How to Settle Taxes Owed

- File Back Taxes —The IRS only accepts settlement offers if you have filed all your required tax returns. If you have...

- Amend Ghost Returns — In some cases, if you have unfiled back taxes, the IRS creates a substitute for return (SFR) for...

- Apply for a Settlement — Once you are in tax compliance, you can start to apply for a settlement. A tax...

Full Answer

Do you have to pay taxes on a settlement?

Whether you need to pay taxes on a lawsuit settlement is dependent on the circumstances of the case. You’ll have to determine the nature of the claim and whether it was paid to you. If it was a settlement of an accident, it’ll be treated as ordinary income. Its value will be taxable if the plaintiff made it whole and won’t receive tax breaks.

Do you pay taxes on a settlement?

There are many factors to consider when determining whether you need to pay tax on your settlement. Legal settlements can include lost wages, damages for emotional distress, and attorney fees. All of these items are taxable. While the amount of your award may be large, you will still need to report them on the correct forms.

Do I have to pay tax on a settlement agreement?

Many people believe that if money is paid under a settlement agreement it must be tax free. However, this not necessarily the case. The key issue is the nature of the payment. Make sure you obtain legal advice about which payments are taxable and which are not. Which payments are taxable and which are not?

Will I have to pay taxes on my settlement?

While there are times that you are not required to pay tax on your settlement, there are also cases in which you will be required to fork over a percentage. As long as you know your way around the law, you can minimize how much you have to pay in the end. In Court for Personal Injury?

How Does a Tax Settlement Work?

What is a tax settlement?

How long do you have to pay back taxes?

What is partial payment installment agreement?

How to settle taxes owed?

What happens if you default on a settlement offer?

Why do you settle taxes if you don't qualify?

See 2 more

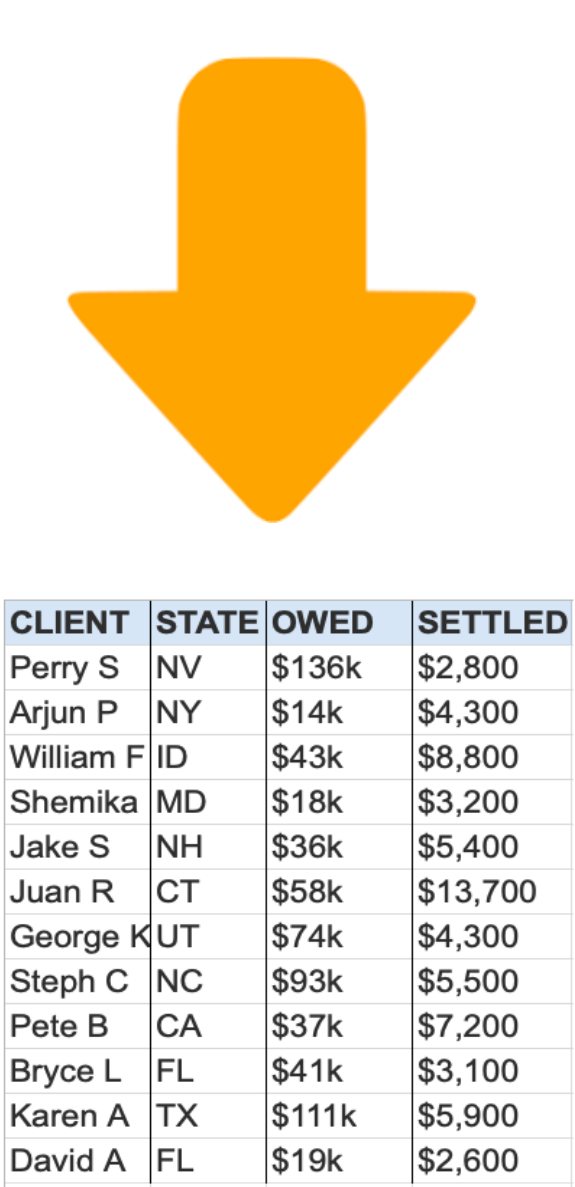

How much will the IRS usually settle for?

Each year, the Internal Revenue Service (IRS) approves countless Offers in Compromise with taxpayers regarding their past-due tax payments. Basically, the IRS decreases the tax obligation debt owed by a taxpayer in exchange for a lump-sum settlement. The average Offer in Compromise the IRS approved in 2020 was $16,176.

What is the best way to settle tax debt?

An offer in compromise allows you to settle your tax debt for less than the full amount you owe. It may be a legitimate option if you can't pay your full tax liability or doing so creates a financial hardship....Apply With the New Form 656Ability to pay.Income.Expenses.Asset equity.

How can I get my tax debt forgiven?

You will need to apply for tax debt relief and be accepted into an IRS debt forgiveness program. You must then agree to the terms of your IRS debt forgiveness program. In order to monitor your tax debt forgiveness, the IRS will continually assess your financial situation.

Is there a one time tax forgiveness?

One-time forgiveness, otherwise known as penalty abatement, is an IRS program that waives any penalties facing taxpayers who have made an error in filing an income tax return or paying on time. This program isn't for you if you're notoriously late on filing taxes or have multiple unresolved penalties.

What do I do if I owe the IRS over 10000?

What to do if you owe the IRSSet up an installment agreement with the IRS. Taxpayers can set up IRS payment plans, called installment agreements. ... Request a short-term extension to pay the full balance. ... Apply for a hardship extension to pay taxes. ... Get a personal loan. ... Borrow from your 401(k). ... Use a debit/credit card.

What happens if you owe the IRS more than $50000?

If you owe more than $50,000, you may still qualify for an installment agreement, but you will need to complete a Collection Information Statement, Form 433-A. The IRS offers various electronic payment options to make a full or partial payment with your tax return.

Who qualifies for IRS Fresh Start?

People who qualify for the program Having IRS debt of fifty thousand dollars or less, or the ability to repay most of the amount. Being able to repay the debt over a span of 5 years or less. Not having fallen behind on IRS tax payments before. Being ready to pay as per the direct payment structure.

What if I owe the IRS and can't pay?

The IRS offers payment alternatives if taxpayers can't pay what they owe in full. A short-term payment plan may be an option. Taxpayers can ask for a short-term payment plan for up to 120 days. A user fee doesn't apply to short-term payment plans.

Can't afford to pay back taxes?

If you don't qualify for an online payment plan, you may also request an installment agreement (IA) by submitting Form 9465, Installment Agreement RequestPDF, with the IRS. If the IRS approves your IA, a setup fee may apply depending on your income. Refer to Tax Topic No. 202, Tax Payment Options.

What is the lowest payment the IRS will take?

What is the minimum monthly payment on an IRS installment agreement?Amount of tax debtMinimum monthly payment$10,000 or lessNo minimum$10,000 to $25,000Total debt/72$25,000 to $50,000Total debt/72Over $50,000No minimumMay 16, 2022

What is the IRS 6 year rule?

6 years - If you don't report income that you should have reported, and it's more than 25% of the gross income shown on the return, or it's attributable to foreign financial assets and is more than $5,000, the time to assess tax is 6 years from the date you filed the return.

What is the 2 out of 5 year rule?

During the 5 years before you sell your home, you must have at least: 2 years of ownership and. 2 years of use as a primary residence.

Can tax debt be negotiated?

Can You Negotiate Tax Debt? The IRS will sometimes let you pay much less than you actually owe in taxes using an option called Offer in Compromise (OIC). To qualify, you must convince the IRS that you're unable to afford what you owe. You can make this reduced payment using short-term installments or one lump sum.

Can you settle back taxes for less?

Yes – If Your Circumstances Fit. The IRS does have the authority to write off all or some of your tax debt and settle with you for less than you owe. This is called an offer in compromise, or OIC.

Does IRS forgive penalties and interest?

We charge interest on penalties. Interest increases the amount you owe until you pay your balance in full. We'll automatically reduce or remove the related interest if any of your penalties are reduced or removed.

How does an IRS offer in compromise work?

An offer in compromise is an agreement between a taxpayer and the IRS that settles a tax debt for less than the full amount owed. An offer in compromise is an option when a taxpayer can't pay their full tax liability. It is also an option when paying the entire tax bill would cause the taxpayer a financial hardship.

What is partial payment installment?

A Partial Payment Installment Agreement is when you make payments based on what you can afford rather than the monthly amount required to satisfy the taxes in full before the CSEDs expire. The balance gets reduced as the statute of collections comes into effect. Under that statute of limitations on taxes expires after a certain period of time (generally 10 years from the date it is assessed). As the expiration date hits, that tax amount owed is erased, and you are no longer responsible for it.

Can bankruptcy eliminate taxes?

Bankruptcy can sometimes eliminate taxes owed. You can eliminate certain taxes through Chapter 7, but it depends on the age of the taxes and several other factors. Bankruptcy is not always the best option if you solely looking at it to discharge taxes. Consequently, it generally negatively impacts your credit and forces you to liquidate assets. If you are considering this option, contact a bankruptcy attorney.

What to do if you owe IRS money?

If you owe the IRS money, you may be able to negotiate a settlement in order to resolve the debt. This can be a tricky process, so you want to consider hiring a professional to handle the offer in compromise.

What happens if you owe back taxes to the IRS?

When you owe back taxes to the IRS, you’re indebted to the government itself – and there are very few ways out of that debt. In some cases, taxpayers can argue that the debt they’re facing isn’t valid and argue doubt as to their own liability.

When neither a payment plan nor an offer in compromise is in the cards, what is your best bet?

When neither a payment plan nor an offer in compromise is in the cards, your best bet might be to just focus on fighting back against the IRS’s collection actions, until you can get back on your feet.

Can you negotiate with the IRS about debt?

There are very few ways around a debt with the IRS. The government expects you to pay them one way or another, and even in the most desperate cases, your best bet is to negotiate for a reduced debt rather than a full pardon. Working with experienced tax professionals is key, as the IRS can be particularly picky about tax debt settlements and won’t accept just any offer.

Is a compromise a part of negotiating a tax settlement?

Drafting an effective offer in compromise is still just one part of negotiating a tax settlement with the IRS, albeit a crucial one.

Can you pay less than what you owe?

It’s important to remember that while an offer in compromise can let you pay less than what you ultimately owe, the IRS can be quite meticulous – and time spent investing in an offer sure to be rejected is ultimately time you could have saved by pursuing a different approach.

Is it hard to negotiate a tax settlement with the IRS?

Negotiating a tax settlement with the IRS can be a stressful and difficult process. It’s important to pick the right partners for the job, so you can put this chapter of your life behind you once and for all.

How Does Tax Settlement Work?

There are two strategies for obtaining a tax settlement. The first is to try to negotiate with the IRS for less than what you owe.

What Is a Tax Settlement?

A tax settlement, you may presume, entails working out a problem in a courtroom –but the majority of tax debt settlements are as simple as filling out the proper IRS forms.

What is the tax rule for settlements?

Tax Implications of Settlements and Judgments. The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code. IRC Section 104 provides an exclusion ...

What is an interview with a taxpayer?

Interview the taxpayer to determine whether the taxpayer provided any type of settlement payment to any of their employees (past or present).

What is employment related lawsuit?

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example lost wages, business income and benefits, are not excludable form gross income unless a personal physical injury caused such loss.

What is a 1.104-1 C?

Section 1.104-1 (c) defines damages received on account of personal physical injuries or physical sickness to mean an amount received (other than workers' compensation) through prosecution of a legal suit or action, or through a settlement agreement entered into in lieu of prosecution.

What is the exception to gross income?

For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury.

Is a settlement agreement taxable?

In some cases, a tax provision in the settlement agreement characterizing the payment can result in their exclusion from taxable income. The IRS is reluctant to override the intent of the parties. If the settlement agreement is silent as to whether the damages are taxable, the IRS will look to the intent of the payor to characterize the payments and determine the Form 1099 reporting requirements.

Is emotional distress taxable?

Damages received for non-physical injury such as emotional distress, defamation and humiliation, although generally includable in gross income, are not subject to Federal employment taxes. Emotional distress recovery must be on account of (attributed to) personal physical injuries or sickness unless the amount is for reimbursement ...

What happens if you accept a tax offer?

You must meet all the Offer Terms listed in Section 7 of Form 656, including filing all required tax returns and making all payments; Any refunds due within the calendar year in which your offer is accepted will be applied to your tax debt;

How long does it take for an IRS offer to be accepted?

Your offer is automatically accepted if the IRS does not make a determination within two years of the IRS receipt date.

Do you have to pay the application fee for low income certification?

If accepted, continue to pay monthly until it is paid in full. If you meet the Low Income Certification guidelines, you do not have to send the application fee or the initial payment and you will not need to make monthly installments during the evaluation of your offer. See your application package for details.

Does the IRS return an OIC?

The IRS will return any newly filed Offer in Compromise (OIC) application if you have not filed all required tax returns and have not made any required estimated payments. Any application fee included with the OIC will also be returned. Any initial payment required with the returned application will be applied to reduce your balance due. This policy does not apply to current year tax returns if there is a valid extension on file.

How Does a Tax Settlement Work?

You determine which type of settlement you want and submit the application forms to the IRS. The IRS reviews your application and requests more information if needed. If the IRS does not accept your settlement offer, you need to make alternative arrangements. Otherwise, collection activity will resume. If the IRS accepts your settlement offer, you just make the payments as arranged.

What is a tax settlement?

A tax settlement is when you pay less than you owe and the IRS erases the rest of your tax amount owed. If you don’t have enough money to pay in full or make payments, the IRS may let you settle. The IRS also reverses penalties for qualifying taxpayers.

How long do you have to pay back taxes?

If you personally owe less than $100,000 or if your business owes less than $25,000, it is relatively easy to get an installment agreement. As of 2017, the IRS gives taxpayers up to 84 months (7 years) to complete their payment plans.

What is partial payment installment agreement?

A partial payment installment agreement allows you to make monthly payments on your tax liability. You make payments over several years, but you don’t pay all of the taxes owed. As you make payments, some of the taxes owed expire. That happens on the collection statute expiration date.

How to settle taxes owed?

These are the basic steps you need to follow if you want to settle taxes owed. File Back Taxes —The IRS only accepts settlement offers if you have filed all your required tax returns. If you have unfiled returns, make sure to file those returns before applying.

What happens if you default on a settlement offer?

At that point, you are in good standing with the IRS, but if you default on the terms of the agreement, the IRS may revoke the settlement offer . To explain, imagine you owe the IRS $20,000, and the IRS agrees to accept a $5,000 settlement.

Why do you settle taxes if you don't qualify?

If you don’t qualify for a tax settlement for less money, then it will ensure you are paying back a lower amount of taxes and penalties that are due.