- Define your goals. All debt settlement negotiations start with an offer – either a collector reaches out to you or you reach out to a creditor.

- Know who holds the debt. First, make sure you know who you’re talking to. ...

- Reach an agreement. When you start your actual negotiation, start low. ...

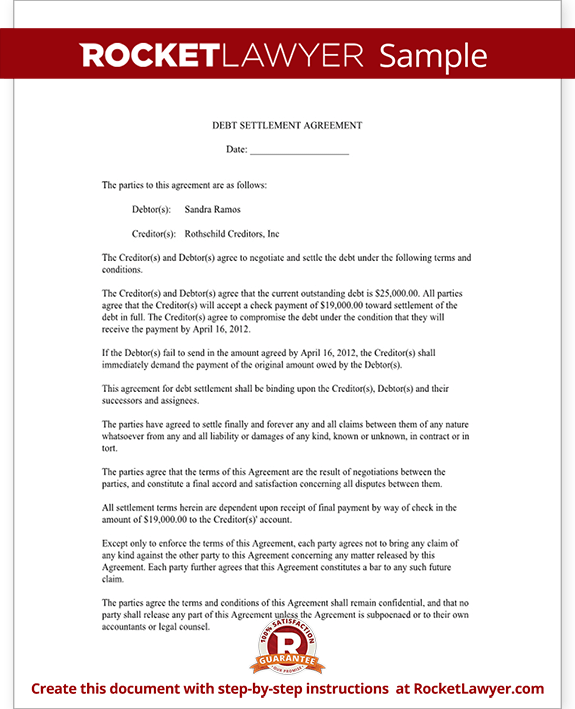

- Sign the formal document. Once that agreement is reached, the terms of the settlement are laid out in writing and both parties sign the formal debt settlement agreement.

- Pay the settlement amount. You pay the amount agreed to, usually in a single lump sum settlement.

- Make sure the creditor reports the final status of the account to the credit bureaus. The new status of your account should show up on your credit report. ...

Full Answer

Does debt negotiation really work?

In a Nutshell. Debt negotiation can work to help you settle your debts for less than you owe. But it only usually works with certain kinds of debts and with accounts that are several months late or nearing their statute of limitations. It may work better with a third-party debt collector than the original lender.

What is the best way to settle debt?

Part 1 of 3: Negotiating the Debt Amount Download Article

- Read the judgment. Debtors and creditors should review the court order (judgment) to determine the total amount due and any specific payment instructions ordered by the court.

- Evaluate your financial situation. Whether you are the creditor or the debtor, you should review your finances before negotiating the amount of the debt.

- Contact the other party. ...

How to settle your debts on your own?

How to do a DIY debt settlement: Step by step

- Determine if you’re a good candidate. Have you considered bankruptcy or credit counseling? ...

- Know your terms. You need to negotiate two things: how much you can pay and how it’ll be reported on your credit reports.

- Make the call. Dealing with your creditor will require persistence and persuasion. ...

- Finalize the deal. ...

How do I settle a debt with a debt collector?

- A debt collection agency may contact you with a settlement offer.

- You can contact the debt collection agency in writing and offer a settlement figure. ...

- You can make a counter offer if the agency's settlement offer is too high or it rejects your offer. ...

- Accept the terms of the agreement in writing.

What percentage should I offer to settle debt?

When you're negotiating with a creditor, try to settle your debt for 50% or less, which is a realistic goal based on creditors' history with debt settlement. If you owe $3,000, shoot for a settlement of up to $1,500.

How does a debtor negotiate a settlement?

To get ready to negotiate a settlement or repayment agreement with a debt collector, consider this three-step approach:Learn about the debt. ... Plan for making a realistic repayment or settlement proposal. ... Negotiate with the debt collector using your proposed repayment plan.

Will a debt collector settle for 30%?

Lenders typically agree to a debt settlement of between 30% and 80%. Several factors may influence this amount, such as the debt holder's financial situation and available cash on hand.

How much can you negotiate a debt?

Start by offering cents on every dollar you owe, say around 20 to 25 cents, then 50 cents on every dollar, then 75. The debt collector may still demand to collect the full amount that you owe, but in some cases they may also be willing to take a slightly lower amount that you propose.

What is the 11 word phrase to stop debt collectors?

If you need to take a break, you can use this 11 word phrase to stop debt collectors: “Please cease and desist all calls and contact with me, immediately.” Here is what you should do if you are being contacted by a debt collector.

Is it better to settle or pay in full?

Settling for Less Can Relieve Stress And it's important to know that paying your debt in full is the better option when it comes to your credit. If you can't pay in full, settling is better than defaulting on your debt and may relieve some stress for you.

Is it worth it to settle debt?

In general, paying off the total amount of debt you owe is a better option for your credit. An account that appears as "paid in full" on your credit report shows potential lenders that you have fulfilled your obligations as agreed, and that you paid the creditor the full amount due.

What should you not say to debt collectors?

Don't Give Information About Your Income, Debts, or Other Bills. Debt collectors can get some of this information from your credit report and may even use it to get you to make immediate payment. For example, they may say “I see that you're current on all your credit card payments.

Do settlements hurt your credit?

Yes, settling a debt instead of paying the full amount can affect your credit scores. When you settle an account, its balance is brought to zero, but your credit report will show the account was settled for less than the full amount.

What is a reasonable full and final settlement offer?

It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

What happens if a debt collector won't negotiate?

If the collection agency refuses to settle the debt with you, or if the agency or creditor agrees to settle, but you renig on your end of the agreement, the collection agency or creditor may decide to pursue more aggressive collection efforts against you, which may include a lawsuit.

How Much Do debt settlement companies charge?

a 15% to 25%Debt settlement companies typically charge a 15% to 25% fee to tackle your debt; this could be a percentage of the original amount of your debt or a percentage of the amount you've agreed to pay.

What is the common way of a debtor to negotiate to creditor to pay their debt s?

Aim to Pay 50% or Less of Your Unsecured Debt If you decide to try to settle your unsecured debts, aim to pay 50% or less. It might take some time to get to this point, but most unsecured creditors will agree to take around 30% to 50% of the debt. So, start with a lower offer—about 15%—and negotiate from there.

Will debt collectors settle for half?

Some want 75%–80% of what you owe. Others will take 50%, while others might settle for one-third or less. Proposing a lump-sum settlement is generally the best option—and the one most collectors will readily agree to—if you can afford it.

What is a reasonable full and final settlement offer?

It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

What is the process of loan settlement?

Loan settlement is the process of negotiating with your lender to pay off your loan for a lesser amount than what you originally borrowed. This can be done for various reasons, such as financial hardship or wanting to get out of debt quicker.

What percentage of a debt is typically accepted in a settlement?

A creditor may agree to accept anywhere from 40% to 50% of the debt you owe, but it could go as high as 80%. The original creditor is likely to be...

How does debt settlement affect your credit?

Debt settlement may hurt your credit score by more than 100 points and the settlement will stay on your credit report for seven years. Add this to...

Why is debt settlement considered a last resort?

Debt settlement is considered a last resort strategy because of the damage it does to your credit. Other options that require you to pay back the f...

Why do you do it yourself debt settlement?

A DIY settlement avoids the fees you might pay to a professional debt settlement company .

How many steps to take when you head down the DIY road of debt settlement?

Here are seven steps you can take when you head down the DIY road of debt settlement.

What are the downsides of DIY debt settlement?

Downsides of DIY Debt Settlement. Regardless of whether you take on the task yourself or reach out to a debt settlement company, you may face a tax burden if you do reach a settlement. If at least $600 in debt is forgiven, you’ll likely pay income taxes on the forgiven amount. Another downside to either DIY or professional debt settlement is ...

What to ask when entering a payment plan?

If you do enter a payment plan, ask whether the creditor will lower the interest rate on the debt to ease your financial burden. During your negotiations, maintain a written record of all your communication with a creditor. Last but not least, keep your cool and be honest.

How do debt collectors make money?

Debt collectors make money by collecting past-due debts that originated with a creditor, such as a credit card company. When dealing with debt collectors, be patient. It may take several attempts to get the type of settlement you’re comfortable with.

Why is debt settlement considered a last resort?

Debt settlement is considered a last resort strategy because of the damage it does to your credit. Other options that require you to pay back the full principal debt amount—and thus do not negatively affect your credit score—include debt consolidation and debt management plans.

Can you negotiate a DIY debt settlement?

If you choose to negotiate a DIY debt settlement, you don’t relinquish your personal control over the timing of the process.

What is do it yourself debt settlement?

With do-it-yourself debt settlement, you negotiate directly with your creditors in an effort to settle your debt for less than you originally owed.

What is the difference between debt settlement through a company and doing it yourself?

Time and cost are the main distinctions between debt settlement through a company and doing it yourself.

How much does a debt settlement company charge?

With a debt settlement company, you’ll likely pay a fee of 20% to 25% of the enrolled debt once you agree to a negotiated settlement and make at least one payment to the creditor from an account set up for this purpose, according to the Center for Responsible Lending.

What company did the CFPB take legal action against?

In 2013, the CFPB took legal action against one company, American Debt Settlement Solutions, saying it failed to settle any debt for 89% of its clients. The Florida-based company agreed to effectively shut down its operations, according to a court order.

What does "settled" mean on credit report?

Settled debts are generally marked as “Settled” or “Paid Settled,” which doesn’t look great on credit reports. Instead, you'll try to get your creditor to mark the settled account “Paid as Agreed” to minimize the damage.

How long can you be behind on a debt settlement?

Debt settlement is an option if your payments are at least 90 days late, but it’s more feasible when you're five or more months behind. But because you must continue to miss payments while negotiating, damage to your credit stacks up, and there is no guarantee that you’ll end up with a deal.

How long does it take to settle a debt?

While completing a plan through a company can take two and a half years or more, you may be able to settle your debts on your own within six months of going delinquent, according to debt settlement coach Michael Bovee.

What to do if you agree to a settlement?

If you agree to a repayment or settlement plan, record the plan and the debt collector’s promises. Those promises may include stopping collection efforts and ending or forgiving the debt once you have completed these payments. Get it in writing before you make a payment.

How to talk to a debt collector about your debt?

Explain your plan. When you talk to the debt collector, explain your financial situation. You may have more room to negotiate with a debt collector than you did with the original creditor. It can also help to work through a credit counselor or attorney.

How to contact a debt collector?

Any debt collector who contacts you to collect a debt must give you certain information when it first contacts you, or in writing within 5 days after contacting you, including: 1 The name of the creditor 2 The amount owed 3 That you can dispute the debt or request the name and address of the original creditor, if different from the current creditor.

How long does it take for a debt collector to contact you?

Any debt collector who contacts you to collect a debt must give you certain information when it first contacts you, or in writing within 5 days after contacting you, including: The name of the creditor. The amount owed. That you can dispute the debt or request the name and address of the original creditor, if different from the current creditor.

How long does a debt have to be paid before it can be sued?

The statute of limitations is the period when you can be sued. Most statutes of limitations fall in the three to six years range, although in some jurisdictions they may extend for longer.

What to do if you don't recognize the creditor?

If you don’t recognize the name of the creditor, you can ask what the original debt was for (credit card, mortgage foreclosure deficiency, etc.) and request the name of the original creditor. After you receive the debt collector’s response, compare it to your own records.

When will debt collectors have to give notice of eviction moratorium?

All debt collectors must follow the Fair Debt Collection Practices Act (FDCPA). This can include lawyers who collect rent for landlords. Starting on May 3, 2021, a debt collector may be required to give you notice about the federal CDC eviction moratorium.

Why is it important to negotiate a settlement?

It’s important when trying to negotiate a settlement that you have realistic goals. You’re not going to get out of debt for nothing – you’ll need to pay something to get your balances discharged. How much you end up paying depends on what you want to accomplish and who you’re negotiating with.

How much does a debt settlement pay?

The average debt settlement pays out roughly 48% of the original amount owed.

How to avoid credit damage?

However, there are several solutions you can negotiate which may allow you to avoid credit damage, including: Negotiating to list a credit account status as paid in full. Negotiating to re-age an account to remove delinquent payments. Using pay for delete to remove a debt collection account from your credit report.

What is the original creditor?

The original creditor – i.e. the credit card company that you have the account through. An in-house collections department, who may be trying to collect on a debt that’s past-due but not charged off yet. A third-party debt collector that’s attempting to collect on a charged off debt on behalf of the original creditor.

What is debt buyer?

A debt buyer, who purchased a portfolio of bad debts from the credit card company for a small percentage of each amount owed. A debt buyer is much more likely to settle for a lower amount. They paid pennies on the dollar to purchase your debt from the credit card company.

What to do if your debt is not matching your records?

Ask for the agency’s name, the name of the representative that you’re speaking with , and a contact call-back number. Then ask that they send you a written notice about the debt immediately.

What happens when you settle your debt?

When you settle your debt, you agree to pay less than what you owe. Depending on your situation, this may be the right form of debt relief for you. Unlike some other methods, you don’t always have to use a professional service to settle. The following steps will teach you how to negotiate debt settlement on your own.

How to settle debt for less than what you owe?

While many creditors might agree to settle your debt for less than what you owe, there’s no guarantee that debt settlement will work. If you’re considering trying it on your own, here’s a rough guide to the steps you may want to take: 1. Assess your situation. Create a list of your past-due accounts with the creditors’ names, how much you owe, ...

Why do creditors accept settlement offers?

Creditors can either send your accounts to collections, sue you for nonpayment, or sell the debt to a third-party debt buyer or collector.

What to do if a creditor doesn't settle?

If the creditor doesn't agree to settle, you may want to wait until it sells the debt and try again with the debt buyer or collection agency.

How long do you have to be late to settle a credit card?

For example, you may need to be at least 90 days late on an account before a creditor considers settling. Or, some creditors might not settle at all, and you’ll have to wait until the debt is sold to another company. Some creditors might also be more likely to sue you to collect an unpaid debt than others.

What to do if you feel like you're drowning in debt?

If you feel like you’re drowning in debt, the idea of settling for less money than you owe can be appealing. You could hire a debt settlement company that will work on your behalf to negotiate settlements with your creditors.

What to do if you think you have enough money to settle an account?

Once you think you have enough money saved up to settle an account, you can call your creditor and make an offer. In some cases, the creditor may have already sent you a settlement offer. You could accept the offer, or respond with a lower counteroffer.

How long do you have to be behind on credit card payments to settle?

Creditors generally don’t agree to settle an account if you’re only a few days late. You may need to be at least 90 or more days behind on your payments before a credit card company will even consider a settlement. By that point, your late payments have likely been reported to the credit bureaus.

How much does a debt settlement company charge?

According to Forbes, most debt settlement companies charge 15% to 25% for their services. It can be a percentage of either the total amount you owe or the settlement amount. Thus, if you settle $10,000 in debt for $5,000, you could owe another $750 to $2,500 in fees.

What does a debt settlement company do?

They promise to negotiate with your creditors to settle your debt in return for a sum that’s less than the total amount you owe. Lenders often agree to the settlement rather than risk having to write off your debt as a complete loss.

What are the pros and cons of debt settlement?

Pros & Cons of Debt Settlement. The obvious benefit of debt settlement is getting rid of your debt for less than you owe. According to Nolo, many creditors are willing to settle a debt for less than half the original amount.

How long does it take for a debt to settle?

Before taking on this challenge, figure out if debt settlement makes sense for you. Lenders are most likely to settle a debt when it’s at least 90 days past due, but it hasn’t yet gone to debt collection. Unsecured debt, such as credit card debt and unpaid medical bills, are typically easier to settle than mortgage debt, student loans, or back taxes.

Why do creditors have to negotiate with you?

The main reason creditors have to negotiate with you is that they fear losing their entire investment if they don’t. If they have to sell off your debt to a debt buyer, they’ll get very little, and if you go bankrupt, they could get nothing.

What is debt consolidation loan?

If you’re having trouble meeting the payments on several high-interest debts, perhaps a debt consolidation loan could bring those payments down to a manageable level. These loans roll several existing debts into a single loan with a lower interest rate.

What happens when you are under financial stress?

When you’re under a lot of financial stress, it’s frustrating if the person on the other end of the line doesn’t show any sympathy for your problems. However, taking that anger out on your creditor or a debt collector doesn’t get you anywhere. Most likely, they’ll just label you a problem customer and hang up.

How to get a final settlement agreement?

Getting your final debt settlement agreement in writing is essential. But it’s easier to reach agreements by talking on the phone. When you reach an agent, ask for someone who has the authority to make settlement agreements. You may have to speak to several people at the collection agency to get what you want.

What happens if you don't have a settlement agreement?

If you don’t have the settlement agreement in writing, the debt collector may cash your check but not fulfill its promises. When you follow up without written proof, the agency may refute your claim that it had promised to cancel the debt in response to your partial payment.

What happens if a debt collector doesn't prove the debt is yours?

If the debt collector can’t prove the debt is yours, it’s required by law to remove the debt from your credit history and stop contacting you about payment. However, if the collection agency validates the debt as yours, you’ll need to find another way to resolve the debt — possibly by reaching a debt settlement agreement.

What to do when you can't afford to pay your debt?

When you can’t afford to pay your debts, you may want to negotiate a debt settlement agreement with your creditors or with a collection agency. Negotiating a settlement could close your past-due account, but even a fair settlement has some drawbacks. You may need to part with a lump sum of cash, for example.

How to prove debt is yours?

Step 1: Validate The Debt is Really Yours. You don’t need to settle the debt when the debt is not yours, to begin with. Federal laws require debt collectors who contact you about debt to prove the debt is yours — if you ask within 30 days of the collector’s first contact with you.

Why is partial payment bad?

This is bad because you’re exposing yourself to more legal action unnecessarily. This can also extend the account’s lifespan on your credit report.

How to continue settlement discussions?

You can continue the settlement discussions by making another counteroffer of your own.

What is debt negotiation?

In a Nutshell: Debt negotiation is a practice that allows a person to pay a lump sum that is typically less than the amount they owe to resolve, or “settle,” a debt. It’s a program that’s usually offered by third-party companies, like Golden Financial Services and also debt settlement lawyers. Debt negotiators can reduce a person’s debt by ...

What is debt settlement?

Debt settlement programs provide clients with a single payment every month. That payment does not get disbursed to the creditors every month but instead goes directly into a “special purpose savings account.”. The consumer has full control over this savings account, but the settlement company can also monitor it.

What is the best alternative to debt settlement?

Debt collection agencies often can’t prove a debt is valid, resulting in the debt becoming “legally uncollectible”.

How do you qualify for debt settlement?

To qualify for debt settlement call Golden Financial Services Toll-Free: (866) 376-9846!

How does a credit card settlement work?

The credit card settlement process reduces a person’s debt, by negotiating with the creditor to lower the debt in exchange for a one-time lump-sum payment. The debtor and creditor agree on a reduced balance that will be regarded as “payment in full”.

What happens when you pay a debt in lump sum?

One by one, each debt gets negotiated down and settled for a fraction of the balance. When it’s time to pay the creditor a lump sum payoff (i.e., the settlement amount), the client must agree to the settlement first.

How does settling a debt affect credit?

How does settling a debt affect a person’s credit? Settlement programs can result in credit scores going down by up to 100-200 points, but in other cases , credit scores may not be negatively affected at all.

What to do if you can't get a debt collector to accept a lower payment?

Even if you can't get the collector to agree to accept a lower payment, you may be able to work out an arrangement to pay off the debt in installments. Knowing how to negotiate with debt collectors will help you work out a payment solution that helps you take care of the debt collection account for good. 1.

How to contact debt collectors?

Here are a few things you should know: 4 1 Debt collectors can only call you between 8 a.m. and 9 p.m. 2 They can't harass you or use profane language when speaking to you. 3 They can't threaten to take action that's illegal or that they don't intend to follow through with. 4 Debt collectors can only contact your employer, family members, and friends to contact information about you.

What to do if a credit collector doesn't send proof?

Otherwise, if the collector doesn't send sufficient proof, send the collector a cease and desist letter asking they stop contacting you and dispute the debt with the credit bureaus. 8

How long does it take for a debt collector to send you a notice?

5 Approach all debt collections with a healthy dose of skepticism. Within five days of contacting you, the collectors must send you a debt validation notice.

How do debt collectors work?

Debt collections can happen to even the most financially responsible consumers. A bill may slip your mind, you may have a dispute with the creditor over how much you really owe, or billing statements can get lost in the mail before you ever know the debt exists.

How long does it take for a debt validation notice to be sent?

Within five days of contacting you, the collectors must send you a debt validation notice. This notice lists how much money you owe, names the entity to which you owe it, and details steps you can take if you believe there's been a mistake. 6

How do junk debt buyers make money?

Or, junk debt buyers earn profits on debts they've purchased for just pennies on the dollar. 2 . Collectors only make money when consumers pay the debt. They can't seize property or take money from consumer bank accounts unless they sue and obtain a court judgment and permission to garnish the consumer's wages. 3 . 2.