settlement fee is a charge that covers expenses in excess of the amount a person pays to purchase or sell a property. Settlement fees can encompass many types of expenses, but often include such things as application and attorney ’s fees, loan origination fees, and fees for title searches.

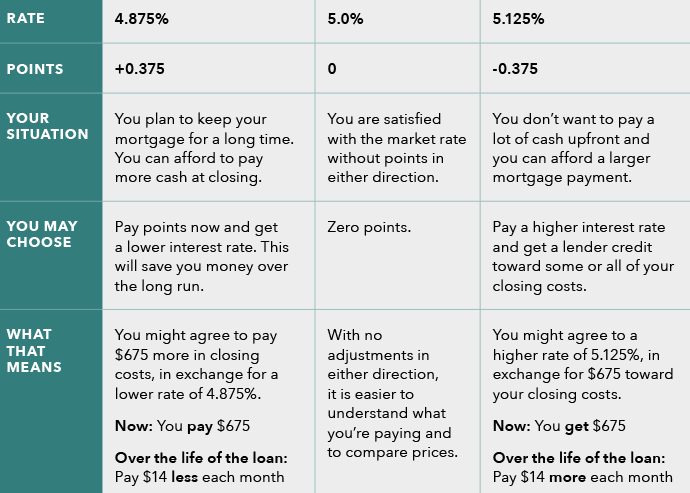

What is a point fee?

Points are fees that are charged a single time and can be negotiated with a lender to lower the interest rate a borrower will pay on a mortgage in exchange for paying a particular sum up front.

What is a point in a mortgage?

Points are fees that are charged a single time and can be negotiated with a lender to lower the interest rate a borrower will pay on a mortgage in exchange for paying a particular sum up front. For example, paying $1,000 US Dollars (USD) up front might lower a person’s interest paid over the life of his loan by one percent. Points paid at settlement are tax deductible in some jurisdictions as well.

Do appraisers charge fees?

Appraisers and home inspectors charge fees, which are often included in settlement fee totals. In most cases, the settlement fees a seller pays are negotiable. In order to make his home more attractive or easier to buy, a seller may agree to pay one or more of the settlement fees usually paid by the buyer.

Is it legal to have a seller assist with a settlement fee?

Having the seller assist with a settlement fee is usually legal, as long as the seller's contribution is detailed in the official agreement between the buyer and seller and doesn't violate any terms set by the lender.

Is an appraisal included in settlement fees?

Lenders may also require an inspection by a professional home inspector in order to analyze the structure of the property and look for evidence of issues such as termites. Appraisers and home inspectors charge fees, which are often included in settlement fee totals.

What are closing costs?

Your closing costs include a number of different fees that are all associated with your financing of the purchase of the property. These typically include your origination fee, recording fees, points, the cost of the title insurance, title insurance endorsements, attorney fees, and the payment of private mortgage insurance on the home.

What is settlement on HUD?

The settlement is the finalization of your purchase of real estate property. The fees associated with this sale are referred to as your settlement costs. Your settlement cost will be detailed on your HUD-1 statement, often referred to as your Settlement Statement.

Why do we review closing statements before closing?

Then before closing we will review the closing statement to make sure the closing company didn't make any mistakes that will cost you money . You could end up paying more in closing cost through mathematical error or improper reading of the contract by the closing company. You would be amazed at the credits and other monies that were supposed to be given to the buyer at closing that were not on the closing statement upon on first review.

What does a realtor estimate?

In addition, your Realtor will provide you with an estimate of your expenses at the time of writing your purchase offer. This estimate will include best guesses for the charges the lender will be charging you for. The lender's cost include document preparation, processing fees and credit report.

Who pays for title insurance in Florida?

Northeast Florida is a little different then the rest of the country in that Sellers typically pay for the title insurance cost on a purchase transaction. For this reason the Seller typically picks the closing agent or closing attorney and is responsible for those associated cost. However, if you are refinancing your home then you will be responsible for the title insurance.

Why are the amount you pay not identical?

The amount that you must pay are not identical due to the fact that you each have certain expenses that are specific to your particular position as buyer or seller. Sometimes, it is prearranged prior to the closing for the seller to pay some of your costs as Buyer.

Who pays closing costs?

Typically the buyer pays closing costs, though sometimes negotiations between the buyer and the seller can lead to the seller paying some of the closing costs.

What is origination fee?

Usually a percentage of the amount loaned (often 1%). The origination fee is stated in the form of points.

How long does an adjustable rate mortgage last?

Note: Bank of America adjustable-rate mortgage (ARM) loans feature an initial fixed interest rate period (typically 5, 7 or 10 years) after which the interest rate becomes adjustable every six months for the remainder of the loan term .

What is the purpose of collecting money from a borrower?

Money collected from the borrower by the lender (typically as part of the monthly mortgage payment) in order to pay property taxes and homeowners insurance premiums.

How much is a point on a mortgage?

Money paid to the lender, usually at mortgage closing, in order to lower the interest rate. One point equals one percent of the loan amount. For example, 2 points on a $100,000 mortgage equals $2,000. Sometimes referred to as discount points or mortgage points.

What is the down payment on a home?

Down payment. Money paid toward the purchase of a home, typically ranging between 5% and 20% of the purchase price. A down payment of less than 20% often requires the borrower to have private mortgage insurance.

What is loan amount?

Loan amount. The amount of debt, not including interest, being assumed by taking out a mortgage. Interest rate. The cost of a loan to the borrower, expressed as a percentage of the loan amount and paid over a specific period of time. The interest rate does not include fees charged for the loan.

What is title settlement fee?

The title settlement fee, or closing fee, is a charge from the title company to cover the administrative costs of closing. Title companies may or may not list out the individual costs of the fee.

How much does a home buyer pay for closing costs?

Home buyers can typically expect to pay 2% – 5% of the loan amount in closing costs. One of the main costs is a title fee. Here we’ll cover what title fees are, who pays them and how much they cost.

What Are Title Fees?

Title is the right to own and use the property. Title fees are a group of fees associated with closing costs. These fees pay a title company to review, adjust and insure the title of the property.

How to find closing costs?

You can find title fees and overall closing costs on a couple documents: 1 Closing disclosure: Your closing disclosure will break down total closing costs, including title fees, in an itemized list. 2 Loan estimate: The loan estimate will list your total closing costs, along with title service fees, and tell you the cash you need to bring to close.

How much does title fee vary?

Title fees change from company to company and from location to location. They can also change depending on what’s included. In general, closing costs, which title fees are a large part of, cost from 2% – 5% of the total loan amount.

How much does it cost to record a deed?

The national average for this charge is around $125.

What is abstract of title?

The abstract is the summary of the title search from the title company. It compiles the details of the search and the related official documents and communicates them in a concise manner. Abstract of title fees can range from $200 – $400 for an update to the abstract to $1000+ if a new abstract of title must be created.

What is settlement fee?

As you'll see from the results provided by the closing cost calculator, the settlement fees you'll pay are a collection of lender and third-party charges. On the Loan Estimate, you'll find that the total cash required at settlement will also include one other major expense: the down payment.

How much are closing costs?

Enter your loan details in our closing costs calculator to get an estimate of the fees you'll pay at closing — also referred to as mortgage settlement.

How does closing cost work?

How it works: Your lender pays your closing costs in exchange for either charging you a higher interest rate or adding the fees into your loan amount, or both.

What is closing cost?

Closing costs are fees for the services, taxes and insurance required for the lender to evaluate the home you’re buying and process and finalize your mortgage.

What is application fee?

Application fee: This is a lender charge that helps defray the cost of processing a loan. While classified here as a "fixed," not shoppable, expense, not all lenders charge an application fee, and it's worth comparing lenders to find the best combination of low fees and a favorable interest rate.

What is closing cost calculator?

This closing costs calculator lets you see an estimate of costs without waiting to apply for a mortgage. Having an estimate while you are saving and shopping for a home puts you in the driver’s seat by giving you time to plan how you’ll pay the total amount due at settlement.

How much closing cost on $300000 house?

On a $300,000 house, we assume $9,261 in closing costs (about 3.4% of the loan's value). Costs you can shop for amount to about $7,600, while fixed costs and fees are estimated to be $1,661.

What are closing costs?

When are closing costs due? Seller closing costs are a combination of taxes, fees, prepayments and services that vary depending on your location. Closing costs can differ due to variations in local tax laws, lender costs, and title and settlement company fees.

How much does a buyer pay for closing costs?

Buyer closing costs: As a buyer, you can expect to pay 2% to 5% of the purchase price in closing costs, most of which goes to lender-related fees at closing. More on buyer closing costs later. Seller closing costs: Closing costs for sellers can reach 8% to 10% of the sale price of the home. It’s higher than the buyer’s closing costs because ...

What is a credit toward closing costs?

This is also called a seller assist or seller concession.

How much does escrow cost?

Escrow providers charge either a flat fee (between $500 and $2,000, depending on where you live), or about 1% of the home sale price to manage the closing of the transaction, which includes the signing and recording of the closing documents and the deed, and the holding of all the purchase funds. There are usually some additional charges — think office expenses, fees for transferring funds, the copying of documents, and notary charges.

How much does closing cost for a home?

The average closing costs for a seller total roughly 8% to 10% of the sale price of the home, or about $19,000-$24,000, based on the median U.S. home value of $244,000 as of December 2019.

Why are closing costs higher than closing costs?

It’s higher than the buyer’s closing costs because the seller typically pays both the listing and buyer’s agent’s commission — around 6% of the sale in total. Fees and taxes for the seller are an additional 2% to 4% of the sale. However, seller closing costs are deducted from the proceeds of the sale of the home at closing, ...

When selling a house, do you have to pay prorated taxes?

When you go to sell your house, you’ll be responsible for prorated property taxes due up to the date of the sale, at which point the buyer will take over. Depending on your timing, you may have to pay money at closing to bring yourself up to date.

How much does a seller pay for closing costs?

Closing costs for sellers of real estate vary according to where you live, but as the seller you can expect to pay anywhere from 6% to 10% of the home’s sales price in closing costs at settlement. This won’t be cash out of the seller’s pocket; rather it will be deducted from the profit on your home—unless you are selling with very low equity on your mortgage. In this case, sellers may need to bring a little cash to the table to satisfy your lender—and some closing costs may be held in escrow.

What are closing costs for sellers?

Additional closing costs for sellers of real estate include liens or judgments against the property; unpaid homeowners association dues; prorated property taxes; escrow fees; and homeowners association dues included up to the settlement date.

What are the taxes that are included in closing costs?

Transfer taxes, recording fees, and property taxes are key parts of a seller’s closing costs. Transfer taxes are the taxes imposed by your state or local government to transfer the title from the seller to the buyer. Transfer taxes are part of the closing costs for sellers.

Why is my mortgage payoff higher than my mortgage balance?

This is because of lenders’ prorated interest on the mortgage.

What is title insurance?

Title insurance fees are another fee to keep in mind when you sell real estate. As part of closing costs, sellers typically pay the buyer’s title insurance premium. Title insurance protects buyers and lenders in case there are problems with the title in a real estate deal.

How much commission does a real estate agent get for a $350,000 purchase?

For a $350,000 purchase price, the real estate agent’s commission would come to $21,000. Buyers have the advantage of relying on sellers to pay real estate agent commissions. 2. Loan payoff costs. Most home sellers often seek out a sales price for their home that will pay off their mortgage and satisfy their lenders.

Do you have to include closing costs when selling a house?

Also, don’t forget to estimate some of the closing costs associated with preparing to sell, such as cosmetic repairs or improvements to make your home more attractive to buyers. Those closing costs may be returned with a higher sales price, but you should still include them in your calculations.

Origination Costs

Title Settlement Closing Fee and Other Costs

- Additional costs may also apply whenever you take out a loan. Many of the title costs vary from company to company, allowing you to shop around to get a good deal on title as some are owned by attorneys, while others are not. Usually, you will pay a fee for title services, sometimes there are costs the seller will pay as well. A title is a document...

Administrative Settlement Fees

- Before finalizing a home sale, lenders and other agents must perform a range of administrative tasks. These imply additional fees. Financial institutions, for instance, have to ensure that they have collateral for making any loan. This usually involves an appraisal fee to confirm the value of your property. Banks and brokers will also need to check your credit history to determine if they …

How to Find Your Title Settlement Closing Fee

- You can find title settlement closing fees on your loan estimate and closing disclosure. This legally required document lists all the costs, risks and features associated with your mortgage. Lenders are obliged to provide you with a loan estimate within three days of making your application. Learning more about title settlement closing fees lets you plan for the transaction b…