Are my workers'comp settlements taxable income?

Moreover, an experienced workers' compensation attorney may be able to structure your workers' comp settlement in a way that minimizes the offset and reduces your taxable income. Thus, while a portion of your workers' comp may considered taxable income, in practice the taxes paid on workers' comp are usually small or non-existent.

How does a workers'compensation settlement affect my Social Security benefits?

If you've received a lump sum from workers' comp, Social Security will prorate the settlement amount, after deducting expenses, to come up with your monthly rate. Reducing Taxable Income Through Your Workers' Compensation Settlement

Are my workers'compensation benefits taxable?

Workers' compensation benefits are not normally considered taxable income at the state or federal level. The lone exception arises when an individual also receives disability benefits through Social Security disability insurance (SSDI) or Supplemental Security Income (SSI).

Is a lump sum lump sum payment from workers comp taxable?

If the workmans comp was not taxable then the lump sum is also not taxable ... you just got one final amount so the insurance company can stop making monthly payments which could continue for years.

How can I avoid paying taxes on a settlement?

Spread payments over time to avoid higher taxes: Receiving a large taxable settlement can bump your income into higher tax brackets. By spreading your settlement payments over multiple years, you can reduce the income that is subject to the highest tax rates.

Should Workers compensation be reported on w2?

How do I deduct this income? Workers compensation for occupational sickness or injury are not taxable if paid under a workers' compensation act. The W-2 will need to entered as it is because the IRS will be looking for that income. But, you have a work around so you don't end up with increased taxable income.

What is the largest workers comp settlement?

a $10 millionTo date, the largest settlement payment in a workers' comp case came in March of 2017, with a $10 million settlement agreement.

What does lump sum settlement mean?

A lump sum settlement is a payout that comes in one single, large payment. This type of settlement occurs following negotiations, and the single payment covers the entire agreed on amount.

How does workers comp affect tax return?

Repayment of Workers' Compensation Benefits While you are completing your income tax return, deduct the same amount of your benefit (shown in box 10) on line 25000. This deduction allows your workers' compensation benefits to be deducted from your income. This ensures that you are not taxed on both amounts.

Do you pay tax on compensation payments?

Where compensation relates to a loss of profits from a trade; loss of income from a property business; or breach of contract relat- ing to a business, any such payment is likely to be treated as taxable income. If compensa- tion includes interest, that element could also be taxable as income.

How long do most workers comp settlements take?

around 12-18 monthsHow Long Does It Take to Reach a Settlement for Workers' Comp? The entire settlement process—from filing your claim to having the money in your hands—can take around 12-18 months depending on the details of your case and whether or not you have legal representation.

How long does it take to get paid after a settlement?

While rough estimates usually put the amount of time to receive settlement money around four to six weeks after a case it settled, the amount of time leading up to settlement will also vary. There are multiple factors to consider when asking how long it takes to get a settlement check.

How long does it take to get the Rtwsp check?

An eligibility determination will be made within 60 days. Privacy Notice on Collection of Personal Information: The Department of Industrial Relations will use the personal information collected below to determine your eligibility for, and pay the benefit authorized by Labor Code § 139.48.

How are lump sum payments taxed?

Mandatory Withholding Mandatory income tax withholding of 20% applies to most taxable distributions paid directly to you in a lump sum from employer retirement plans even if you plan to roll over the taxable amount within 60 days.

Why are lump sum payments taxed so high?

Bonuses are taxed heavily because of what's called "supplemental income." Although all of your earned dollars are equal at tax time, when bonuses are issued, they're considered supplemental income by the IRS and held to a higher withholding rate. It's probably that withholding you're noticing on a shrunken bonus check.

How are lump sum payments calculated?

0:007:52Present Value Formula Lump Sum (single amount) - YouTubeYouTubeStart of suggested clipEnd of suggested clipThe present value of a lump sum or the present value of a single amount this is when you're givenMoreThe present value of a lump sum or the present value of a single amount this is when you're given the future well. And you asked to calculate what the present value is.

Where do I put workers comp on TurboTax?

@aman2020 You should receive a form 1099-G reporting your workmen's compensation income and you will enter that in the Unemployment section of TurboTax, which is in the federal Wages and Income section.

Is workers Comp taxable in NY?

Under IRS regulations, workers' compensation-related benefits are exempt from federal income, Social Security and Medicare taxes. Workers' compensation-related benefits are also exempt from New York State and local income taxes, if applicable.

Is workers Comp taxable in Texas?

The benefits from workers' compensation are typically not taxable in Texas. You do not need to claim the income benefits from workers' compensation you receive on your taxes. Still, we encourage you to speak with a financial professional to make sure that you follow all state and local tax guidelines.

Is workers Comp taxable in California?

Taxes on Workers' Compensation in California Worker's compensation money is exempt from taxes in the overwhelming majority of cases. Worker's compensation is a public, federally funded benefit that serves to protect injured workers while they recover.

How Does a Workers’ Compensation Lump-Sum Settlement Work?

With a lump-sum settlement, the injured worker receives a substantial sum of money at once. For instance, someone with a serious injury may receive...

What are the Benefits of Accepting a Lump-Sum Settlement?

For many injured employees, agreeing to a lump-sum settlement makes sense.

What are the Downsides of Lump-Sum Settlements?

A lump-sum settlement should not be accepted without serious consideration.

What is the Alternative to a Lump-Sum Settlement?

An injured worker may feel that a lump-sum settlement is not in their best interest. The alternative is to accept a structured settlement.

How Do I Know if a Lump-Sum or Structured Settlement Makes Sense for Me?

Figuring out whether to accept a lump-sum or structured settlement can be challenging. No decision should be made without serious contemplation.

What is the reduction in workers compensation called?

This reduction is called the workers’ compensation offset.

How much of your earnings can you receive from Social Security Disability?

Let’s do the math. If you are receiving both Social Security Disability and workers’ compensation benefits, the combined amount cannot exceed 80% of your average current earnings. Your “average current earnings” are defined as the largest of:

Why is it important to have a workers compensation attorney?

It’s important that your workers’ compensation attorney structure your workers’ compensation settlement to minimize the offset. This will also minimize the tax burden.

Is supplemental income on workers comp taxed?

If an injured worker receives supplemental security income on top of their workers’ compensation, that supplemental income can be taxed. Specifically, there is a small portion of your workers’ comp benefits that can be taxed if you also receive either Social Security Disability Insurance (SSDI) ...

Is taxable workers compensation the same as SSA?

The amount of taxable workers’ compensation is the same amount the SSA reduces in your disability payments.

Do you owe taxes on Social Security?

Most people who receive workers’ compensation benefits and Social Security benefits don’t have enough taxable income to owe federal taxes. What this means is that even if a portion of your benefits is taxable, it is still unlikely you will owe any taxes. Furthermore, an accomplished workers’ compensation lawyer will be able to structure your ...

Is workers compensation taxable?

Workers’ compensation is not taxable. In fact, workers compensation settlements and payments are tax-exempt under the the Workers’ Compensation Act. According to this IRS publication, “Amounts you receive as workers’ compensation for an occupational sickness or injury are fully exempt from tax if they are paid under a workers’ compensation act ...

What expenses can you deduct from your workers comp?

The expenses include lawyer fees, medical expenses, and even dependent costs.

How much of your pre-injury income can you receive from SSDI?

By law, you can only receive up to 80% of your pre-injury earnings between SSDI and workers comp benefits. If your SSDI and workmen’s comp add up to over 80% of your pre-injury income, the Social Security Administration will offset your SSDI (reduce it) by the exact amount you’re over the threshold.

Is workers comp taxable?

Generally speaking, no workers comp settlements are not taxable at the federal or state level. If you’re injured at work and receive payments to cover your medical expenses, loss of wages, and pain/suffering, they aren’t taxable in most cases.

Is 401(k) withdrawal taxable?

Similarly, if you receive retirement income including withdrawing from your 401K or IRA,that income is taxable if you cross the threshold of the minimum required income to file taxes, not including your workers comp income.

Do you have to work on light duty to get workers comp?

Many people on workmen’s comp end up going back to work on ‘light duty.’ Since you’ll earn income working but still get some workers comp, you’ll owe taxes on the earned income that isn’t the workmen’s comp income if it exceeds the threshold for taxable income for the year.

Do you have to report workers comp on taxes?

You do not have to report workers comp income on your tax returns. If you received workers comp for the entire year, you would have no income to report on your taxes, IF it’s the only income you receive.

Can you ask for lump sum settlement?

If you receive a lump sum settlement, you can ask for it to be prorated over your lifetime. You still receive the settlement in one payment, but for tax purposes, it’s amortized over your expected lifetime.

How Does a Workers’ Compensation Lump-Sum Settlement Work?

With a lump-sum settlement, the injured worker receives a substantial sum of money at once. For instance, someone with a serious injury may receive a settlement offer of $500,000. If the worker accepts the money, the money will be issued immediately. This allows the worker to have instant access to the full settlement amount.

What are the Benefits of Accepting a Lump-Sum Settlement?

For many injured employees, agreeing to a lump-sum settlement makes sense. They appreciate the advantages that can come from a lump-sum settlement, including:

What is the Alternative to a Lump-Sum Settlement?

An injured worker may feel that a lump-sum settlement is not in their best interest. The alternative is to accept a structured settlement. With a structured settlement, money is disbursed over time. In other words, the settlement amount is given to the employee on a regular schedule. The schedule could be every week, month, or year.

How Do I Know if a Lump-Sum or Structured Settlement Makes Sense for Me?

An injured employee will want to make sure that their medical condition has stabilized before accepting either type of settlement. That way, they have a general sense of how their disability will affect the rest of their life.

What are the benefits of structured settlement?

Some of the other upsides to structured settlements include: 1 A structured settlement offers consistent payments. This reduces the ability to spend all the cash at one time. 2 A structured settlement allows for the possibility of a lifetime of compensation. Many workers appreciate knowing that if they need more money, they can appeal for it. 3 A structured settlement is tax-exempt. The same tax rules governing lump-sum settlements pertain to structured settlements. Consequently, workers do not harm themselves by choosing a structured settlement over a lump-sum settlement.

Why is structured settlement important?

This reduces the ability to spend all the cash at one time.

What are the two types of settlements?

However, many workers are confused by the two main settlement types: lump-sum settlements and structured settlements. Before accepting any settlement offer, especially a lump-sum settlement, an employee who has a work-related injury should consider consulting with a lawyer. The lawyer can help them understand the advantages and disadvantages ...

Is a debt recovery exemption waived?

such compensation and benefits shall be exempt from all claims of creditors, and from levy, execution, and attachments or another remedy for recovery or collection of a debt, which exemption may not be waived.

Is there a reverse offsetting process for workers comp?

Some states also implement a “reverse offsetting” process. Instead of your SSI/SSDI, your workers’ comp will be reduced.

Do You Receive a 1099 for Workers Compensation?

A 1099 form is a record of any income you received other than wages and salaries. Since workers’ compensation isn’t a taxable income, you should not receive a 1099 form for it. If you did, inform your workers’ compensation office about the mistake and find out what you can do. You can also talk to your employer so they can file a corrected 1099.

Can I get workers comp and SSDI at the same time?

And if you’re wondering, yes, it’s very much possible to receive workers comp and SSDI or SSI at the same time. The combined amount, however, should not exceed 80% of your weekly wage from before the accident. Otherwise, the SSA will reduce your benefits in a process called workers compensation offsetting.

Is workers comp taxable?

In general, the law does not consider workers’ compensation as taxable income. Thus, workers’ comp sett lements are not taxable both at the state and federal level. It doesn’t matter whether you’re receiving monthly payments or a lump sum settlement. As long as it’s part of your workers’ comp benefits, you won’t get taxed.

Is workmen's compensation taxable?

The Internal Revenue Code expressly states that: “amounts received under workmen’s compensation acts as compensation for personal injuries or sickness shall not form part of the taxable gross income.” But if you’re receiving SSI or SSDI on top of your workers’ comp, it’s a different story.

Does SSI affect taxes?

Aside from SSI/SSDI, having other sources of income while receiving workers comp will also affect your taxes. For example, if you take money from a 401k or retirement plan during your benefit period, you’ll most likely pay taxes for that. If you return to work or did any income-generating activity while on workers comp, you’ll also be taxed accordingly.

How much of your earnings can you receive from workers compensation?

If you're receiving both workers' compensation and Social Security disability benefits, the combined amount of your benefits cannot exceed 80% of your average current earnings. Your "average current earnings" are defined as the largest of:

How much is a prorated Social Security settlement?

If the settlement agreement provides that the lump sum is spread out over the beneficiary's lifetime, Social Security will usually find that the prorated monthly amount is $30 ($13,500 divided by 450 months).

How much is John's SSDI?

He is eligible for a monthly SSDI benefit of $1,500 and monthly workers' comp of $800, for a total of $2,300 per month. Because that amount exceeds $2,000 (80% of his average current earnings), in most states John's SSDI will be reduced by $300.

What is reverse offset for workers comp?

A minority of states have a "reverse offset," in which your workers' comp payments are reduced. Social Security will subtract legal fees, past and future medical costs, payments to dependents, and other expenses from the workers' comp amount prior to calculating the offset.

Is a $250 unemployment check taxable?

Thus, if SSA lowers your monthly SSDI check by $250 due to the workers' compensation offset, then $250 of your workers' comp is taxable. Most people who receive Social Security and workers' comp benefits don't have enough taxable income to owe federal taxes, so even if a portion of your benefits are taxable, it's not likely you'll owe taxes.

Is workers compensation taxable?

Workers' compensation benefits are not normally considered taxable income at the state or federal level. The lone exception arises when an individual also receives disability benefits through Social Security disability insurance (SSDI) or Supplemental Security Income (SSI). In some cases, the Social Security Administration (SSA) ...

Can you spread workers comp benefits?

Note that in a few areas, the settlement can only be spread through your retirement date, not for the rest of your actuarial life. Either way, a well-drafted settlement agreement can often eliminate your tax liability for workers' comp benefits.

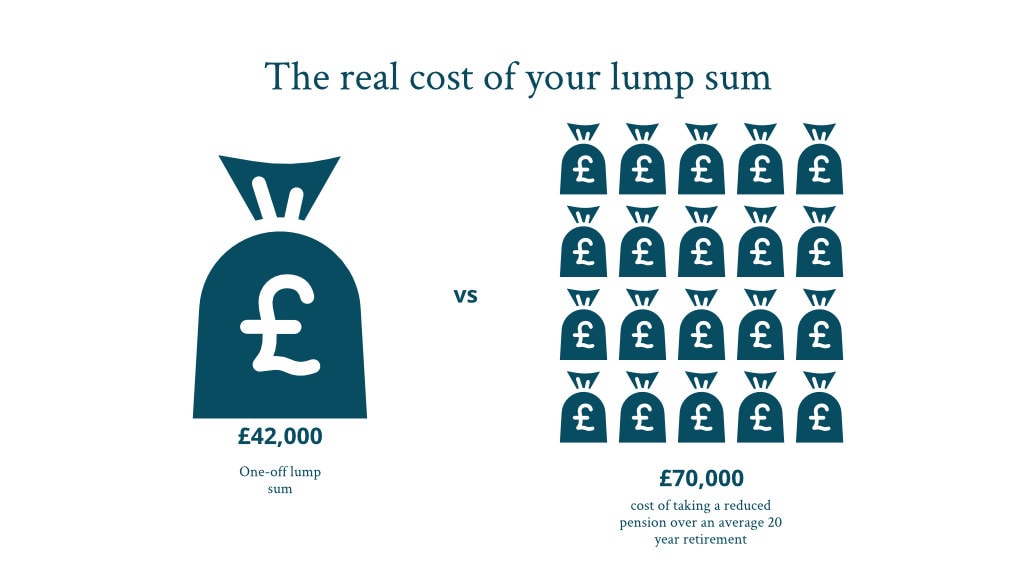

What is lump sum compensation?

It’s important to know that there are 2 ways workers’ compensation benefits could be provided if you will require lifetime care for your work-related injury: A lump sum settlement is a single large payment that’s intended to cover your medical expenses for the remainder of your life. It’s paid once, and you manage the money your own way.

What are the advantages of lump sum settlement?

There are some distinct advantages to a lump sum settlement. First, the money becomes yours. If you’re the type of person who manages money well and is careful about saving for the long-term, it might be helpful to have a finite amount that you can spend as you need it.

What happens if you run out of money on your insurance?

Even if all of the expenses are expected, if the money runs out, it runs out. There’s no second chance. There are times when the insurance company will require that you resign from your job in order to take a lump sum settlement.

How are lost wages calculated?

Usually, lost wages are calculated into the overall amount of a lump sum settlement. With lifetime medical benefits, you’re covered for your medical expenses only, not any additional amount of time you’d need to take off from work in the future as a result of the injury. For example, if your injury requires you to have surgery 5 years from now, you would be covered for the surgery but not for the amount of time you need to be out of work to recover.

How long does workers compensation last?

In most states, workers’ compensation will provide lost wages and permanent partial disability benefits for a maximum of 500 weeks (about 9.5 years). If an authorized treating physician believes that ongoing medical treatment related to a work-related injury is reasonable and necessary, you could become eligible for lifetime medical benefits.

How many workers were covered by the federal workers compensation system in 2015?

About 135.6 million workers were covered under state and federal workers’ compensation programs in the U.S. in 2015. The system paid nearly $62 billion in benefits during that year. While most work-related injuries are relatively minor and workers can recover and return to work, that’s not always the case.

Do you have to prove medical expenses related to work injury?

Second, you can obtain whatever medical treatment you think you need. There’s no requirement to prove that medical expenses are related to the work injury because the money is yours to spend. You would manage your own medical treatment.

Is compensation for sickness taxable?

Many other amounts you receive as compensation for sickness or injury aren't taxable. These include the following amounts.

Is workers compensation taxable?

No, workers' compensation benefits are not taxable income.