What is the current credit card interchange rate?

Interchange Rates

- Average Interchange Rates. The typical interchange rate is 1.7% - 2% for credit cards and 0.5% for debit cards. ...

- Visa Interchange Fees

- Mastercard Interchange Fees

- Discover Interchange Fees

- American Express Interchange Fees. American Express has a more complex fee structure. ...

- Ways to Save on Interchange Rates. ...

When will visa and MasterCard raise interchange fees?

Visa and Mastercard have both stressed that they do not directly benefit from the higher interchange fees, which they said are used by card issuing banks to fund new products and fight fraud. The separate plan to increase scheme fees will apply to transactions between the UK and the EU and take effect from July 2022.

What is the current interchange rate?

The typical interchange rate is 1.7% - 2% for credit cards and 0.5% for debit cards. Here are the average credit card processing fees for the 4 major credit card networks: Below, review some of the most common interchange fees you may encounter for each card association, as of April 2021.

How to dispute credit card transactions and fees?

In order to get your money back quickly, follow these five steps to dispute a credit card charge:

- Double check that the charge is actually incorrect. Make sure that the billing error is actually unauthorized and not a recurring charge or purchase you forgot about. ...

- Gather supporting documents. ...

- Work with the merchant. ...

- Contact your card issuer. ...

- Wait for a reply. ...

What is payment card settlement?

One option may be a credit card settlement, which is when your credit card company forgives a portion of the amount you owe in exchange for you repaying the remaining amount.

What was the outcome of the 2013 class action lawsuit against Visa and Mastercard?

In December 2013, U.S. District Court Judge John Gleeson approved a settlement in the case that amounted to $7.25 billion. The settlement lowers interchange fees for merchants and also protects credit card companies from being sued over the issue again in the future. That settlement was reversed.

Who pays Visa interchange fees?

Definition: Interchange fees are transaction fees that the merchant's bank account must pay whenever a customer uses a credit/debit card to make a purchase from their store. The fees are paid to the card-issuing bank to cover handling costs, fraud and bad debt costs and the risk involved in approving the payment.

How much will I get from Bank of America settlement?

What does the Settlement provide? Bank of America has agreed to establish a Settlement Fund of $27.5 million from which Settlement Class Members will receive payments or Account credits. The amount of such payments or Account credits cannot be determined at this time.

Why is this case against Visa and MasterCard being heard by the court?

The Rule 23(b)(3) Class Plaintiffs claim that: Visa, and its respective member banks, including the Bank Defendants, violated the law because they set interchange fees. Mastercard and its respective member banks, including the Bank Defendants, violated the law because they set interchange fees.

What accusations have been made against Visa and MasterCard?

The Department charges that Visa and MasterCard violated the antitrust laws by placing authority for their competitive decisions in the hands of banks that have significant financial interests in both networks - known in the banking industry as "duality." These governing banks have rejected competitive initiatives that ...

How do banks make money from interchange?

Banks Make Money With Interchange Fees You buy something for $100 with your debit card. The store would pay an interchange fee of $2.15. The store keeps $97.85 of the purchase price, and the $2.15 interchange fee goes to the bank that provided you with the credit or debit card.

How much do banks make on interchange fees?

In the United States, the average interchange rate is around 0.3% for debit cards and 1.8% for credit cards.

How much is the Visa interchange fee?

Business credit cards may have higher fees than consumer rewards credit cards. For example, Visa Business credit card has an interchange fee of 2.200 % + 10¢ while the Visa Rewards Traditional credit card has a fee of 1.650 % + 10¢.

What bank has the biggest lawsuit?

The settlement by BNP Paribas in the U.S. sanctions case for nearly $9 billion ranks among the biggest ever among banks since the early 2000s, and tops the list of those not related to the financial crisis. It is the biggest-ever fine levied against a bank for violating U.S. economic sanctions.

What's going on with the Bank of America lawsuit?

Bank of America is being sued by a customer who claims the bank “misrepresented” its free money transfer service and failed to warn her and others about the fees it could cause, court documents show.

What happened to Bank of America class action lawsuit?

Update: Bank of America agreed to pay $8 million to end class action claims it hit customers with multiple fees on the same checks in violation of their account agreements. Plaintiff Steven Checchia filed a motion June 9 in a Pennsylvania federal court, asking a judge to grant approval to the deal.

What percentage does Visa charge merchants?

Typical Costs From Major Credit Card CompaniesCredit CardAverage Interchange FeesVisa1.15% + $0.05 to 2.40% + $0.10Mastercard1.15% + $0.05 to 2.50% + $0.10Discover1.35% + $0.05 to 2.40% + $0.10American Express1.43% + $0.10 to 3.30% + $0.10Aug 19, 2022

How are interchange fees split?

Interchange fees are split up between some of the money going to the card-issuing bank – like Chase or Bank of America – while the rest of the fees go to the card brand.

Do banks pay Visa?

The fees, roughly 1 to 3 percent of each purchase, are forwarded to the cardholder's bank to cover costs and promote the issuance of more Visa cards. The banks have used interchange fees as a growing profit center and to pay for cardholder perks like rewards programs.

Which category decides the interchange fee?

An interchange fee is an amount that the issuing institutions collect from the acquiring bank. Usually, this fee is a percentage of the total transaction plus a fixed amount. And while the issuing institutions collect, assess and set this fee, they are paid to the issuing bank, who issue a particular card.

What banks conspired to artificially inflate interchange fees?

Plaintiffs allege that, between January 1, 2004 and the January 25, 2019, Defendants Visa, MasterCard and several banks including Bank of America, JPMorgan Chase and Citigroup conspired to artificially inflate the prices of interchange fees that merchants' acquiring banks pay to customers' issuing banks in a credit or debit card transaction. Since the interchange fees are inflated, the discount fees merchants pay to accept card payments are in turn artificially high, and various rules prevent merchants from challenging the inflated fees.

What is the deadline for a pending settlement?

Pending Settlements: Filing Deadline: $5.54 to $6.24 Billion. Not yet established; Claim forms are not yet available.

What is SRG in class action?

SRG is a third party service that can be hired to file and track claims. We specialize in helping companies file claims to obtain their share of settlement money from class action lawsuits once a settlement has been reached. Our services are voluntary and are not required to file a claim. No-cost assistance will be available from the Class Administrator and Class Counsel during any claims-filing period. Official documents and information on the case can be found on the Court-approved case website www.paymentcardsettlement.com. This summary is not and should not be construed as legal, tax or other professional advice.

Does SRG require additional information?

Please note that SRG may require additional information from you (the claimant) in order to meet requirements for the Payment Card Interchange Fee Settlement. In consideration for SRG filing a claim and seeking reimbursement on the claimant’s behalf, claimant agrees to pay SRG 25% of the face value of the reimbursement.

Where is the In re Payment Card Interchange Fee and Merchant Discount Antitrust Litigation?

The docket number is 05-md-01720. The United States District Court in the Eastern District of New York in Brooklyn is the venue.

Who is the senator who proposed the settlement on credit card swipe fees?

Richard Durbin , the senator from Illinois who was the main proponent of those rules, has called the proposed settlement on credit card swipe fees, "gives Visa and MasterCard free rein to carry on their anti-competitive swipe-fee system with no real constraints and no legal accountability.

What was the settlement of the Dodd-Frank bill?

Dodd-Frank required the Federal Reserve to write rules for swipe fees on debit card purchases. Richard Durbin, the senator from Illinois who was the main proponent of those rules, has called the proposed settlement on credit card swipe fees, "gives Visa and MasterCard free rein to carry on their anti-competitive swipe-fee system with no real constraints and no legal accountability. This is not a settlement I would agree to. I hope that the remaining merchant plaintiffs will review the proposed settlement carefully and think hard about whether it will be good for the future of our credit- and debit-card systems.” Barney Frank, a representative from Massachusetts and a primary supporter of legislation to repeal rules on debit card swipe fees said he supports the settlement and stated, "A free-market approach in this area will be better for the economy and all concerned parties.”

What did the plaintiffs argue about the settlement?

The plaintiffs argued that the settlement violated their rights by not allowing them to opt out of some provisions. The inability to opt out of litigation releases that bar future suits was an important point of contention. Jeff Shinder, a lawyer for the plaintiffs said, "The proposed settlement violates the due process rights of millions of merchants by denying them the ability to opt out of the injunction, and this fundamental issue of law should be addressed now before notice goes out to merchants."

What is swipe fee?

Plaintiffs allege that Visa, Mastercard, and other major credit card issuers engaged in a conspiracy to fix interchange fees, also known as swipe fees, that are charged to merchants for the privilege of accepting payment cards, at artificially high levels. In their complaint, the plaintiffs also alleged that the defendants unfairly interfere with merchants from encouraging customers to use less expensive forms of payment such as lower-cost cards, cash and checks.

When will the swiping fee be reversed?

That settlement was reversed. Currently one for US$ 6.24 billion is scheduled to go before the district court on November 7, 2019. Terminals for swiping credit cards, and origin of the term "swipe fee".

Who opposes the Safeway settlement?

Opposition. According to court filings, Target, Wal-Mart, Home Depot, Neiman Marcus, Saks, and 1,200 other plaintiffs oppose the settlement. A group of large merchants including Kroger, Walgreens, and Safeway have reached a separate agreement with the defendants over swipe fees.

What is interchange fee?

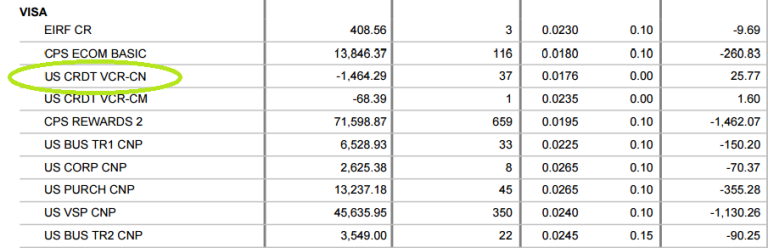

Interchange fees typically account for the greatest part of the fees paid by merchants for accepting Visa and Mastercard cards. Visa and Mastercard set interchange fee rates for different kinds of transactions and publish them on their websites, usually twice a year. Back to Top.

When will the settlement fund be paid?

The amount paid from the settlement fund will be based on your actual or estimated interchange fees attributable to Visa and Mastercard card transactions (between you and your customers) from January 1, 2004 through January 25, 2019.

What happens if you don't exclude yourself from the settlement?

If you did not exclude yourself from the Rule 23 (b) (3) Settlement Class, you cannot be part of any other lawsuit against Defendants and other released parties listed in the Rule 23 (b) (3) Class Settlement Agreement for released conduct. You will be bound by the Rule 23 (b) (3) Settlement Class Release, except that as to the declaratory and injunctive relief claims asserted in the pending proposed Rule 23 (b) (2) class action captioned Barry’s Cut Rate Stores, Inc., et. al. v. Visa, Inc., et al., MDL No. 1720, Docket No. 05-md-01720-MKB-JO, you will continue to have all rights pursuant to Rule 23 of the Federal Rules of Civil Procedure which you have as a named representative plaintiff or absent class member in that action, except the right to initiate a new separate action before five (5) years following the court’s approval of the settlement and the exhaustion of all appeals. The July 23, 2019 deadline for requesting exclusion from the Rule 23 (b) (3) Settlement has now passed.

What is the hearing about in the settlement?

The hearing was about whether or not the settlement is fair, adequate, and reasonable.

How to contact Judge Brodie?

1-800-625-6440. 1-800-625-6440 - toll-free. If you do not get a Claim Form in the mail or by email, you may download one at this website, or call: 1-800-625-6440. Please Do Not Attempt to Contact Judge Brodie or the Clerk of Court With Any Questions.

When is the final approval of the settlement?

On December 13, 2019, the Court granted Final Approval to the settlement, which is now under appeal (see " The Court’s Fairness Hearing "). Once the appeals process is complete, the court will then finalize the claim form and set a deadline for members of the Rule 23 (b) (3) Settlement Class to submit claims.

Who are the defendants in a lawsuit?

The companies that the plaintiffs have been suing are the “Defendants.” Defendants are:

When did the interchange fees settlement happen?

The Court granted final approval of this Settlement on December 13, 2019, and will establish a claims process whereby eligible merchants will be able to claim their share of the billions in settlement funds.

What is reconciliation with settlement administrator?

Reconcile with the Settlement Administrator to help ensure that you receive a proper and timely recovery.

How to contact MCAG?

Need more information? Call MCAG at 1-800-355-0466 to learn more or CLICK HERE to complete our contact form and an MCAG representative will respond shortly.

What is the lawsuit against Visa and Mastercard?

The lawsuit claims that Visa and Mastercard, separately, and together with certain banks, violated antitrust laws and caused merchants to pay excessive fees for accepting Visa and Mastercard credit and debit cards. The defendants say they have done nothing wrong and the Court has not decided who is right, but the parties have agreed to a settlement.

What is the purpose of the notice of settlement for Visa and Mastercard?

District Court for the Eastern District of New York to inform merchants about an agreement to settle a class action lawsuit that may affect them. The lawsuit claims that Visa and Mastercard, separately, and together with certain banks, violated antitrust laws and caused merchants to pay excessive fees for accepting Visa and Mastercard credit and debit cards. The defendants say they have done nothing wrong and the Court has not decided who is right, but the parties have agreed to a settlement. The Court has now given preliminary approval to this settlement.

When will the net class settlement fund be used?

The net class settlement fund, after deducting court-awarded attorneys' fees and costs, will be used to pay valid claims of merchants that accepted Visa or Mastercard credit or debit cards at any time between January 1, 2004 and January 25, 2019.

Do merchants have to fill out a claim form?

To receive payment, merchants will be required to fill out a claim form. Claims cannot yet be filed. If the Court grants final approval, and if that approval is affirmed on any appeals, the Court will approve a claim form and set a claim deadline. Claim forms will then be mailed to all identified merchants.

Who is bound by the terms of the settlement agreement?

Members of the Settlement Class who do not exclude themselves by the deadline will be bound by the terms of this settlement, including the release of claims against the released parties provided in the settlement agreement, whether or not the members file a claim for payment.

Can you exclude yourself from a settlement?

Exclude themselves from the Settlement Class. Merchants who exclude themselves will not get any money from this settlement but can individually sue the Defendants on their own at their own expense, if they want to. Merchants who wish to exclude themselves must make a written request, place it in an envelope, and mail it with postage prepaid and postmarked no later than July 23, 2019, or send it by overnight delivery shown as sent by July 23, 2019, to Class Administrator, Payment Card Interchange Fee Settlement, P.O. Box 2530, Portland, OR 97208-2530.

How long does a MCAG settlement last?

MCAG will gather historical data over the fifteen-year settlement period that pertains to all of your business locations, across multiple processors, and submit multiple claims. MCAG’s extensive expertise in analyzing merchant sales data reduces your potential burden with the submission process, including:

What is a MCAG fee?

MCAG’s services are optional to merchants and there are no upfront fees. MCAG charges a 25% contingent fee of any recoveries that you may be entitled to from this settlement. For this fee, MCAG services include the necessary data analysis, document preparation, claims filing, recovery, and reconciliation for your business. If no money is recovered, MCAG will not charge or retain a fee.

Is there a settlement for a class action?

The Court has granted final approval of a settlement to resolve the class action. Claim forms are not yet available and class members need not sign up for a third-party service to recover settlement funds. Once a claims process is available, no-cost assistance will be available from the Class Administrator and Class Counsel. Additional information regarding the litigation is available on the Court-approved website at www.paymentcardsettlement.com.

Can you file a claim with MCAG?

Claims forms are not yet available, but you can engage MCAG now to help ensure that a proper and timely claim is filed on behalf of your business.