You can contact the debt collection agency in writing and offer a settlement figure. Generally, you should start the negotiation by offering approximately 25 percent of the debt. You can make a counter offer if the agency's settlement offer is too high or it rejects your offer.

Full Answer

How to make a settlement offer to debt collection agency?

1 A debt collection agency may contact you with a settlement offer. 2 You can contact the debt collection agency in writing and offer a settlement figure. ... 3 You can make a counter offer if the agency's settlement offer is too high or it rejects your offer. ... 4 Accept the terms of the agreement in writing.

What is a debt settlement offer letter?

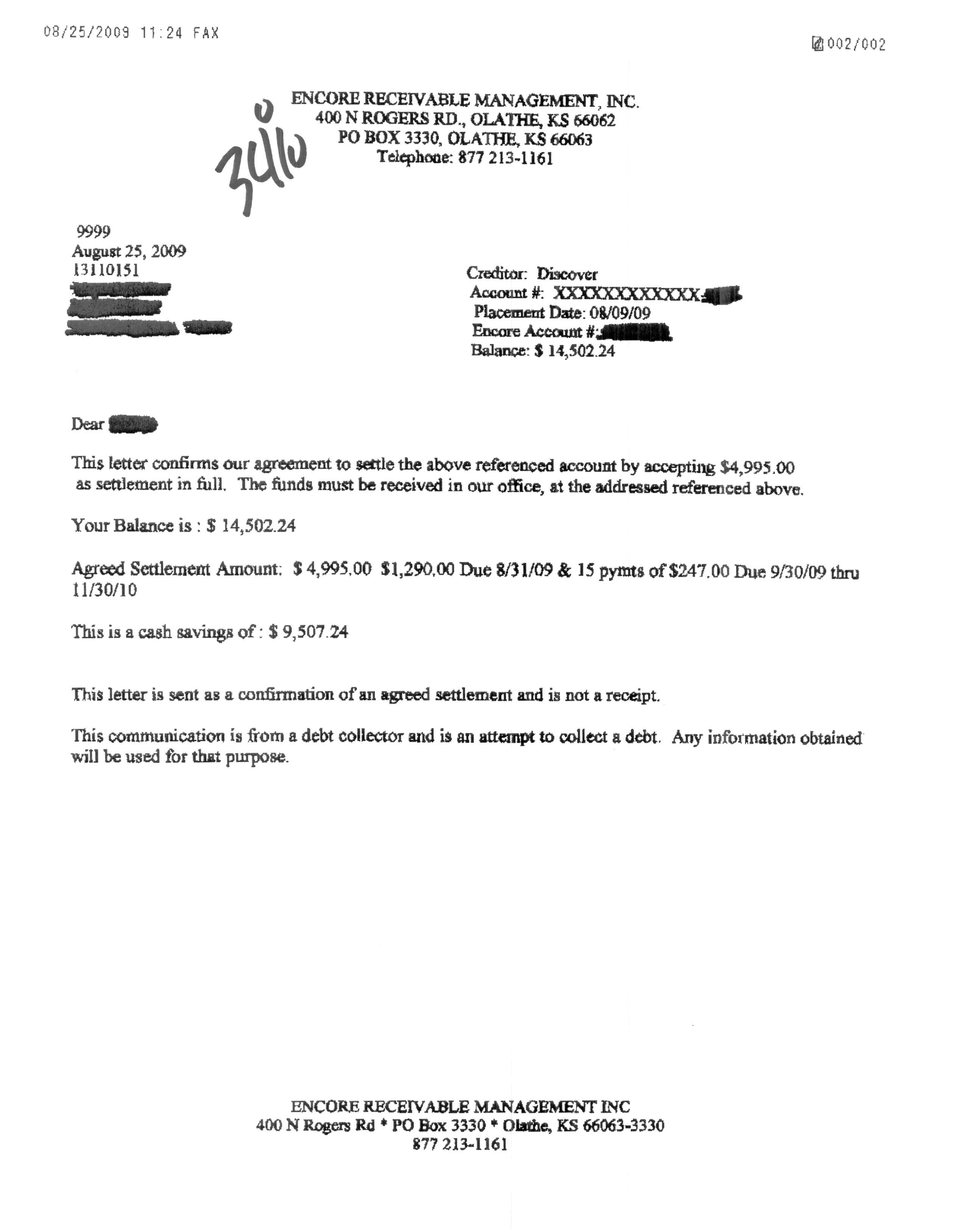

A debt settlement offer letter is a written proposal that a debtor or his attorney sends to a creditor or a debt collections agency to offer a specific amount of money to forgive a debt. A creditor may also send a debtor an offer letter.

Can you offer a lump sum payment to settle a debt?

At times in life, you may find you are unable to pay a bill that then goes to a debt collection agency. Once this has happened, you can enter into a payment agreement or offer a lump sum payment to clear the debt. This can be done using a debt settlement offer letter.

What is a debt settlement?

Debt settlement is one option you have, which means offering to pay a portion of your debt in return for the creditor or debt collector forgiving the rest. You might either pay it back in one lump sum or in installments.

How do you get an offer to settle a debt?

A 6-step DIY debt settlement planAssess your situation. ... Research your creditors. ... Start a settlement fund. ... Make the creditor an offer. ... Review a written settlement agreement. ... Pay the agreed-upon settlement amount.

How much should I offer to settle a debt with a collection agency?

Start by offering cents on every dollar you owe, say around 20 to 25 cents, then 50 cents on every dollar, then 75. The debt collector may still demand to collect the full amount that you owe, but in some cases they may also be willing to take a slightly lower amount that you propose. A payment plan.

Can you negotiate a settlement with a collection agency?

Believe it or not, though, it's possible to negotiate with a collection agent and end up paying less than you owe. Why is that? Because the collection agency bought the original debt from your creditor, most likely for a substantial discount. That means they don't have to recover the entire amount to make a profit.

What is a reasonable offer to settle a debt?

When you're negotiating with a creditor, try to settle your debt for 50% or less, which is a realistic goal based on creditors' history with debt settlement. If you owe $3,000, shoot for a settlement of up to $1,500.

What happens if a debt collector won't negotiate?

If the collection agency refuses to settle the debt with you, or if the agency or creditor agrees to settle, but you renig on your end of the agreement, the collection agency or creditor may decide to pursue more aggressive collection efforts against you, which may include a lawsuit.

What is the 11 word phrase to stop debt collectors?

If you need to take a break, you can use this 11 word phrase to stop debt collectors: “Please cease and desist all calls and contact with me, immediately.” Here is what you should do if you are being contacted by a debt collector.

What is a reasonable full and final settlement offer?

It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

What should you not say to debt collectors?

Don't Give Information About Your Income, Debts, or Other Bills. Debt collectors can get some of this information from your credit report and may even use it to get you to make immediate payment. For example, they may say “I see that you're current on all your credit card payments.

Is it better to settle or pay in full?

Paid in full means the remaining balance of your debt, including interest, was paid off. Paying in full is an option whether your account is current, past due or in collections. It's better to pay in full than settle in full when it comes to paying off debt.

Is it worth it to settle debt?

In general, paying off the total amount of debt you owe is a better option for your credit. An account that appears as "paid in full" on your credit report shows potential lenders that you have fulfilled your obligations as agreed, and that you paid the creditor the full amount due.

Can I pay original creditor instead of collection agency?

Working with the original creditor, rather than dealing with debt collectors, can be beneficial. Often, the original creditor will offer a more reasonable payment option, reduce the balance on your original loan or even stop interest from accruing on the loan balance altogether.

What is the average percentage on debt settlement?

According to the American Fair Credit Council, the average settlement amount is 48% of the balance owed. So yes, if you owed a dollar, you'd get out of debt for fifty cents.

What is a reasonable full and final settlement offer?

It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

What is the average debt settlement percentage?

According to the American Fair Credit Council, the average settlement amount is 48% of the balance owed. So yes, if you owed a dollar, you'd get out of debt for fifty cents.

Can I pay original creditor instead of collection agency?

Working with the original creditor, rather than dealing with debt collectors, can be beneficial. Often, the original creditor will offer a more reasonable payment option, reduce the balance on your original loan or even stop interest from accruing on the loan balance altogether.

What happens if you pay a settlement offer?

As long as your creditors accept your offer – i.e. agree to sum of money in the settlement offer – they will accept partial settlement of your debt in exchange for writing off the remaining amount you owe. If the settlement offer is big enough, the money will be shared equally among all of your creditors.

Is debt settlement the right route?

Debt settlement makes the most sense in cases where you can’t afford your current bills, but you can afford to pay something, and you want to avoid bankruptcy.

How to settle a debt with a debt collector?

Here’s how to settle with a debt collector. The first thing you should know is that you can negotiate. Debt settlement is one option you have, which means offering to pay a portion of your debt in return for the creditor or debt collector forgiving the rest. You might either pay it back in one lump sum or in installments.

What to do if you hire a debt settlement company?

If you hire a debt settlement company, they should handle the back-and-forth negotiations with a debt collector. But if not, you’ll be in charge. Before you make a settlement offer, you’ll need to figure out how much you can afford to pay and whether you can pay in installments or as a lump sum.

What time can debt collectors call you?

Debt collectors can only call you between 8 a.m. and 9 p.m. You can send a letter asking debt collectors to stop contacting you. The Consumer Financial Protection Bureau has a sample letter you can download. But be careful using this type of letter if there is still time for the collector to sue you in your state.

How long does a settlement last?

One big issue with many settlement companies is that their programs can last as long as 36 to 48 months. During that time, they ask you to stop paying your creditors to save up money for a lump sum settlement payment. But in the meantime, you keep racking up interest charges and fees.

How long can a debt collector sue you?

There is a statute of limitations ( it varies by state and type of debt) for how long a debt collector has to sue you. Most statutes are three to six years. If the delinquent debt is past the statute of limitations in your state, it’s considered expired. But admitting that the debt is yours, or paying a portion of it, ...

How much does a debt settlement company charge?

Check out the company’s ratings with the Better Business Bureau. Ask them what fee they will charge you (some can be as high as 20 to 25%) and whether their fee is based on your total debt or just the portion that is forgiven. Legally, they can’t charge you any fees upfront.

How does debt settlement work?

How does debt settlement work? When you work with a debt settlement company, you’ll stop paying your bills until the amount you owe has become significant. At that point, the settlement agency will approach your creditors to make a debt settlement offer, proposing to wipe out your debt with a lump sum payment that is less than what you owe. Creditors may be inclined to accept a debt settlement offer if they feel it’s the best they can do.

How long does it take to pay off debt?

Most consumers who enter a debt management plan can pay off their debts within 60 months.

Can you settle debt with creditors?

When you have more debt than you can handle, making a debt settlement offer to your creditors may seem like a great strategy. After all, who wouldn’t want to get out of debt by paying a fraction of what you owe? But there are serious drawbacks to every debt settlement offer, and it’s important to understand your exposure before you apply for debt settlement.

Is debt management better than debt settlement?

When you want to get out of debt as quickly as possible but don’t want to make a debt settlement offer or risk the adverse debt settlement credit impact, a debt management plan may be a better course of action. The benefits of a debt management plan vs debt settlement include:

Does paying your creditors damage your credit?

No lasting damage to your credit rating, since you’ll continue to pay your creditors.

Why is it beneficial to settle debt?

Settling debt is beneficial to the collector because it implies that they will get a significant part of the total amount owed. As you may already know, the odds of getting an account in collections paid are not good. It is more likely that the debtor will file for bankruptcy and the debt automatically discharged. This means that the debt collector risks getting nothing out of what they are owed. And even if the debtor does not file for bankruptcy, it will still cost a lot of time and money trying to take legal action against the debtor to collect the debt.

What information is needed for a debt settlement letter?

Your personal information includes your full legal name, mailing address, and current date.

What is a debt settlement offer letter?

A debt settlement offer letter is a written proposal that a debtor or his attorney sends to a creditor or a debt collections agency to offer a specific amount of money to forgive a debt. A creditor may also send a debtor an offer letter. Usually, debt settlement offer letters are sent when a debt is past the due date and has probably been moved to a collection agency, and the debtor is unable to pay all the debt they’ve accumulated.

Is it bad to settle a debt?

Although settling a debt account is considered negative by many people, it won’t hurt you as much as not paying at all. Suppose you are planning to make a major purchase, for example, buying a home. In that case, you may be required to either settle or clear any outstanding delinquent debts before you can qualify for a loan from any financial lending institution. If paying the debt in full is not an option due to financial constraints, consider settling the account because it is more beneficial to your financial health than letting the debt go delinquent or, worse, to default.

What to do if a collection company contacts you about a debt?

It may say the account will be settled, paid in full, accepted as settlement in full, or something similar. Keep a copy of the letter, and any payment confirmations, in case a collection company contacts you about the debt again in the future.

Why do creditors accept settlement offers?

Creditors can either send your accounts to collections, sue you for nonpayment, or sell the debt to a third-party debt buyer or collector.

What to do if a creditor doesn't settle?

If the creditor doesn't agree to settle, you may want to wait until it sells the debt and try again with the debt buyer or collection agency.

How to settle debt for less than what you owe?

While many creditors might agree to settle your debt for less than what you owe, there’s no guarantee that debt settlement will work. If you’re considering trying it on your own, here’s a rough guide to the steps you may want to take: 1. Assess your situation. Create a list of your past-due accounts with the creditors’ names, how much you owe, ...

How long do you have to be late to settle a credit card?

For example, you may need to be at least 90 days late on an account before a creditor considers settling. Or, some creditors might not settle at all, and you’ll have to wait until the debt is sold to another company. Some creditors might also be more likely to sue you to collect an unpaid debt than others.

What to do if you feel like you're drowning in debt?

If you feel like you’re drowning in debt, the idea of settling for less money than you owe can be appealing. You could hire a debt settlement company that will work on your behalf to negotiate settlements with your creditors.

What to do if you think you have enough money to settle an account?

Once you think you have enough money saved up to settle an account, you can call your creditor and make an offer. In some cases, the creditor may have already sent you a settlement offer. You could accept the offer, or respond with a lower counteroffer.

Was this answer helpful to you?

Please do not share any personally identifiable information (PII), including, but not limited to: your name, address, phone number, email address, Social Security number, account information, or any other information of a sensitive nature.

What happens if the statute of limitations is passed?

If the statute of limitations has passed, then your defense to the lawsuit could stop the creditor or debt collector from obtaining a judgment. You may want to find an attorney in your state to ask about the statute of limitations on your debt. Low income consumers may qualify for free legal help.

How to contact a debt collector?

Any debt collector who contacts you to collect a debt must give you certain information when it first contacts you, or in writing within 5 days after contacting you, including: 1 The name of the creditor 2 The amount owed 3 That you can dispute the debt or request the name and address of the original creditor, if different from the current creditor.

What is CFPB sample letter?

The CFPB has prepared sample letters that you can use to respond to a debt collector who is trying to collect a debt. The letters include tips on how to use them. The sample letters may help you to get information, set limits or stop any further communication, or exercise some of your rights.

How to talk to a debt collector about your debt?

Explain your plan. When you talk to the debt collector, explain your financial situation. You may have more room to negotiate with a debt collector than you did with the original creditor. It can also help to work through a credit counselor or attorney.

How long does it take for a debt collector to contact you?

Any debt collector who contacts you to collect a debt must give you certain information when it first contacts you, or in writing within 5 days after contacting you, including: The name of the creditor. The amount owed. That you can dispute the debt or request the name and address of the original creditor, if different from the current creditor.

How long does a debt have to be paid before it can be sued?

The statute of limitations is the period when you can be sued. Most statutes of limitations fall in the three to six years range, although in some jurisdictions they may extend for longer.

What line does the sender sign after the word "sincerely"?

The Sender must then sign his or her Name on the blank line following the word “Sincerely”

What is a debt settlement offer letter?

The Debt Settlement Offer Letter is a form that shows a debt is willing to be closed if the parties agree to new terms. Typically, this letter is from the debtor in order to offer a lump sum payment if the creditor is willing to release the burden of the full amount. After the letter is accepted, the parties will enter a debt settlement agreement unless a simple receipt is enough to satisfy the debtor.

What happens after a letter is accepted?

After the letter is accepted, the parties will enter a debt settlement agreement unless a simple receipt is enough to satisfy the debtor.

Where to find blank lines in a letter?

Locate the set of blank lines beneath the body of this letter . The Sender of this letter should use these lines to document his or her current “E-Mail” Address on the first one.

What is the next empty space in a letter?

The next empty space is reserved for the Date of this Letter. Make sure to enter the current date in the traditional Month Name, Two-Digit Day, and Four-Digit Calendar Year.

Where is the address on a letter?

The first task will be to address the three blank lines on the right half of the page just beneath the Title. The Sender of this letter should fill in his or her Full Name on the first line, then use the next two lines to record his or her Mailing Address.

What is a debt settlement offer letter?

This can be done using a debt settlement offer letter. This is a form that is used when the debtor and creditor want to agree to new terms in settling the outstanding debt. The letter is usually sent by the debtor to the creditor and may offer a lump sum that is not the full amount, but one that is agreeable to the creditor to accept ...

What should a debt settlement letter include?

There are some key details that all debt settlement offer letters should have: The full name used for the credit account. Your full address. Your account numbers or a reference number from the creditor. This information is what your creditor will need to pull up all of the relevant details of your account with them.

How to write a settlement letter?

Make sure your letter has: 1 Header – this should include your full name and address, as well as the date that the letter has been written. 2 Body – this is where you will explain the details of your settlement offer (amount, dates of payments you will make, and how they will be made) and what you are expecting from your creditor. 3 Contact – your contact details, including a current phone, mobile, and e-mail address. 4 Closing – this is where you will sign the letter

Why is it important to have a copy of an offer of acceptance from the creditor?

This is why it is important to have a written copy of an offer of acceptance from the creditor as proof, to stop them from trying to come back and claim the balance afterward.

What percentage of debt should be offered to a creditor?

Typically, an offer of between 30% of the debts outstanding balance should be made to a creditor for them to even consider it. The cre4ditor will normally come back with a counteroffer of 50%.

How long does a partial settlement stay on your credit report?

Negative marks on your credit report, such as a partial debt settlement, can stay on your report for 7 years.

Can a creditor claim a debt that was partially paid?

One main question people ask is whether a creditor can try to claim the balance of a debt that was partially paid and accepted as releasing the debtor from the debt. When a creditor agrees to do so, they are considered to be estopped from being able to claim the remainder of the debt. Estoppel occurs when a debtor has relied on the creditor’s release agreement, making it unjustified for them to go back on that agreement. This is why it is important to have a written copy of an offer of acceptance from the creditor as proof, to stop them from trying to come back and claim the balance afterward.