The Body of the Letter

- First Paragraph. Your opening paragraph should quickly state the purpose of your letter, which is a proposal to settle the account for less than the full amount.

- Second Paragraph. You’ll use this paragraph to present the details of your settlement offer. ...

- Final Paragraph. ...

- Your Signature. ...

How to negotiate a settlement with a collection agency?

Negotiate a settlement with the debt collection agency. You can negotiate in 2 ways. A debt collection agency may contact you with a settlement offer. You can contact the debt collection agency in writing and offer a settlement figure. Generally, you should start the negotiation by offering approximately 25 percent of the debt.

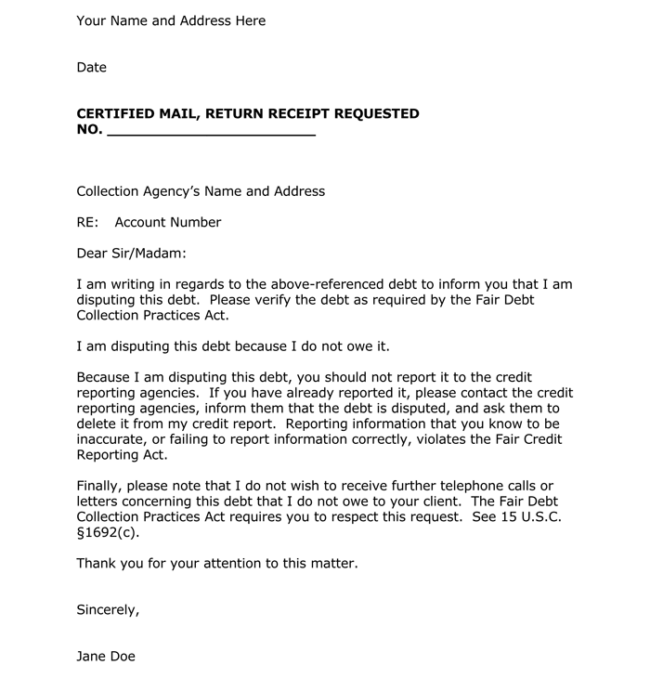

How to write a dispute letter to a collection agency?

Sample Letter: Disputing a Debt with a Collection Agency [Date] [Collection Agency Name] [Collection Agency Address] [Re: Your account number, if known] To Whom It May Concern: I wish to dispute the following charges that your company is attempting collection of: [List charges] I dispute the charges for the following reason(s):

Should you settle with a collection agency?

However, you can settle your debt with the collection agency. Nevertheless, you must know how to make a settlement with a collection agency to avoid any complications. Validate the debt collection agency claims. You should send the debt collection agency a letter requesting that it send you proof you owe the debt. Check the statute of limitations.

How do I settle my debt with a collection agency?

When entering negotiations, make sure to:

- Know your rights. You can’t be harassed, lied to, threatened, or even spoken to out of business hours.

- Consider your debt. What type of debt do you owe? This will help in understanding what you could ask for.

- Speak calmly and logically.

- Make your offer. Debt collectors may settle for around 50% of your debt. ...

How do I write a debt settlement agreement?

The following terms and conditions should be included in a settlement.Original creditor and collection agent's company name.Date the letter was written.Your name.Your account number.Outstanding balance owed on the account (optional)Amount agreed to as settlement.More items...

How do you get a settlement to offer to a collection agency?

Start by offering cents on every dollar you owe, say around 20 to 25 cents, then 50 cents on every dollar, then 75. The debt collector may still demand to collect the full amount that you owe, but in some cases they may also be willing to take a slightly lower amount that you propose.

Can I ask a collection agency to settle for less?

Believe it or not, though, it's possible to negotiate with a collection agent and end up paying less than you owe. Why is that? Because the collection agency bought the original debt from your creditor, most likely for a substantial discount. That means they don't have to recover the entire amount to make a profit.

What percentage should I offer to settle debt with collection agency?

When you're negotiating with a creditor, try to settle your debt for 50% or less, which is a realistic goal based on creditors' history with debt settlement. If you owe $3,000, shoot for a settlement of up to $1,500.

How do you write a settlement offer?

Writing the Settlement Offer Letter Include your personal contact information, full name, mailing address, and account number. Specify the amount that you can pay, as well as what you expect from the creditor in return. A good starting point for negotiation could be offering around 30% of the amount that you owe.

Is it better to settle or pay in full?

Generally speaking, having a debt listed as paid in full on your credit reports sends a more positive signal to lenders than having one or more debts listed as settled. Payment history accounts for 35% of your FICO credit score, so the fewer negative marks you have—such as late payments or settled debts—the better.

What is the 11 word phrase to stop debt collectors?

If you need to take a break, you can use this 11 word phrase to stop debt collectors: “Please cease and desist all calls and contact with me, immediately.” Here is what you should do if you are being contacted by a debt collector.

What should you not say to debt collectors?

Don't Give Information About Your Income, Debts, or Other Bills. Debt collectors can get some of this information from your credit report and may even use it to get you to make immediate payment. For example, they may say “I see that you're current on all your credit card payments.

Do settlements hurt your credit?

While settling an account won't damage your credit as much as not paying at all, a status of "settled" on your credit report is still considered negative. Settling a debt means you have negotiated with the lender and they have agreed to accept less than the full amount owed as final payment on the account.

Will debt collectors settle for 30%?

Lenders typically agree to a debt settlement of between 30% and 80%. Several factors may influence this amount, such as the debt holder's financial situation and available cash on hand.

What is a good settlement percentage?

The percentage of a debt typically accepted in a settlement is 30% to 80%. This percentage fluctuates due to several factors, including the debt holder's financial situation and cash on hand, the age of the debt, and the creditor in question.

Is it worth it to settle debt?

The short answer: Yes, debt settlement is worth it if all of your debt is with a single creditor, and you're able to offer a lump sum of money to settle your debt. If you're carrying a high credit card balance or a lot of debt, a settlement offer may be the right option for you.

What happens if a debt collector won't negotiate?

If the collection agency refuses to settle the debt with you, or if the agency or creditor agrees to settle, but you renig on your end of the agreement, the collection agency or creditor may decide to pursue more aggressive collection efforts against you, which may include a lawsuit.

What percentage will credit card companies settle for?

Lenders typically agree to a debt settlement of between 30% and 80%. Several factors may influence this amount, such as the debt holder's financial situation and available cash on hand.

When should a collection account be settled?

When you settle an account, the creditor (in this case the collection agency) will update the account on your credit report to show it has been settled in full for less than the total balance owed. This indicates that the account is closed and that there is no longer a balance due.

Can I pay original creditor instead of collection agency?

Working with the original creditor, rather than dealing with debt collectors, can be beneficial. Often, the original creditor will offer a more reasonable payment option, reduce the balance on your original loan or even stop interest from accruing on the loan balance altogether.

What is the most important part of a debt settlement letter?

One of the most important components of your debt settlement letter is a single number: the amount you decide to offer. You’ll base that number on your assessment of two considerations. Affordability. Never offer more than you can afford to pay.

What is the purpose of the settlement paragraph?

You’ll use this paragraph to present the details of your settlement offer. This will include the dollar amount you’re proposing to pay.

Why do you need to sign a letter?

Your Signature. Your letter will require your signature because you’ll be offering the creditor a contract, which is settlement of the debt. If you fail to sign your letter, the creditor may interpret that as an indication you’re not completely serious.

What to do if you can't pay your debt?

If you decide to try to settle your debts, you’ll start the process by writing a debt settlement letter. You’ll use the letter to propose settling the debt for a reduced amount.

What should be the opening paragraph of a letter?

First Paragraph. Your opening paragraph should quickly state the purpose of your letter, which is a proposal to settle the account for less than the full amount. In the next sentence, you’ll explain why you can’t pay the full amount.

What happens if you fail to sign a letter?

If you fail to sign your letter, the creditor may interpret that as an indication you’re not completely serious.

What should I say in the last sentence?

In the last sentence, you should provide a reason why you won’t be able to pay the full amount. It should be a circumstance beyond your control. I’ve listed several within the parentheses, but feel free to include whatever situation may be preventing you from making full payment. You don’t need to be long-winded here.

What Is a Debt Settlement Letter?

If you’re unable or unsure about negotiating a debt settlement over the telephone, negotiating by letter is a reasonable option. It’s not much different negotiating with your creditor by telephone, but it might take longer. There are several ways to prepare a settlement letter, including hiring an attorney to write it for you or going online to download a template to use as a starting point. There are also several sample letters you can look at to get an idea of what your completed letter should look like.

What is the first step in a debt settlement?

The first step in a debt settlement negotiation with a bank, credit card company, or collection agency is to confirm the debt belongs to you. Some debts pass through multiple collection agencies once they leave the original creditor. During that time, mix-ups can occur or debts can become so old they are past the statute of limitations and legally uncollectible .

How does debt settlement work?

Luckily, there are many debt relief options. Debt settlement is one of the most advertised and for good reason. It’s often used for credit card debts and allows borrowers with unmanageable debt to pay off one or more debts for less than the full amount. The creditor then forgives the remaining debt. This may sound too good to be true, but it’s not. How well it works for you will depend on your financial situation and whether you choose to hire a debt settlement company to help you or do the debt settlement process yourself. This article will explain how to handle debt settlement on your own and how to write the best debt settlement letter possible.

How long do you have to be behind on your debt to get a creditor to accept your debt?

To increase your chances of getting a creditor to accept your debt, you need to be at least 90 days behind on your payments with that creditor. And during the negotiation process, you’ll need to continue not making any payments. This will hurt your credit score and the extra fees and interest may increase your overall debt. But it’s easier to convince a creditor that you can’t fully pay off your debt when you haven’t made any payments for several months. Remember, a creditor is willing to settle a debt for less than what you owe because they fear your financial situation is so uncertain that they won’t recover any money from you in the near future.

How to reach out to your creditor?

Now it’s time to reach out to your creditor. You can do this by telephone or by letter. Either way, you’ll need to have some cash saved up beforehand. Most debts get settled after the borrower makes a one-time lump-sum payment of the outstanding debt. In other cases, you’ll need to pay two or three large payments over a short period of time instead. Creditors rarely agree to let borrowers use a payment plan with monthly payments to settle their debts.

How long does it take to settle a debt?

Another major advantage is that the DIY debt settlement process tends to be faster, perhaps six months or less. In contrast, using a debt settlement company can easily take several years. Not only does this extra time mean it takes longer to get debt relief, but that’s more time for your debt to accrue interest and penalties.

What is the second step in negotiating a debt?

The second step is deciding what terms you’ll agree to. During negotiations, the biggest item to discuss will be how much of the debt you need to pay. But don’t overlook another important term: how the debt will show up on your credit report.

How to write a settlement letter?

Make sure your letter has: 1 Header – this should include your full name and address, as well as the date that the letter has been written. 2 Body – this is where you will explain the details of your settlement offer (amount, dates of payments you will make, and how they will be made) and what you are expecting from your creditor. 3 Contact – your contact details, including a current phone, mobile, and e-mail address. 4 Closing – this is where you will sign the letter

What should a debt settlement letter include?

There are some key details that all debt settlement offer letters should have: The full name used for the credit account. Your full address. Your account numbers or a reference number from the creditor. This information is what your creditor will need to pull up all of the relevant details of your account with them.

What is a debt settlement offer letter?

This can be done using a debt settlement offer letter. This is a form that is used when the debtor and creditor want to agree to new terms in settling the outstanding debt. The letter is usually sent by the debtor to the creditor and may offer a lump sum that is not the full amount, but one that is agreeable to the creditor to accept ...

Why is it important to have a copy of an offer of acceptance from the creditor?

This is why it is important to have a written copy of an offer of acceptance from the creditor as proof, to stop them from trying to come back and claim the balance afterward.

What percentage of debt should be offered to a creditor?

Typically, an offer of between 30% of the debts outstanding balance should be made to a creditor for them to even consider it. The cre4ditor will normally come back with a counteroffer of 50%.

How long does a partial settlement stay on your credit report?

Negative marks on your credit report, such as a partial debt settlement, can stay on your report for 7 years.

What should the header of a letter include?

Header – this should include your full name and address, as well as the date that the letter has been written.

How long does it take to settle a debt with a collection agency?

They have five days to do so under the Fair Debt Collection Practices Act (FDCPA).

How to settle a debt on your own?

When you’re working to settle a debt on your own, you want to do everything in writing. This is especially true if you’re making formal debt settlement agreements. Creditors and collectors will try to get you to agree to things over the phone. Don’t fall for it! Ask them to send you their proposal in writing. Avoid saying anything that acknowledges that you’re obligated to repay the debt. You can use these debt settlement letter templates to negotiate everything in writing.

What is a counteroffer letter?

This template letter makes a counteroffer when an original creditor offers you an initial settlement amount. The goal is to offer a lower amount and negotiate for a removal of the negative information from your credit history.

Can you admit to a debt?

Never admit that you owe the debt or that you’re supposed to pay it. This can reset the statute of limitations on collecting the debt in some states!

What happens when a debt collector calls in a debt that is not being paid?

When creditors need to call in a debt that is not being paid by a consumer, they may give the problem to a debt collecting agency. Sometimes, debt collectors can be extremely persistent and actually harass a consumer.

What is the Fair Debt Collection Practices Act?

The Fair Debt Collection Practices Act (FDCPA) was created by congress to regulate debt collection agencies’ practices. If the debt collector is calling the consumer at work, they must stop if they receive a phone call from the consumer requesting them to stop. If the consumer is called at home, they need to write a cease ...

What to do if a consumer is called at home?

If the consumer is called at home, they need to write a cease and desist letter to get the debt collector to stop. While it is legitimate for a collection agency to collect the money owed, it is not legitimate for them to intimidate and harass the consumer.

What is a cease and desist letter?

This letter is a formal request that you cease and desist contacting me. It is also formal notification that I will file a complaint with the Federal Trade Commission in STATE Attorney General’s office, and I will pursue civil and criminal claims if you do not comply.

What is a C&D letter?

If this happens, the consumer can send a cease and desist (C&D) letter to the collection agency requesting or insisting that they stop harassing communication.

Can a C&D letter increase the chance of a collection agency sue?

For one thing, the letter could increase the chance the collection agency will sue and, since it stops all communication, the consumer may not know what other steps the collection agency intends to take. Not all creditors have to stop when a C&D letter is received.

Do all creditors have to stop a C&D?

Not all creditors have to stop when a C&D letter is received. The original creditor can still contact the consumer even if he or she has sent a letter asking them to stop. Original creditors are not bound by the FDCPA.