A non-compete agreement (sometimes called an agreement not to compete) is an agreement between two parties in which one party compensates the other party for agreeing not to compete. This agreement can be a cost to a business, and this cost can be deducted in some circumstances.

Full Answer

Is a settlement tax deductible?

In terms of settlement, an accrual-based taxpayer would deduct such cost once the settlement agreement is executed and the company’s payment amount is established.

Are Non-Compete Agreements tax deductible?

Non-Compete Agreements and Tax Deductions. A non-compete agreement (sometimes called an agreement not to compete) is an agreement between two parties in which one party compensates the other party for agreeing not to compete.

How is a non-compete fee received from a company taxed?

If the non-compete covenant is a part of a transaction involving transfer of capital assets amounting to transfer of the business, the non-compete fee received would be covered under the proviso (i) to section 28 (va) (a) and would be taxed as a capital receipt.

Are lawsuits tax deductible for businesses?

Even when the company settles down the lawsuit without any payment between the two parties there will still be the tax deduction and that will be based on the court fees and the lawyer’s fees. All these things will still be a part of the company’s expenditure and the business owner will not be obliged to include that during tax payment.

Is a non-compete agreement tax deductible?

The buyer can capitalize the amount of the purchase price allocated to the non-competition covenant and is entitled to a tax deduction for the life of the covenant. Because of these differing tax treatments, the seller and buyer will have opposite interests when negotiating the sale.

How is a noncompete agreement taxed?

Tax Treatment of Noncompete Covenants: Owner Where the owner enters into a compensatory noncompete covenant, the consideration received is taxed to the owner at ordinary income rates, whether the transaction is structured as a stock or asset sale.

How do you depreciate a non-compete agreement?

Covenant Not to Compete Must Be Amortized Over 15 years The Tax Court, in a CASE OF FIRST IMPRESSION, has held that a company must amortize over 15 years a covenant not to compete because it was entered into with an indirect acquisition of an interest in a trade or business -- that is, the redemption of the company's ...

Is a noncompete an asset?

A noncompete agreement is an intangible asset because there is value in preventing another party from operating a business within the same industry. While it is difficult to place a specific value on a noncompete agreement, value can be assigned during purchase accounting.

How long do you amortize covenant not to compete for tax purposes?

Regardless of whether a covenant not to compete is entered into in connection with the acquisition of a corporation or partnership through direct purchase of the assets or indirectly through the purchase of stock or partnership interests, the covenant is considered an Internal Revenue Section 197 intangible and must be ...

Is non-compete agreement capital gain?

Payments received for a covenant not to compete are treated as ordinary income rather than capital gain. Therefore, sellers will generally prefer allocating the purchase price to capital assets and Sec.

Does a non-compete transfer in an acquisition?

Indeed, even California, which prohibits employment non-competes outright, allows such provisions to apply to merger/acquisition transactions.

Is a covenant not to compete taxed as ordinary income?

Payments received for a covenant not to compete are treated as ordinary income rather than capital gain. Therefore, sellers will generally prefer allocating the purchase price to capital assets and Sec.

Are non-compete agreements enforceable in New Jersey?

For a non-compete agreement to be enforceable, New Jersey courts require that the non-compete agreement (1) protects the legitimate interests of the employer; (2) does not impose an undue hardship on the employee; and (3) is not injurious to the public.

What voids a noncompete agreement?

You Can Void a Non-Compete by Proving Its Terms Go Too Far or Last Too Long. Whether a non-compete is unenforceable because it covers too large of a geographical area or it lasts too long can depend on many factors. Enforceability can depend on your industry, skills, location, etc.

Are non competes enforceable in Tennessee?

Non-compete agreements are enforceable against former employees, according to Tennessee law, as long as the agreements are reasonable and necessary to protect the employer's legitimate interests, the Court of Appeals of Tennessee has ruled.

What is the Medicare tax on self employment?

But if the seller already receives wages or other self - employment income at or above the Federal Insurance Contributions Act limit, the only cost will be the 2.9% Medicare Health Insurance (HI) portion of the self - employment tax and possibly the additional 0.9% Medicare tax on earned income.

How long can a non-compete agreement be enforced?

The enforceability of the noncompete agreement depends on a number of factors, including: 1 The length of the agreement, with the courts generally considering a period of two to three years or less to be reasonable; 2 The scope of the agreement, which should not be overly broad; and 3 The geographic area covered by the agreement, which should be reasonable based on the company's and the individual's expected area of operation.

What is the maximum long term capital gain rate for self-created goodwill?

Assuming the seller has no basis in the self - created goodwill, the proceeds allocated to his or her goodwill will be taxed once at the maximum long - term capital gain rate of 15% or 20% (depending on the seller's taxable income).

What are some examples of incentives to minimize allocations to covenants?

Examples include receivables, inventory, machinery, and equipment.

Do sellers allocate the purchase price to capital assets?

Therefore, sellers will generally prefer allocating the purchase price to capital assets and Sec. 1231 assets (like goodwill and real estate) rather than to covenants not to compete. If the buyer is indifferent about how the price is allocated, the IRS will look at whether "too little" is allocated to the covenant.

Is a consulting agreement deductible?

Amounts attributable to a consulting agreement are deductible over the period the seller is to provide services. To the extent that a portion of the consideration can be legitimately attributed to the consulting agreement, the buyer will be entitled to a deduction at the time of the payment.

Can a buyer and seller agree to allocate more of the purchase price to goodwill?

For example, the buyer and seller may agree to allocate none of the purchase price to the covenant and allocate more of the purchase price to goodwill. The buyer is indifferent because both covenants and goodwill are amortized over 15 years under Sec. 197. However, the seller prefers goodwill because it is a capital asset.

What is the meaning of "non-compete fee" in Sasken Communication Technologies Ltd v ITO?

In Sasken Communication Technologies Ltd v ITO (21), the ITAT held that where non-compete fees were paid by the assessee company to its employees at the commencement of their employment, for not competing with the assessee company in case of the said employees terminating their services with it, the same would be remuneration or compensation paid in relation to employment and therefore, would fall under the term salary or profit in lieu of salary.

What does "not to compete with a particular person" mean?

The agreement not to compete with a particular person in his business does not prevent a person from carrying on the same business in a manner which would not compete with the business of that particular person.

When an assessee signed a negative covenant not to carry on manufacture or trade in product for certain period of time?

when an assessee signed a negative covenant not to carry on manufacture or trade in product for certain period of time, it amounted only to self-imposed restriction and not a transfer. There is neither a sale or exchange or relinquishment of an asset, nor any right therein, which is extinguishable, the right to manufacture or trade remaining intact after the period for which the negative covenant was signed

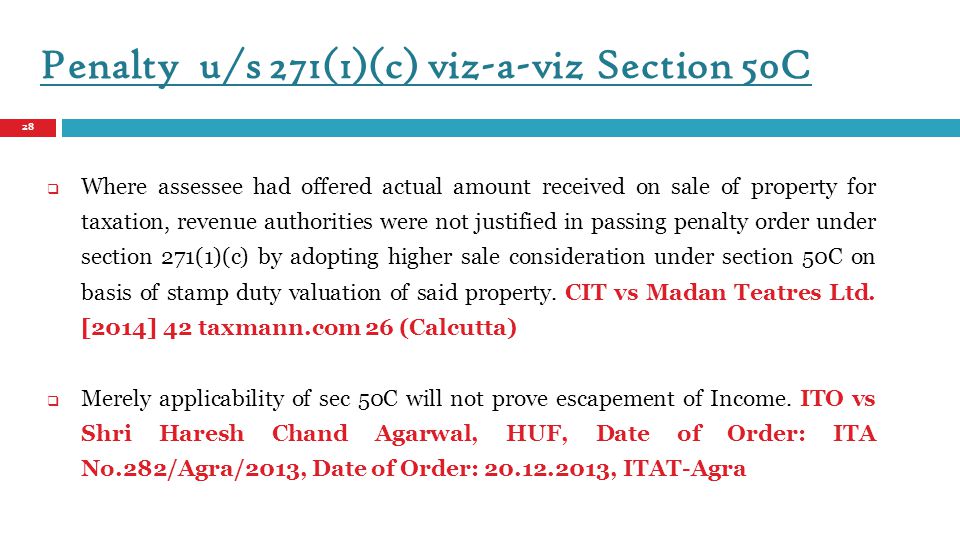

Is non-compete fee taxable?

Payment received as non-compete fee was treated as a capital receipt till the assessment year 2003-04. Through the Finance Act, 2002, the said receipt were made taxable under section 28 (va) of the Income Tax Act, 1961 with an exception is found under proviso clause (i) to section 28 (va) (a), which provides that any sum, whether received or receivable, in cash or kind, on account of transfer of the right to manufacture, produce or process any article or thing or right to carry on any business, which is chargeable under the head ‘Capital gains’ would not be taxed under section 28 (va). Further the Finance Act, 2002 also amended section 55 (2) (a) to provide for ‘cost of acquisition’ in case of transfer of ‘right to manufacture, produce or process any article or thing’ or ‘right to carry on any business’. These amendments have brought about a dichotomy in the taxability of non- compete fees, with regards to taxability as ‘Business income’ under section 28 (va), or as ‘Capital gains’ covered by the proviso (i) to Section 28 (va) (a). From the decisions of the Income Tax Appellate Tribunal (‘ITAT’) and the High Courts it can be seen that the taxability of non-compete fee would depend on the factors such as the position of the recipient of the non-compete fee with regards to the business before and after the non-compete covenant coming to operation, his relation with the payer of non-compete fee, the type of asset transfer taking place, and the terms of the non-compete covenant. Some of these factors influencing the taxability of non-compete fee have been discussed below:

Is a non-compete a transfer of rights?

The non-compete covenant on its own cannot amount to a transfer of any right. A mere refrainment from carrying on an activity would be taxed under section 28 (va) as can be seen from the decision of the Bombay High Court in the case of John D’souza v. CIT and Anr (11). In this case the assessee had entered into an agreement with a company which had purchased a certain plot on which the assessee was carrying on fish farming. By the agreement, the assessee had agreed to stop fish farming in in the said ponds, for which he had received a certain sum from the said company. The High Court was of the view that the assessee had received the said sum for ‘not carrying on any activity in relation to fish farming’, the same being taxable under section 28 (va) (a). Assessee contended that the said sum be taxed under section 45 as capital gains. To this the High court held that for the application of section 45 there should be a transfer of capital asset which was absent in the case.

Is a receipt capital gains?

The ITAT ruled in f avour of the assessee and held the entire receipt is to be treated as capital gains. The ITAT relied on the following facts as mentioned in the order of Commissioner of Income Tax (Appeals) (‘CIT (A)’), for holding that the assessee had wholly given up its “right to carry on the Healthcare Journals and Communications business” for a specified period:

What is a limitation to deduction?

When we talk about the limitation to the tax deduction we mean the things that you might think or may imagine will be considered part of business’ expenses but are not considered the expenses by the legislation. So, in a legitimate business, you have to be careful of such thing so that you are not burdened with more load regarding taxes than you imagine.

What is a lawsuit settlement?

A lawsuit settlement is when two different parties settle their case on an agreeable situation or payment. Mostly in such cases, one of the parties has to pay the other party a settlement amount to close the case legally. If you are new to the business side of the industry you will need to learn how to do your taxes and what things can lead to a deduction of taxes, even in such cases you have to know your limitations as to what extent tax can be deducted, and are lawsuit settlements tax deductible? You cannot expect your business tax to be deducted from a personal lawsuit because that is a personal matter, but if you are paying a business settlement there can be a chance of tax being deducted for that.

Can you deduct lawsuit settlements?

If you know the limitations to these things and are well aware of what things can increase the deduction you will have to pay a small amount of tax only in such a crisis. Any expenses of the business can help you in tax deduction and lawsuit settlements are one of the business’s expenditures just like the office rent is. So, this is the most understandable example of tax deduction due to lawsuit settlement.

Is personal business expense a business expense?

As we know personal business is one of these things that are not to be mixed in your business and such expenses will never be considered part of your business expenses. Similarly, if the company is facing a lawsuit because of any employee or even the owner of a business, then money spent on them will never be considered a business expense but it will always be a personal expense. This is why any such settlements will not cause the deduction in the taxes.

Can you deduct business taxes from a personal lawsuit?

You cannot expect your business tax to be deducted from a personal lawsuit because that is a personal matter, but if you are paying a business settlement there can be a chance of tax being deducted for that.

Do business taxes increase or decrease?

Usually, when it comes to the business taxes, they are to be paid from the profit you have earned. Similarly, the tax will increase or decrease according to some loss or profit in your business. For the tax payments, your entire inventory is scanned for the very same reasons. If anything bad happens to your business that results in less profit, then it will eventually reduce the tax.

Is a settlement considered a company's expense?

If the lawsuit is against the whole business based on any kind of services, then the settlement will be considered as the company’s expenses. Even if you claim this as the company’s lawsuit it will be up to the decision of legislation as to what this lawsuit will be labeled as.

What is the tax consequences of a settlement?

Takeaway. The receipt or payment of amounts as a result of a settlement or judgment has tax consequences. The taxability, deductibility, and character of the payments generally depend on the origin of the claim and the identity of the responsible or harmed party, as reflected in the litigation documents. Certain deduction disallowances may apply.

What is the exception to restitution?

The restitution exception applies only if (1) a court order or settlement identifies the payment as restitution/remediation or to come into compliance with law (identification requirement) and (2) the taxpayer establishes that the payment is restitution/remediation or to come into compliance with law ( establishment requirement).

How is proper tax treatment determined?

In general, the proper tax treatment of a recovery or payment from a settlement or judgment is determined by the origin of the claim. In applying the origin-of-the-claimtest, some courts have asked the question "In lieu of what were the damages awarded?" to determine the proper characterization (see, e.g., Raytheon Prod. Corp., 144 F.2d 110 (1st Cir. 1944)).

Is a claim for damages deductible?

For example, a claim for damages arising from a personal transaction may be a nondeduct ible personal expense. A payment arising from a business activity may be deductible under Sec. 162, while payments for interest, taxes, or certain losses may be deductible under specific provisions of the Code (e.g., Sec. 163, 164, or 165). Certain payments are nondeductible (as explained further below), and others must be capitalized, such as when the payer obtains an intangible asset or license as a result of asettlement.

Is a settlement taxable income?

For a recipient of a settlement amount, the origin-of-the-claimtest determines whether the payment is taxable or nontaxable and, if taxable, whether ordinary or capital gain treatment is appropriate. In general, damages received as a result of a settlement or judgment are taxable to the recipient. However, certain damages may be excludable from income if they represent, for example, gifts or inheritances, payment for personal physical injuries, certain disaster relief payments, amounts for which the taxpayer previously received no tax benefit, cost reimbursements, recovery of capital, or purchase price adjustments. Damages generally are taxable as ordinary income if the payment relates to a claim for lost profits, but they may be characterized as capital gain (to the extent the damages exceed basis) if the underlying claim is for damage to a capitalasset.

Is a settlement deductible?

For both the payer and the recipient, the terms of a settlement or judgment may affect whether a payment is deductible or nondeductible, taxable or nontax able, and its character (i.e., capital or ordinary). In general, the taxpayer has the burden of proof for the tax treatment and characterization of a litigation payment, ...

Does the disallowance apply to restitution?

The disallowance does not apply to payments for restitution (including remediation of property) or to come into compliance with law; taxes due; or amounts paid under court orders when no government or governmental entity is a party to the suit.

Why do you capitalize lawsuits?

For example, if a lawsuit arises because a plaintiff challenges the validity of a merger transaction, such expenses incurred in defending the lawsuit must be capitalized because the claim is rooted in the acquisition of a capital asset. If, however, the plaintiffs allege that securities law violations by the board of directors harmed the value ...

Is defending a lawsuit tax deductible?

Background. Like the cost of office equipment and rent, the costs associated with defending a lawsuit are generally considered costs incurred in the ordinary course of business and are, therefore, tax deductible. Not all lawsuits and legal costs are treated equally. Court cases and legislation have narrowed the scope of what is, and what is not, ...

Can a company deduct legal expenses?

No company welcomes a lawsuit with open arms, but knowing that related expenses are generally deductible can be comforting as legal bills start to multiply. Companies must be aware of the limitations of writing off legal expenses, damages, and settlements so that they can take full advantage of the deduction on their next tax return. To fully assess your situation, it is always best to consult a professional regarding available tax deductions for costs incurred in litigation.

Is legal fees deductible?

Any legal fees or court costs incurred will be deductible as well as the cost of resolving the suit , whether the company pays damages to the plaintiff or agrees to settle the dispute. Moreover, if a company is defending itself against the government, any damages characterized as remedial or compensatory are deductible.

Is a lawsuit deductible for a company?

Any lawsuit a company faces is disruptive to business. The costs associated with hiring attorneys, defending a case, and paying for damages or a settlement can be exorbitant, and damage a company’s profitability. The good news is these payments are generally tax deductible business expenses. In order to maximize this deduction, however, companies ...

Is a fine deductible in a settlement agreement?

The characterization of such damages in the settlement agreement is critical. Fines and punitive and penal damages are not deductible. Consult a tax attorney when it comes to negotiating any settlement agreement to ensure that the desired tax treatment of costs is baked into the agreement.

Is a lawsuit deductible if it does not stem from a business activity?

This decision serves as a reminder to businesses that being a named defendant alone is not enough; if a lawsuit does not stem from a business activity, the legal fees and settlement expenses will not be deductible. Know Your Limits.

What is the tax rule for settlements?

Tax Implications of Settlements and Judgments. The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code. IRC Section 104 provides an exclusion ...

What is the exception to gross income?

For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury.

What is the purpose of IRC 104?

IRC Section 104 provides an exclusion from taxable income with respect to lawsuits, settlements and awards. However, the facts and circumstances surrounding each settlement payment must be considered to determine the purpose for which the money was received because not all amounts received from a settlement are exempt from taxes.

What is employment related lawsuit?

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example lost wages, business income and benefits, are not excludable form gross income unless a personal physical injury caused such loss.

What is a 1.104-1 C?

Section 1.104-1 (c) defines damages received on account of personal physical injuries or physical sickness to mean an amount received (other than workers' compensation) through prosecution of a legal suit or action, or through a settlement agreement entered into in lieu of prosecution.

Is emotional distress excludable from gross income?

96-65 - Under current Section 104 (a) (2) of the Code, back pay and damages for emotional distress received to satisfy a claim for disparate treatment employment discrimination under Title VII of the 1964 Civil Rights Act are not excludable from gross income . Under former Section 104 (a) (2), back pay received to satisfy such a claim was not excludable from gross income, but damages received for emotional distress are excludable. Rev. Rul. 72-342, 84-92, and 93-88 obsoleted. Notice 95-45 superseded. Rev. Proc. 96-3 modified.

Is a settlement agreement taxable?

In some cases, a tax provision in the settlement agreement characterizing the payment can result in their exclusion from taxable income. The IRS is reluctant to override the intent of the parties. If the settlement agreement is silent as to whether the damages are taxable, the IRS will look to the intent of the payor to characterize the payments and determine the Form 1099 reporting requirements.

Why should enforcement action settlement agreements identify settlement payments as restitution?

Enforcement action settlement agreements should identify settlement payments as restitution to maximise the chances of tax deductibility

Who is the final arbiter of enforcement action settlement payments?

Ultimately, the IRS remains the final arbiter of enforcement action settlement payments’ tax deductibility. Lauren Briggerman and Kirby Behre are members, and George Hani is a member and chair of the Tax Department, at Miller & Chevalier.

What is the new tax law?

New tax law modifies rules for deductibility of settlement payments in enforcement actions. In many civil and criminal resolutions involving government enforcement matters, the settling defendant entity or individual is required to ‘disgorge’ any profits or other ill-gotten gains that resulted from the alleged misconduct.

What is Section 162 F?

Section 162 (f) specifically prohibited the deduction of any “fine or similar penalty paid to a government for the violation of any law” (26 U.S.C. 162 (f) (2012)). The policy behind this rule was that a taxpayer should not be permitted to enjoy a tax benefit from the payment of an amount intended to be punitive.

Is disgorgement a punitive or compensatory payment?

As a result, defendants settling enforcement actions with the government should be prepared to argue to the IRS why their settlement payments are compensatory rather than punitive.

Can IRS disgorgement be tax deductible?

Even if enforcers agree to characterise a settlement payment as restitution, however, the IRS remains free to challenge the tax deductibility of settlement payments to government agencies. To the extent that such payments disgorge ill-gotten gains, settling defendants should be aware of relevant case law and internal IRS guidance that may foreshadow the IRS’s unwillingness to view certain disgorgement payments as tax deductible. In October 2016, the United States Supreme court ruled in Kokesh v. SEC that disgorgement in SEC enforcement cases constituted a penalty, thereby rejecting the SEC’s long-held position that disgorgement is an equitable remedy.

Can IRS disfavour settlements?

Recent case law and IRS internal guidance suggest that the IRS may disfavour gran ting tax deductibility to settlement payments that aim to disgorge ill-gotten gains. Settling defendants should arm themselves with facts to convince the IRS that their disgorgement payments are compensatory, and therefore do meet the definition of restitution, ...

What happens if you fail to include identification and establishment language in your settlement agreement?

If they fail to do so, they may forfeit their ability to claim a deduction for those payments.

When do you file 1098-F?

The official must also file a Form 1098-F and Form 1096, and must do so on or before February 28 (March 31 if filed electronically) of the year following the calendar year in which the order or agreement became binding. Finally, the official must provide a written statement, including the information reported to the IRS, ...

What is restitution in the new rule?

The new rule outlines enhanced requirements and greater definitional guidance on what qualifi es as “restitution,” “remediation,” and “coming into compliance with a law ,” particularly when it comes to environmental matters.

Is restitution deductible?

Restitution and remediation do not include amounts paid to a governmental account for general enforcement efforts or other discretionary purposes. Rather, to be deductible, the monies paid to a government or government entity must be paid into a separate fund or account and be used exclusively for the restitution or remediation of the environment, ...

Is a settlement agreement deductible?

This means that, generally, monies paid pursuant to a court order or settlement agreement with a government entity are not deductible. However, the 2017 Tax Cuts and Jobs Act (TCJA) amended § 162 (f) to allow deductions for payments for restitution, remediation, or those paid to come into compliance with a law.

Can you deduct a court order?

This means that, generally, monies paid pursuant to a court order or settlement agreement with a government entity are not deductible. However, the 2017 Tax Cuts and Jobs Act (TCJA) amended § 162 (f) to allow deductions for payments for restitution, remediation, or those paid to come into compliance with a law. Yet, in the years following the amendment to § 162 (f), taxpayers were left with several questions about what was and was not deductible.