Where to enter compensation on 1040?

Where to enter interest on 1099-INT?

Is legal settlement taxable?

About this website

How do I report a settlement to the IRS?

Attach to your return a statement showing the entire settlement amount less related medical costs not previously deducted and medical costs deducted for which there was no tax benefit. The net taxable amount should be reported as “Other Income” on line 8z of Form 1040, Schedule 1.

Do I have to report settlement money to IRS?

The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code.

Are settlement payments taxable income?

Settlement money and damages collected from a lawsuit are considered income, which means the IRS will generally tax that money. However, personal injury settlements are an exception (most notably: car accident settlements and slip and fall settlements are nontaxable).

Are legal settlements 1099 reportable?

Money reported as gross proceeds paid to a lawyer is not classified as income by the IRS. That is, unlike Form 1099-MISC box 3 (other income) or Form 1099-NEC, the IRS does not match the taxpayer ID number for gross proceeds paid to an attorney with the lawyer's tax return to be sure it is income.

How can I avoid paying taxes on a settlement?

How to Avoid Paying Taxes on a Lawsuit SettlementPhysical injury or sickness. ... Emotional distress may be taxable. ... Medical expenses. ... Punitive damages are taxable. ... Contingency fees may be taxable. ... Negotiate the amount of the 1099 income before you finalize the settlement. ... Allocate damages to reduce taxes.More items...•

Are settlements tax deductible?

Generally, if a claim arises from acts performed by a taxpayer in the ordinary course of its business operations, settlement payments and payments made pursuant to court judgments related to the claim are deductible under section 162.

Why is a W 9 required for settlement?

The Form W-9 is a means to ensure that the payee of the settlement is reporting its full income. Attorneys are frequently asked to supply their own Taxpayer Identification Numbers and other information to the liability carrier paying a settlement.

Is a lump sum payment in a divorce settlement taxable?

Generally, lump-sum divorce settlements are not taxable for the recipient. If the lump-sum payment is an alimony payment, it is not deductible for the person who makes the payment and is not considered income for the recipient.

Are property insurance settlements taxable?

Home insurance payouts are not taxable because they aren't considered income—you're simply restoring the original state of your assets. The IRS taxes your wages and any source of income that increases your wealth. Unless your insurance company overpays you, your payout isn't considered income.

Do you need a 1099 for settlement payments?

If your legal settlement represents tax-free proceeds, like for physical injury, then you won't get a 1099: that money isn't taxable. There is one exception for taxable settlements too. If all or part of your settlement was for back wages from a W-2 job, then you wouldn't get a 1099-MISC for that portion.

Do you get a 1099 for insurance settlement?

If you do have to pay taxes on an insurance claim, you'll receive a 1099 form to help you file.

Are property damage settlements 1099 reportable?

Although tax provisions are not controlling, the IRS is generally reluctant to override the intent of the parties. Accordingly, any settlement payments made expressly for nontaxable damages are excluded from the 1099 reporting requirements.

Is a lump sum payment in a divorce settlement taxable?

Generally, lump-sum divorce settlements are not taxable for the recipient. If the lump-sum payment is an alimony payment, it is not deductible for the person who makes the payment and is not considered income for the recipient.

Why is a W 9 required for settlement?

The Form W-9 is a means to ensure that the payee of the settlement is reporting its full income. Attorneys are frequently asked to supply their own Taxpayer Identification Numbers and other information to the liability carrier paying a settlement.

Do you have to pay taxes on a lawsuit settlement in Florida?

In most cases in Florida, a settlement will not be taxed. However, there are certain types of damages that could be considered taxable. These include the following: Punitive Damages – These are damages that go beyond your initial loss.

Are lawsuit awards taxable?

General rule relative to taxability of amounts received from lawsuit settlements is IRC §61 that states that all income is taxable from whatever source derived, unless exempted by another section of the Code. May cause or constitute, but is not necessarily, a personal injury.

Where do I enter the settlement income amount and attorney ... - Intuit

This was an employer discrimination lawsuit. The settlement amount was $107,500. Total to attorney was $64,089.71(attorney fees:$51,750 + costs advanced by attorney:$12,339.71). I didn't receive a 1099 from the attorney. I received a check for $43,410.29 from my attorney. After reading some que...

Publication 4345 (Rev. 11-2021) - IRS tax forms

Lost wages or lost profits ‧ If you receive a settlement in an employment-related lawsuit; for example, for unlawful discrimination or involuntary termination, the portion of the proceeds that is for lost wages (i.e., severance pay, back

Tax Implications of Settlements and Judgments

IRC Section 104 provides an exclusion from taxable income with respect to lawsuits, settlements and awards. However, the facts and circumstances surrounding each settlement payment must be considered.

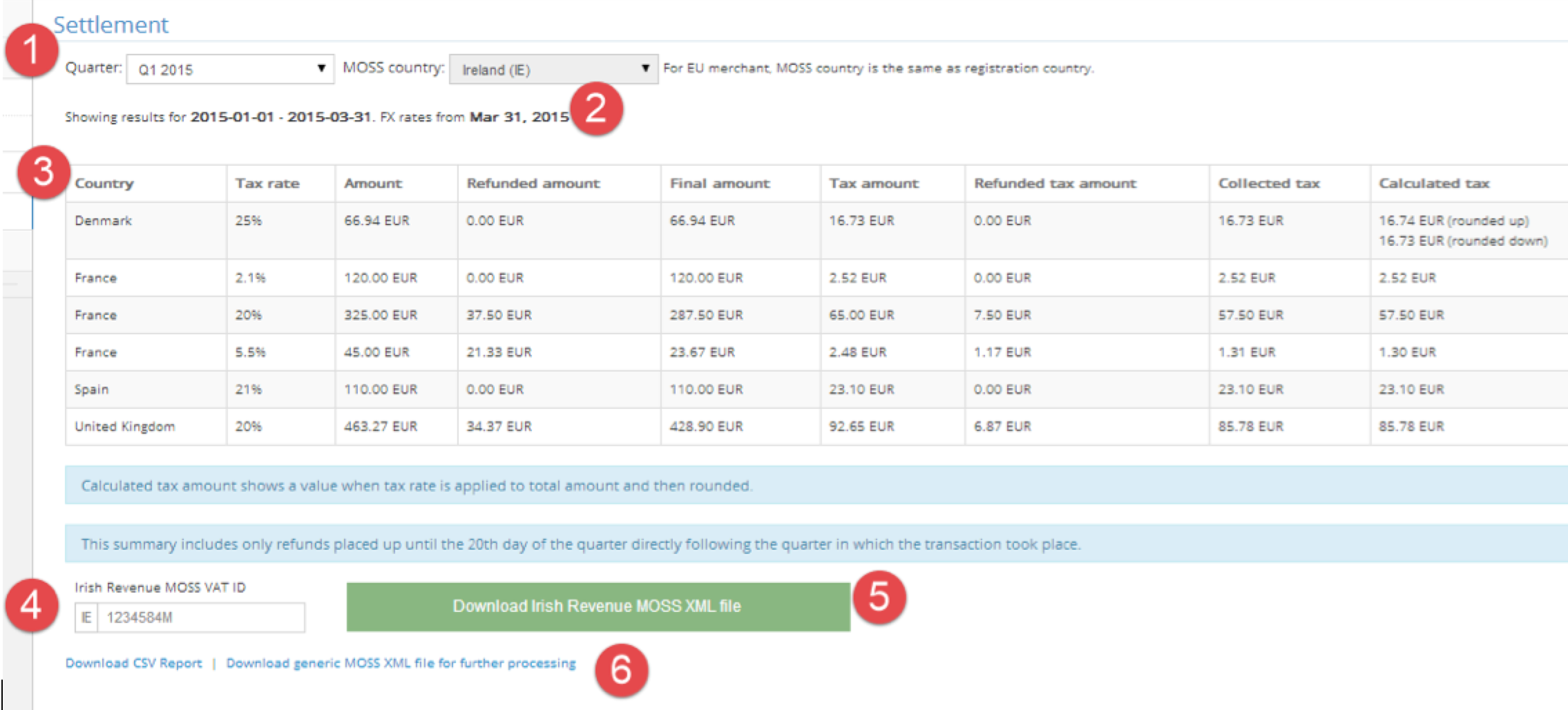

Report Delivery Schedule

There are daily, weekly, and monthly settlement reports. Our settlement process is based on Coordinated Universal Time (UTC), but we'll discuss the timeline in terms of Pacific Daylight Time (PDT) to give a sense of when these events may occur in your timezone.

How to Reconcile Your Settlements

The date of the settlement file is the date we initiated the ACH transfer to your bank account, which is a different date than when the charge was processed.

What should a settlement agent do?

The settlement agent should be able to help you sort out things.

Do you report capital gains on Schedule D?

If you've already sold the shares , however, you're supposed to report the payment as a capital gain on Schedule D for the year you get the check.

What is the tax rule for settlements?

Tax Implications of Settlements and Judgments. The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code. IRC Section 104 provides an exclusion ...

What is employment related lawsuit?

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example lost wages, business income and benefits, are not excludable form gross income unless a personal physical injury caused such loss.

What is an interview with a taxpayer?

Interview the taxpayer to determine whether the taxpayer provided any type of settlement payment to any of their employees (past or present).

Is a settlement agreement taxable?

In some cases, a tax provision in the settlement agreement characterizing the payment can result in their exclusion from taxable income. The IRS is reluctant to override the intent of the parties. If the settlement agreement is silent as to whether the damages are taxable, the IRS will look to the intent of the payor to characterize the payments and determine the Form 1099 reporting requirements.

Does gross income include damages?

IRC Section 104 explains that gross income does not include damages received on account of personal physical injuries and physical injuries.

Is emotional distress excludable from gross income?

96-65 - Under current Section 104 (a) (2) of the Code, back pay and damages for emotional distress received to satisfy a claim for disparate treatment employment discrimination under Title VII of the 1964 Civil Rights Act are not excludable from gross income . Under former Section 104 (a) (2), back pay received to satisfy such a claim was not excludable from gross income, but damages received for emotional distress are excludable. Rev. Rul. 72-342, 84-92, and 93-88 obsoleted. Notice 95-45 superseded. Rev. Proc. 96-3 modified.

Why should settlement agreements be taxed?

Because different types of settlements are taxed differently, your settlement agreement should designate how the proceeds should be taxed—whether as amounts paid as wages, other damages, or attorney fees.

How much is a 1099 settlement?

What You Need to Know. Are Legal Settlements 1099 Reportable? What You Need to Know. In 2019, the average legal settlement was $27.4 million, according to the National Law Review, with 57% of all lawsuits settling for between $5 million and $25 million.

What to report on 1099-MISC?

What to Report on Your Form 1099-MISC. If you receive a court settlement in a lawsuit, then the IRS requires that the payor send the receiving party an IRS Form 1099-MISC for taxable legal settlements (if more than $600 is sent from the payer to a claimant in a calendar year). Box 3 of Form 1099-MISC identifies "other income," which includes ...

How much money did the IRS settle in 2019?

In 2019, the average legal settlement was $27.4 million, according to the National Law Review, with 57% of all lawsuits settling for between $5 million and $25 million. However, many plaintiffs are surprised after they win or settle a case that their proceeds may be reportable for taxes. The Internal Revenue Service (IRS) simply won't let you collect a large amount of money without sharing that information (and proceeds to a degree) with the agency.

What form do you report lost wages on?

In this example, you'll report lost wages on a Form W-2, the emotional distress damages on a Form 1099-MISC (since they are taxable), and attorney fees on a Form 1099-NEC. As Benjamin Franklin said after the U.S. Constitution was signed, "in this world nothing can be said to be certain, except death and taxes.".

What happens if you get paid with contingent fee?

If your attorney or law firm was paid with a contingent fee in pursuing your legal settlement check or performing legal services, you will be treated as receiving the total amount of the proceeds, even if a portion of the settlement is paid to your attorney.

Do you have to pay taxes on a 1099 settlement?

Where many plaintiff's 1099 attorneys now take up to 40% of the settlement in legal fees, the full amount of the settlement may need to be reported to the IRS on your income tax. And in some cases, you'll need to pay taxes on those proceeds as well. Let's look at the reporting and taxability rules regarding legal settlements in more detail as ...

When reporting a potential settlement, judgment, award, or other payment related to exposure, ingestion, or implantation?

When reporting a potential settlement, judgment, award, or other payment related to exposure, ingestion, or implantation, the date of first exposure/date of first ingestion/date of implantation is the date that MUST be reported as the DOI.

Who must report a claim to Medicare?

Reporting a Case. Medicare beneficiaries, through their attorney or otherwise, must notify Medicare when a claim is made against an alleged tortfeasor with liability insurance (including self-insurance), no-fault insurance or against Workers’ Compensation (WC). This obligation is fulfilled by reporting the case in the Medicare Secondary Payor ...

How to get BCRC contact information?

Contact information for the BCRC may be obtained by clicking the Contacts link. When reporting a case in the MSPRP or contacting the BCRC, the following information is needed: Beneficiary Information: Once all information has been obtained, the BCRC will apply it to Medicare’s record.

What is a BCRC letter?

If Medicare is pursuing recovery directly from the beneficiary, the BCRC will issue a Rights and Responsibilities letter and brochure. The Rights and Responsibilities letter is mailed to all parties associated with the case.

What is a rights and responsibilities letter?

The Rights and Responsibilities letter is mailed to all parties associated with the case. The Rights and Responsibilities letter explains: What happens when the beneficiary has Medicare and files an insurance or workers’ compensation claim; What information is needed from the beneficiary;

What is a lawsuit against insurance companies?

Lawsuits against insurance companies, finance companies, etc., for negligence, fraud, breach of contract, etc., can include a variety of claims, and therefore can produce a variety of types of awards/settlements.

What is employment related lawsuit?

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example, lost wages, business income, and benefits, are not excludable from gross income unless a personal physical injury caused such loss

What is the IRC 6041?

IRC §§ 6041(a) and 6045(f), with regard to payments to attorneys, generally requires all persons engaged in a trade or business and making payment in the course of such trade or business to another person of fixed or determinable gains, profits, and income of $600 or more in a calendar year to file an information return with the Service. IRC § 6041(d) provides that each person required to make the return described in IRC § 6041(a) shall furnish to each person for whom a return is required a payee statement.

What is an interview with a taxpayer?

An interview with the taxpayer can provide information regarding the case to assist you in making a determination of the depth of your probe of the issue. Questions may include, but are not limited to, the following:

What is discrimination suit?

Discrimination suits usually are brought alleging infringements in the areas of age, race, gender, religion or disability. These types of cases can generate compensatory, contractual and punitive awards, none of which are excludable under IRC § 104(a)(2).

What is damages intended to compensate the taxpayer for a loss?

Damages intended to compensate the taxpayer for a loss, i.e., payment to compensate the injured party for the injury sustained, and nothing more. This loss may be purely economic, for example, arising out of a contract, or personal, for example, sustained by virtue of a physical injury.

When was the IRC 104(a)(2) amended?

Prior to the 1996 amendment, § 104(a)(2) did not include the word “physical” with regard to “personal injuries or sickness.” As a result, many taxpayers were allowed to exclude income received prior to the amendment‟s August 21, 1996 effective date on account of non-physical injuries and sickness. When reviewing litigation on this issue, examiners should consider the date in which the settlement was received before relying on specific case law for their position.

What if the lawyer is beyond merely receiving the money and dividing the lawyer’s and client’s shares?

What if the lawyer is beyond merely receiving the money and dividing the lawyer’s and client’s shares? Under IRS regulations, if lawyers take on too big a role and exercise management and oversight of client monies, they become “payors” and as such are required to issue Forms 1099 when they disburse funds.

How does Larry Lawyer earn a contingent fee?

Example 1: Larry Lawyer earns a contingent fee by helping Cathy Client sue her bank. The settlement check is payable jointly to Larry and Cathy. If the bank doesn’t know the Larry/Cathy split, it must issue two Forms 1099 to both Larry and Cathy, each for the full amount. When Larry cuts Cathy a check for her share, he need not issue a form.

Why do lawyers send 1099s?

Copies go to state tax authorities, which are useful in collecting state tax revenues. Lawyers receive and send more Forms 1099 than most people, in part due to tax laws that single them out. Lawyers make good audit subjects because they often handle client funds. They also tend to have significant income.

When do you get a 1099 from a law firm?

Forms 1099 are generally issued in January of the year after payment. In general, they must be dispatched to the taxpayer and IRS by the last day of January.

Who must file a 1099?

Lawyers must issue Forms 1099 to expert witnesses, jury consultants , investigators, and even co-counsel where services are performed and the payment is $600 or more. A notable exception from the normal $600 rule is payments to corporations.

Do attorneys have to report 1099?

The tax code requires companies making payments to attorneys to report the payments to the IRS on a Form 1099. Each person engaged in business and making a payment of $600 or more for services must report it on a Form 1099. The rule is cumulative, so whereas one payment of $500 would not trigger the rule, two payments of $500 to a single payee ...

Can a plaintiff lawyer issue a 1099 to Jones Law Firm?

Seeking to help their clients avoid receiving Forms 1099, some plaintiff lawyers ask the defendant for one check payable to the “Jones Law Firm Trust Account.” Many defendants are willing to issue a single Form 1099 only to the Jones Law Firm in this situation. Technically, however, Treasury Regulations dictate that you should treat this Jones Law Firm Trust Account check just like a joint check payable to lawyer and client. That means two Forms 1099, each in the full amount, are required.

Where to enter compensation on 1040?

Enter all compensation that qualifies as ordinary income in Line 21 on Form 1040 for a personal settlement or Line 6 of Schedule C for a business settlement. Do not include any compensation for physical injury or physical sickness unless you itemized your deductions and deducted medical expenses related to the injury in prior tax years. If the settlement was personal, write the word "Settlement" in the explanation line on Line 21.

Where to enter interest on 1099-INT?

Enter any interest received from Box 3 on Form 1099-INT in Line 8a on Form 1040 if the settlement was for your personal return or Line 6 on Schedule C for your business return.

Is legal settlement taxable?

Some, but not all, of the compensation you receive from a legal settlement may be taxable. Whether the Internal Revenue Service taxes the assets your business receives depends on what loss the settlement replaces.

Contents

Report Delivery Schedule

- There are daily, weekly, and monthly settlement reports. Our settlement process is based on Coordinated Universal Time (UTC), but we'll discuss the timeline in terms of Pacific Daylight Time (PDT) to give a sense of when these events may occur in your timezone. Please note that if you are expecting a large number of reports, you may experience delays in delivery times. Daily Repo…

Accessing Your Reports

- There are 3 ways to access your settlement reports. 1. Dashboard 1. Sign in to your Merchant Dashboard 2. On the lefthand sidebar, click Settlements. For each date on the settlement page, you can view total sales, refunds, total fees, and total amount settled. The date listed is when our lending partners initiate an ACH transfer for that payment. I...

How to Reconcile Your Settlements

- The date of the settlement file is the date we initiated the ACH transfer to your bank account, which is a different date than when the charge was processed.

- Take the sum of all the amounts in the total_settled column that have the same Deposit ID. This sum should equal the amount of a deposit made into your bank account. You may have multiple deposits...

- The date of the settlement file is the date we initiated the ACH transfer to your bank account, which is a different date than when the charge was processed.

- Take the sum of all the amounts in the total_settled column that have the same Deposit ID. This sum should equal the amount of a deposit made into your bank account. You may have multiple deposits...

- If you use Order ID, take the sum of all the amounts with the same Order ID across different reports to calculate the final state of that order.

- You can optionally map each Transaction_id to your accounts payable or accounts receivable in your accounting system.

IRC Section and Treas. Regulation

- IRC Section 61explains that all amounts from any source are included in gross income unless a specific exception exists. For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury. IRC Section 104explains that gross income does not include damages received on account of personal phys…

Resources

- CC PMTA 2009-035 – October 22, 2008PDFIncome and Employment Tax Consequences and Proper Reporting of Employment-Related Judgments and Settlements Publication 4345, Settlements – TaxabilityPDFThis publication will be used to educate taxpayers of tax implications when they receive a settlement check (award) from a class action lawsuit. Rev. Rul. 85-97 - The …

Analysis

- Awards and settlements can be divided into two distinct groups to determine whether the payments are taxable or non-taxable. The first group includes claims relating to physical injuries, and the second group is for claims relating to non-physical injuries. Within these two groups, the claims usually fall into three categories: 1. Actual damages re...

Issue Indicators Or Audit Tips

- Research public sources that would indicate that the taxpayer has been party to suits or claims. Interview the taxpayer to determine whether the taxpayer provided any type of settlement payment to any of their employees (past or present).