In general, paying off your debt in full is a better option than debt settlement because it will not harm your credit score. Debt settlement, on the other hand, can help you get out of debt faster and at a lower cost by making a single lump sum payment.

Is it better to settle debt or pay off in full?

Paying off your debt in full without settling will cost you more, but it’s the fastest way to get out from under your debt because settling it is not a quick process. And taking longer to pay off your debt by waiting for a settlement offer to come through can damage your credit score further.

What does it mean when a debt is settled in full?

“Settled in Full” – typically means that a consumer did not pay the full balance and settled the account. The creditor will show no balance on the credit report indicating that there is no more debt obligation. “Paid in Full” – typically means that a consumer did pay the full balance and settled the account.

What does it mean to settle a debt with Experian?

According to Experian, "Settling a debt means that you have negotiated with the lender, and they have agreed to accept less than the full amount owed as final payment on the account." When this occurs, the credit agencies will be notified that the account has been "settled" or "account paid in full for less than the full balance".

What does it mean when a debt is paid in full?

Generally speaking, having a debt listed as paid in full on your credit reports sends a more positive signal to lenders than having one or more debts listed as settled. Payment history accounts for 35% of your FICO credit score, so the fewer negative marks you have—such as late payments or settled debts—the better.

Does paying off a settlement hurt your credit?

Debt settlement can negatively impact your credit score, but it won't hurt you as much as not paying at all. You can rebuild your credit by making all payments on time going forward and limiting balances on revolving accounts.

Does a settlement look better than a charge off?

Generally speaking, having a debt listed as paid in full on your credit reports sends a more positive signal to lenders than having one or more debts listed as settled. Payment history accounts for 35% of your FICO credit score, so the fewer negative marks you have—such as late payments or settled debts—the better.

Is it better to make payments on collections or pay in full?

Paying your debts in full is always the best way to go if you have the money. The debts won't just go away, and collectors can be very persistent trying to collect those debts. Before you make any payments, you need to verify that your debts and debt collectors are legitimate.

Can I get a mortgage after debt settlement?

Most lenders won't want to work with you immediately after a debt settlement. Settlements indicate difficulty with managing financial obligations, and lenders want as little risk as possible. However, you can save enough money and buy a new home in a few years with the right planning.

How do I remove a settled account from my credit report?

Review Your Debt Settlement OptionsDispute Any Inconsistencies to a Credit Bureau.Send a Goodwill Letter to the Lender.Wait for the Settled Account to Drop Off.

How can I get a charge off removed without paying?

How to Remove a Charge-Off Without PayingNegotiate with the Creditor. Negotiating with the creditor usually still involves paying some of the debt. ... Consult with a Credit Repair Company – Buyer Beware. ... Secured Credit Cards. ... Credit Utilization. ... Pay Bills on Time. ... Unsecured Credit Cards. ... Authorized User. ... Credit Rebuilder Loans.More items...•

How long after paying collections will credit score improve?

How long does it take for my credit score to update after paying off debt? It can often take as long as one to two months for debt payment information to be reflected on your credit score. This has to do with both the timing of credit card and loan billing cycles and the monthly reporting process followed by lenders.

Can original creditor remove charge off?

First, creditors aren't obligated to honor your request and remove charge-offs from your credit. So while you can ask for a pay-for-delete, there's no guarantee that a creditor or debt collector will agree to it. Second, if they do agree, you'll likely need to pay the account in full.

How many payments do you have to make to settle a debt?

That last part is important, as debt settlement usually requires you to make a lump sum payment. Some creditors may allow you to break it up into two or three payments in the case of larger debts. But this still means you’ll need to have cash on hand to settle with.

What does it mean to settle a debt?

A settled debt simply means that a creditor has agreed to accept less than what’s owed as final payment. There are companies that offer debt settlement or debt relief services, and it’s also possible to work out a settlement with creditors yourself.

What is a debt counselor?

A credit counselor or debt counselor can look at your debts, income and spending to help you create a realistic budget. They can also discuss different options for debt repayment, including whether a debt management plan (DMP) might be right for you. This debt payoff strategy involves making one payment to the credit counselor, who then distributes the payment among your creditors.

What is debt consolidation loan?

A debt consolidation loan is another option. Debt consolidation loans allow you to pay off multiple debts and then make one payment to the loan going forward. A debt consolidation loan or personal loan could make sense for paying off debt if you need to borrow a larger amount of money and if you can qualify for a lower interest rate.

How long do you have to be behind on your credit card payments to settle?

So, you may need to be 90 to 180 days behind on your payments before a creditor may be willing to settle for less in lieu of charging off the debt altogether. If the creditor is reporting those late payments to the credit bureaus, then those late payments have already done their damage.

How to deal with debt when overwhelmed?

Being overwhelmed by debt can make you feel as if your options are limited; in fact, you have a full range of options—from debt consolidation, to debt management, to debt settlement—as well as resources that can help you, including debt counselors. By looking carefully at your debt and your available options, the best choice will become clearer.

How long does a late payment on a credit report last?

Late payments can linger on your credit reports for up to seven years, although their impact on your scores does fade over time. A settled debt status could add to the negative impact, at least in the near term until those accounts age on your credit reports.

Why trust us?

Our editorial team and expert review board work together to provide informed, relevant content and an unbiased analysis of the products we feature. The editorial content on our site is independent of affiliate partnerships and represents our unique and impartial opinion. Learn more about our partners and how we make money .

Summary

If you find yourself with enough cash to pay off maxed-out card debt, consider your options first, including impact on your score, taxes and fees.

I have a lump sum I can use to pay off maxed-out cards. Should I pay them in full or settle for less?

Since both paying in full and settling will eliminate your credit card debt, you should consider cost savings and the impact of your score of each possible option.

Cost savings of paying off card debt

Like it or not, paying full price is often the quickest and most convenient way to resolve a problem account.

Score recovery due to paying off card debt

While we know your score has dropped almost 200 points to 498, and your cards are maxed out, we don’t know how timely you’ve paid these cards in the past.

When card debt is reported as charge-off

Once a charged-off debt has been settled, the creditor will typically begin reporting the account to the credit bureaus as having been “settled for less than the full amount due.”

When card debt is sent to collections

Whereas a recent debt settlement can hurt the score when replacing a charge-off as the latest negative status, the worst, and last, step along this timeline is much less complicated.

What happens if you pay off debt in full?

If you can pay off the debt in full, you will prevent it from being reported as bad debt – and it will show that way on your credit report. Another upside: You won’t have to deal with the IRS. Advertisement. Advertisement.

How long does it take to settle a debt?

Third, you need to be patient, because debt settlement can take 18 months to four years. Fourth, you need to be OK with the settlement dragging down your credit score for seven years.

How long does a charge off stay on your credit report?

Even worse, you’re not even allowed to make minimum payments – yet the credit card issuer might continue to report the amount as past due. Once a charge-off goes on your credit report, it can say there for seven years.

Can a reader pay off his debts?

A reader can pay off his old debts, but he’s wondering if it’s better not to.

Is debt settlement a real option?

Debt settlement is a real option for some struggling people, but it doesn’t sound like you’re struggling right now, Ryan. Of course, that’s the final piece to this puzzle. Decisions like these aren’t made in a vacuum. If we were meeting to discuss this, I’d ask about the rest of your life. While you have the money now to pay in full, do you have anything else saved? Are you facing big expenses coming up? Is your job secure?

How does debt settlement work?

The companies generally offer to contact your creditors on your behalf, so they can negotiate a better payment plan or settle or reduce your debt.

What is debt settlement?

Debt settlement is a practice that allows you to pay a lump sum that’s typically less than the amount you owe to resolve, or “settle,” your debt. It’s a service that’s typically offered by third-party companies that claim to reduce your debt by negotiating a settlement with your creditor. Paying off a debt for less than you owe may sound great at first, but debt settlement can be risky, potentially impacting your credit scores or even costing you more money.

How many payments do you have to make to a debt collector?

Once the debt settlement company and your creditors reach an agreement — at a minimum, changing the terms of at least one of your debts — you must agree to the agreement and make at least one payment to the creditor or debt collector for the settled amount.

What happens if you stop paying debt?

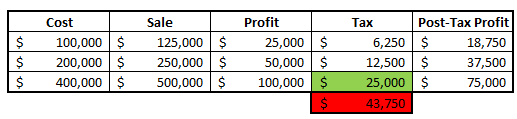

If you stop making payments on a debt, you can end up paying late fees or interest. You could even face collection efforts or a lawsuit filed by a creditor or debt collector. Also, if the company negotiates a successful debt settlement, the portion of your debt that’s forgiven could be considered taxable income on your federal income taxes — which means you may have to pay taxes on it.

How much debt has Freedom Financial resolved?

Why Freedom Financial stands out: Freedom Financial says it has resolved over $12 billion in debt since 2002. The company offers a free, “no-risk” debt relief consultation to help you decide if its program might work for you.

Can a company make a lump sum payment?

The company may try to negotiate with your creditor for a lump-sum payment that’s less than the amount that you owe. While they’re negotiating, they may require you to make regular deposits into an account that’s under your control but is administered by an independent third-party. You use this account to save money toward that lump payment.

Who can check if a debt settlement company is licensed?

The state attorney general’s office can also check if the company is required to be licensed and whether it meets your state’s requirements. The Better Business Bureau has consumer reviews of businesses that could help you as you research a debt settlement service provider.

How to settle debt?

The pros of settling debt: 1 Your credit score damage decreases as your credit utilization decreases . Notice the difference between the heading of this paragraph and that of #1 above. This paragraph heading doesn't mention an increase in your credit score. It does, however, get rid of any lingering score damage caused by having accounts with high credit utilization. So although it does help stop more score damage from occurring, settling debt most likely won't increase your score. 2 Lower monthly payments. Since your debts will be "settled", you will pay less than you initially owed on the account. Sometimes, the amount you'll pay can be 50% less than you were paying for the original debt - saving you money down the line.

What happens when you stop paying debt settlement?

This adds up to more late fees, interest and other potential penalties.

What are the pros and cons of paying off debt?

A con of paying off a debt in full is that the money you used to pay off the debt can't be used elsewhere. If you want to save, invest or spend the money on education, you'll have to wait until you start to build up more resources. You'll have to make the decision which is more important to you: using the money for something else or paying off debt. This can sometimes be a very difficult choice.

How does paying off debt feel?

You'll have less stress in your life. Paying off debt can sometimes feel like a huge weight has been taken off your shoulders. You've thought about it... worried about it... wondered what to do about it...

How long does a settled account stay on your credit report?

The fact that your account (s) was settled and that you didn't pay the full amount, remains on your credit report for 7 years. This could make it more difficult to get future credit from lenders. Tax Consequences. Yes, the IRS is on the lookout for those who have settled accounts.

Does credit score increase with debt?

Your credit score could increase as your credit utilization decreases. Since the debt has probably negatively impacted your payment history (and possibly other credit score factors), your score won't immediately shoot through the roof. However, over time, if no more debt is accumulated, you should see your score rise.

Does settlement affect credit score?

Credit Score Impact. Settling debt, like charging-off it off, is seen as derogatory. It will have a negative impact on your credit score - as will missing payments while negotiating the settlement.

How does the paying a debt effect the credit score?

The credit score weighs more heavily on whether a negative account is When the account was placed on the credit report and last updated, has a Balance, and the Rating of the Account

What does "settled in full" mean?

“Settled in Full” – typically means that a consumer did not pay the full balance and settled the account. The creditor will show no balance on the credit report indicating that there is no more debt obligation.

What does "paid in full" mean on credit report?

“Paid in Full” – typically means that a consumer did pay the full balance and settled the account.

What credit reporting agencies can put a debt on your credit report?

The Credit Reporting Agencies (CRA’s) like Experian, Equifax, and TransUnion can place entries on a credit report after a debt has been paid with the creditor or debt collector showing the accurate status of the acccount and how it was paid.

How old is a zero balance on a mortgage?

Some consumers are forced to pay a debt to obtain a zero balance for a FHA and conventional mortgage. Again once paid and the zero balance is older than 24 months old then the credit score will tend to ignore the negative account. The Rating is the last important factor for how a paid account will reflect in the credit score.

How long does it take for a zero balance to be updated?

Once a zero balance item is updated on the credit report for more than 24 months the score almost ignores it. It has little effect on a credit score. When a negative account has a Balance reporting the credit scoring algorithm looks at it unfavorably because a consumer has not paid their alleged debts. Some consumers are forced to pay a debt ...

What happens if you have a negative credit report?

If a negative account was placed on the credit report over 2 years ago then it could have a major impact lowering your credit score when payment is made. If the debt is older and you must settled the debt then time will heal the damage.

How to pay off a deficiency balance?

The best method for paying off a deficiency balance is to pay the entire balance in full— and if that isn't possible, the next best option is to work out a payment plan.

What happens if you reaffirm your debt under Chapter 7?

If you reaffirm your debt with the lender under Chapter 7, they will promise not to repossess your car again so long as you continue to make your payments. 5

How long can collections try to collect a deficiency balance?

Statutes of limitations for debt vary by state and by type of debt. In general, debt is collectible for three or six years —but some forms of debt in some states can be collected for more than a decade. Keep in mind that, aside from the other negative consequences that come with ignoring debt, there are also actions you can take that inadvertently restart the clock on the debt's timeline.

What happens if you owe $3,000 on a car?

For example, if you still owe $3,000 on your vehicle, and the lender only manages to fetch $2,500 for it at auction, you will have a deficiency balance of $500. You have an obligation to pay off this debt. 1 . Your lender may also require that you pay the cost of repossessing, storing, and selling the vehicle, ...

What happens if you sell your car for less than you owe?

If your car has been repossessed and sold for less than what you owe on the loan, the difference is called a deficiency balance.

What happens if you don't pay your car loan in 2021?

Updated January 26, 2021. If you fall behind on your car loan payments, your auto loan servicer may have the right to repossess your vehicle . If you don't pay them what you owe on the loan, this is one of the few options open to them. They may then sell the car or keep it as compensation for your debt.

Does bankruptcy help pay interest?

Bankruptcy may also help you pay a lower amount or lower interest costs, depending on whether you file Chapter 7 or Chapter 13. 3 . If you reaffirm your debt with the lender under Chapter 7, they will promise not to repossess your car again so long as you continue to make your payments. 5 .