Debt settlement is slightly less damaging to your credit than bankruptcy: Though debt settlement can cause your credit score to take a massive hit during the months that you stop paying your bills, once your debt is settled, it will remain on your credit report for seven years—shorter than the 10 years for Chapter 7 bankruptcy

Chapter 7, Title 11, United States Code

Chapter 7 of the Title 11 of the United States Code governs the process of liquidation under the bankruptcy laws of the United States. Chapter 7 is the most common form of bankruptcy in the United States.

Full Answer

What is the difference between debt settlement and bankruptcy?

What is the Difference Between Debt Settlement and Bankruptcy?

- Debt Settlement. Debt settlement is an alternative to bankruptcy that may be right for some people. ...

- Bankruptcy. Filing for bankruptcy can be a much longer and complicated process than debt settlement. ...

- Discuss Your Case With Our Schertz, TX Bankruptcy Attorney. ...

Is it better to pay off debt or declare bankruptcy?

Unemployment is not required, either, since a temporary setback can also justify filing a bankruptcy case. The short answer to the question is that it is almost always better to pay off debt, if possible, instead of declaring bankruptcy. Sometimes, however, there’s really no other option, such as when the bank wants to foreclose the mortgage.

Is debt settlement bad on your credit report?

Settled accounts may harm your credit history but their effects are minimal compared to having an unpaid debt listed on your credit report. Creditors will look at credit reports with settled debts more favorably than those with unpaid debts.

Should you do debt consolidation, bankruptcy or settlement?

If you’ve exhausted all other options trying to pay off your debts, your last resort may be to either settle your debt or file for bankruptcy. These options should only be considered if you’ve tried everything else and cannot pay down or eliminate your debt.

Which is better a debt relief program or bankruptcy?

Bankruptcy frees you from debt collection, but the headaches can linger for years. Debt settlement without bankruptcy can take more time but — if negotiated properly — can do less damage to your credit. Debt settlement stays on your credit report for seven years, but has less negative impact on your credit score.

What is the difference between bankruptcy and debt consolidation?

While debt consolidation means combining your debts into a new loan with new repayment terms, bankruptcy involves discharging or reducing it so you no longer have to pay back some of it (or even all of it).

What is the success rate of debt settlement?

Completion rates range from 35% to 60%, with the average around 45% to 50%. While most companies defined a completion as having all debts settled, there were two that considered a client completed if they had settled at least 80% of the debt and one if they had settled at least 50% of the debt.

Is bankruptcy worse than debt?

Debt settlement can be more lengthy than bankruptcy, and will still damage your credit score. If you need immediate relief or do not have the ability to pay monthly fees, bankruptcy may be the best (or only) solution.

How long does debt consolidation stay on your record?

Debt settlement can cause your credit score to fall by more than 100 points, and it stays on your credit report for seven years. If your creditors close accounts as part of the settlement process, this can cause your credit utilization to increase, which also negatively affects your credit score.

How much debt should you have to file bankruptcy?

There is no minimum debt to file bankruptcy, so the amount does not matter. Examples of unsecured debts include credit card debt, cash advance (payday) loans, and medical bills. Secured debts: If you are behind on a house or car payment, this may be a very good time to file for bankruptcy.

How long does it take to rebuild credit after debt settlement?

between 6 and 24 monthsYour credit score will usually take between 6 and 24 months to improve. It depends on how poor your credit score is after debt settlement. Some individuals have testified that their application for a mortgage was approved after three months of debt settlement.

Will debt collectors settle for 30%?

Lenders typically agree to a debt settlement of between 30% and 80%. Several factors may influence this amount, such as the debt holder's financial situation and available cash on hand.

Does debt settlement hurt your credit?

Debt settlement can negatively impact your credit score, but it won't hurt you as much as not paying at all. You can rebuild your credit by making all payments on time going forward and limiting balances on revolving accounts.

Will bankruptcy clear all debt?

Bankruptcy doesn't cover all debts so it's important to make sure you know whether any of your debts won't be covered and put plans in place to deal with them. You might need to: keep paying some debts while you're bankrupt. stop paying some debts, but start paying them again when your bankruptcy ends.

How long do settlements stay on credit report?

seven yearsA settled account remains on your credit report for seven years from its original delinquency date. If you settled the debt five years ago, there's almost certainly some time remaining before the seven-year period is reached. Your credit report represents the history of how you've managed your accounts.

How can I get out of debt without bankruptcy?

10 Simple Steps to Get Out of Debt Without Going into BankruptcyOrganize debts. ... Stop all credit card use. ... Trim the budget. ... Do not go shopping. ... Pay the minimum on all but the smallest. ... Reward yourself. ... Apply funds to next debt. ... Delay unnecessary purchases.More items...

How can I consolidate my debt without bankruptcy?

There are several ways to consolidate debt, including:Enrolling in a credit consolidation program through a nonprofit credit counseling agency. ... Taking out a debt consolidation loan through a bank, credit union or online lender.More items...•

What's the difference between Chapter 13 and debt consolidation?

A Chapter 13 bankruptcy reorganizes your debt into one lower monthly payment similar to a debt consolidation program so you only pay as much as you can afford for 5 years. It's essentially a debt consolidation, but without the requirement to pay off all of your debts.

Can debt consolidation hurt your credit?

Debt consolidation loans can hurt your credit, but it's only temporary. When consolidating debt, your credit is checked, which can lower your credit score. Consolidating multiple accounts into one loan can also lower your credit utilization ratio, which can also hurt your score.

What are the cons of debt consolidation?

4 key drawbacks of debt consolidationIt won't solve financial problems on its own. Consolidating debt does not guarantee that you won't go into debt again. ... There may be up-front costs. Some debt consolidation loans come with fees. ... You may pay a higher rate. ... Missing payments will set you back even further.

What Is Debt Settlement?

Debt settlement allows you to pay off a debt for less than what you owe. In a debt settlement program, you make an offer and negotiate with your creditor to lower your debt. Once you pay off the negotiated amount, usually as a lump sum, they report your debt as settled or paid.

How Does Bankruptcy Work?

There are two types of bankruptcies, Chapter 7 and Chapter 13. In a Chapter 7 case, you provide information about your income, expenses, assets, and debts. If you’re employed, you’re also required to submit recent tax returns and pay stubs.

Comparing Debt Settlements to Both Types of Bankruptcy

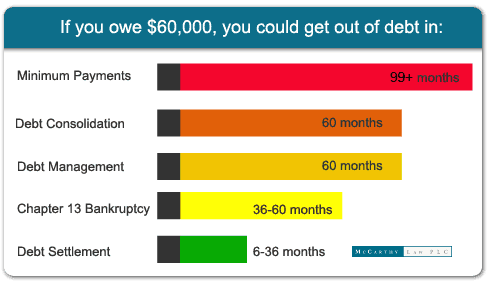

To decide whether debt settlement, Chapter 7 bankruptcy, or Chapter 13 bankruptcy is the best route for you, you’ll want to consider the time and cost of each, what ultimately happens to your debt, and what the effect will be on your credit report.

What are the least desirable routes toward financial recovery for those overwhelmed with unsecured debt?

Debt settlement and bankruptcy are the two least desirable routes toward financial recovery for those overwhelmed with unsecured debt. But if you’re in deep enough, one of these solutions could help you get your finances back in order.

What is the meaning of bankruptcy?

Bankruptcy. An agreement between a borrower and a creditor to reduce the amount of debt owed. When someone claims they can’t afford to pay their debt obligations and asks a bankruptcy court to discharge what they owe. Slightly less damaging to your credit than bankruptcy. Long-term negative impact on credit scores and credit report.

What is debt settlement?

Debt settlement is when you or a third party negotiates with creditors and lenders to pay less than what you owe. Bankruptcy is a legal process in which you petition a bankruptcy court to discard your debt or create a manageable payment plan. Learn more about the differences to figure out which option is right for you.

How long does bankruptcy stay on your credit report?

On the other hand, filing for bankruptcy removes the pressure of debt collectors, but it will become a part of your public record and remain on your credit report for up to 10 years.

How long does debt settlement stay on credit report?

Debt settlement is slightly less damaging to your credit than bankruptcy: Though debt settlement can cause your credit score to take a massive hit during the months that you stop paying your bills, once your debt is settled, it will remain on your credit report for seven years —shorter than the 10 years for Chapter 7 bankruptcy. 3

How long does bankruptcy affect credit?

Long-term negative impact on credit scores and credit report: Bankruptcies remain on your credit report for up to 10 years, and the immediate hit that your score will take will be drastic. Once your debt is discharged, however, your score can begin to improve again—assuming all other payment behaviors remain positive. 4.

What are the two forms of bankruptcy?

With bankruptcy, on the other hand, it most often comes in two forms: Chapter 7 and Chapter 13 .

What is Incharge Debt Solutions?

If bankruptcy is ultimately determined to be the best option for escaping your debt crisis, InCharge Debt Solutions offers bankruptcy education classes that will allow you to complete the credit counseling and debtor education requirements for entering and exiting bankruptcy.

What are the advantages of debt settlement?

Advantages to Settling a Debt: Access to free credit counseling that can help you create and negotiate a debt settlement plan. Pay only part of what you owe to become debt free. Use a debt settlement company to negotiate with creditors and avoid the time and expense involved in bankruptcy.

How does bankruptcy affect credit?

Both bankruptcy and debt settlement can reduce your creditworthiness and lower your credit, or FICO, score for years. Bankruptcy, no matter which chapter you file under, is certain to bring down your score. The better your score is to begin with, the more it will drop.

How to settle debt on your own?

If you decide to pursue debt settlement on your own, it will be vitally important that you educate yourself on the details of the debt that you owe, develop a realistic plan on how much you can save each month based on your current financial situation, and negotiate with creditors or collectors with a sensible repayment plan that they will agree to in writing.

What happens if your monthly debt exceeds 20%?

If your monthly debt payments, excluding mortgage or rent, exceed 20% of your income, you have a debt problem that requires action. The seriousness of the problem, and your ability and determination to overcome it, will determine whether a debt settlement plan or bankruptcy is the better option.

How long does debt settlement stay on your credit report?

Debt settlement will be on your credit report for seven years and definitely impact your ability to get a loan and the interest rate you pay, if you are approved. Debt settlement typically requires that you make a lump-sum payment to clear your account.

What happens if you stop paying your debt?

When you stop payments so you can save for a “lump-sum” offer, late-fee penalties and accrued interest will increase the size of your debt . If you settle a debt, state and federal tax collection will treat the forgiven amount as income and require you to pay taxes on it.

How is Chapter 13 bankruptcy different from Chapter 13 bankruptcy?

The biggest difference is that Chapter 13 bankruptcy terms are decided by the courts, not negotiated between you and your lender or creditor.

What is debt settlement?

Debt settlement is a common option for consumers seeking debt relief, especially when it comes to credit card debt. It’s all about paying less than what you owe. Either on your own or with the help of a debt settlement company, you can get settlement agreements with your various creditors that allow you to create a payment plan to repay a smaller percentage of what you owe.

Why is liquidation bankruptcy called liquidation?

It’s commonly called liquidation bankruptcy because it involves selling available assets that don’t qualify for an exemption for a lump sum payment for settling your debts. If you don’t have assets or your assets qualify for the exemption, you can get out of debt for close to nothing.

How to contact Debt.com?

By Debt.com. Free Debt Analysis. Contact us at (800)-810-0989. If you’re considering either option, it’s important to learn the truth about how they work and how they are different. They have different effects on the amount you owe, your credit score, credit reports, and financial future.

Is debt settlement good?

Going through a debt settlement company can be a good option for those who are behind on multiple accounts, but the accounts are still with the original creditor. Debt settlement companies handle all the settlement agreements for you, so you don’t have to interact with the lenders/creditors yourself anymore.

Is it better to settle debt or pay off debt?

So far, settlement probably sounds great. Before you choose to settle, make sure you know the cons to this method of debt relief. Yes, debt settlement is faster and cheaper. But it can also leave a negative mark on your credit score that could stay there for 7 years. It’s also likely that your credit score will drop.

Can you get out of debt with Chapter 13?

Both could get you out of debt relatively quickly, although with both a debt settlement program and Chapter 13 bankruptcy you will still make monthly payments for a period of time.

Is Chapter 7 Better Than Other Debt Relief Options

We mentioned a couple of ways that Chapter 7 would be better than other debt relief options above. Even though some people consider bankruptcy more of a last resort, you should not think of it that way. Ways that filing Chapter 7 may be the best debt relief option for you include:

Can I Negotiate A Credit Card Debt Settlement Myself

Yes, you can do DIY debt settlement, but it can be complicated, risky and damaging to your credit score. In addition, debt settlement requires you to go delinquent on your payments, which hurts your credit history and stays on your credit report for seven years.

Con: You May Continue A Cycle Of Debt

Although an unsecured personal loan could wipe out some or all of your existing debt, youll still be responsible for paying off new debt.

When To Consider Debt Settlement Or Bankruptcy

If your monthly debt payments, excluding mortgage or rent, exceed 20% of your income, you have a debt problem that requires action. The seriousness of the problem, and your ability and determination to overcome it, will determine whether a debt settlement plan or bankruptcy is the better option.

What Happens When I File Bankruptcy

Filing for bankruptcy after youve defaulted can protect your assets from being seized by the lender or creditor.

Pros And Cons Of Bankruptcy

Though it has a bad connotation, bankruptcy does have some pros worth discussing. Chapter 7 bankruptcy is one of the fastest ways to get out of debt even faster than debt settlement. Chapter 13 and Chapter 7 are clean breaks from your debt, but that doesnt come without a cost.

Debt Relief Vs Bankruptcy: Which One Is The Better Option

October 12, 2021/Tayne Law Group/ debt help, Debt Relief, debt settlement, From the Blog, Personal Finance /

What is Bankruptcy?

The U.S. constitution gives you the ability to seek relief from all or part of your debt in case you cannot repay it by filing for bankruptcy. The two main types of personal bankruptcies that apply to individuals include Chapter 7 and Chapter 13. Chapter 7 helps absolve you from all debt through a liquidation process, and Chapter 13 involves restructuring of your debt. Under Chapter 7, your non-exempt liquid assets are used to repay your creditors.

What Are the Pros and Cons of Bankruptcy?

This is because of the long-term effect that comes with the process. If you file for bankruptcy, its mention will remain in your credit reports for 7 to 10 years. This, in turn, makes getting any kind of credit during this period highly challenging.

Do You Qualify for Bankruptcy?

Qualifying for Chapter 7 bankruptcy requires that you pass a means test. This is to ensure that your income is lesser than your state’s median income based on your family size. Next, you have to receive counseling through a government-approved credit counseling agency. People who do not pass the means test have the option of filing for Chapter 13.