Full Answer

How to negotiate a loan settlement?

To settle a private student loan:

- For private student loans, there is no database to see all of your outstanding loans. ...

- Contact your lender to let them know you would like to settle your student loan.

- Use a polite tone to start the conversation off on a positive note.

- Let your private student loan lender make the initial offer. ...

How to calculate full settlement on your personal loans?

To use it, all you need to do is:

- Enter the original Loan amount (the full amount when the loan was taken out)

- Enter the monthly payment you make

- Enter the annual interest rate

- Enter the current payment number you are at - if you are at month 6, enter 6 etc.

- Click Calculate!

Can I take a loan against my structured settlement?

The short answer is, no, you cannot get a structured settlement loan. Structured settlement loan rates don’t matter because you cannot, legally, take out a loan against your structured settlement.

Can I get a settlement loan?

You can start requesting a loan settlement in delinquency, but only if it’s on its way to default. You can also request a settlement once your loan has passed into default. You might qualify for a student loan debt settlement with your federal loans if:

What happens in loan settlement?

Personal loan settlement process, also known as personal loan defaulter settlement refers to an agreement between a lender and a borrower wherein the loan is 'settled' by repaying only a part of the loan. The lender may forgive a part of the debt in order to help the borrower repay the loan at least partially.

What does settle a loan mean?

Settling a debt means you have negotiated with the lender and they have agreed to accept less than the full amount owed as final payment on the account. The account will be reported to the credit bureaus as "settled" or "account paid in full for less than the full balance."

Is it a good idea to settle debt?

It's a service that's typically offered by third-party companies that claim to reduce your debt by negotiating a settlement with your creditor. Paying off a debt for less than you owe may sound great at first, but debt settlement can be risky, potentially impacting your credit scores or even costing you more money.

Does settling loan hurt your credit?

Loan settlements impact on the CIBIL score When a loan is termed settled, it is viewed as a negative credit behaviour and the borrower's credit score drops by 75-100 points. The CIBIL holds this record for over 7 years.

Can I get loan after settlement?

The bank or lender takes a look at the borrower's CIBIL score before offering him a loan and if the past record shows any settlement or non-payment, his loan is likely to get rejected.

How long does it take to improve credit score after debt settlement?

between 6 and 24 monthsHowever, a debt settlement does not mean that your life needs to stop. You can begin rebuilding your credit score little by little. Your credit score will usually take between 6 and 24 months to improve. It depends on how poor your credit score is after debt settlement.

Is it better to settle or pay in full?

Generally speaking, having a debt listed as paid in full on your credit reports sends a more positive signal to lenders than having one or more debts listed as settled. Payment history accounts for 35% of your FICO credit score, so the fewer negative marks you have—such as late payments or settled debts—the better.

What are the consequences of debt settlement?

Debt settlement can cause your credit score to fall by more than 100 points, and it stays on your credit report for seven years. If your creditors close accounts as part of the settlement process, this can cause your credit utilization to increase, which also negatively affects your credit score.

How long does a settlement stay on your credit report?

seven yearsA settled account remains on your credit report for seven years from its original delinquency date. If you settled the debt five years ago, there's almost certainly some time remaining before the seven-year period is reached. Your credit report represents the history of how you've managed your accounts.

How do I remove a settled debt from my credit report?

You can remove a settled account that's past the 7-year rule from your credit report. If it still appears on your credit report, then you have to file a dispute with the credit bureaus to delete it.

How do I raise my credit score after a settlement?

How to Improve CIBIL Score After Loan Settlement?Build a Good Credit Repayment History. ... Clear off Pending Dues. ... Manage Credit Cards Better. ... Apply for a Secured Card. ... Credit Utilisation. ... Do Not Raise Frequent Loan Queries. ... Apply for a Secured Credit.

What happens if you pay a settlement offer?

As long as your creditors accept your offer – i.e. agree to sum of money in the settlement offer – they will accept partial settlement of your debt in exchange for writing off the remaining amount you owe. If the settlement offer is big enough, the money will be shared equally among all of your creditors.

Is it better to settle or pay in full?

Generally speaking, having a debt listed as paid in full on your credit reports sends a more positive signal to lenders than having one or more debts listed as settled. Payment history accounts for 35% of your FICO credit score, so the fewer negative marks you have—such as late payments or settled debts—the better.

Whats the difference between settling a debt and paying in full?

Should I pay in full or settle instead?" Paying in full means paying the total amount of your debt. Settling in full means coming to an agreement with your creditor or collection agency on an updated payment plan. While this may seem simple, there are nuances to how lenders look at the two on your credit report.

How much should you offer to settle a debt?

When you're negotiating with a creditor, try to settle your debt for 50% or less, which is a realistic goal based on creditors' history with debt settlement. If you owe $3,000, shoot for a settlement of up to $1,500.

How can I settle my personal loan fast?

How to repay personal loan faster - some tips and tricks to followExamine what you owe. ... Analyse your income and obligations. ... Transfer your loan to a lender offering a lower interest rate. ... Make one extra payment. ... Round up your loan payment. ... Use your variable pay to pay off a chunk of your loan.

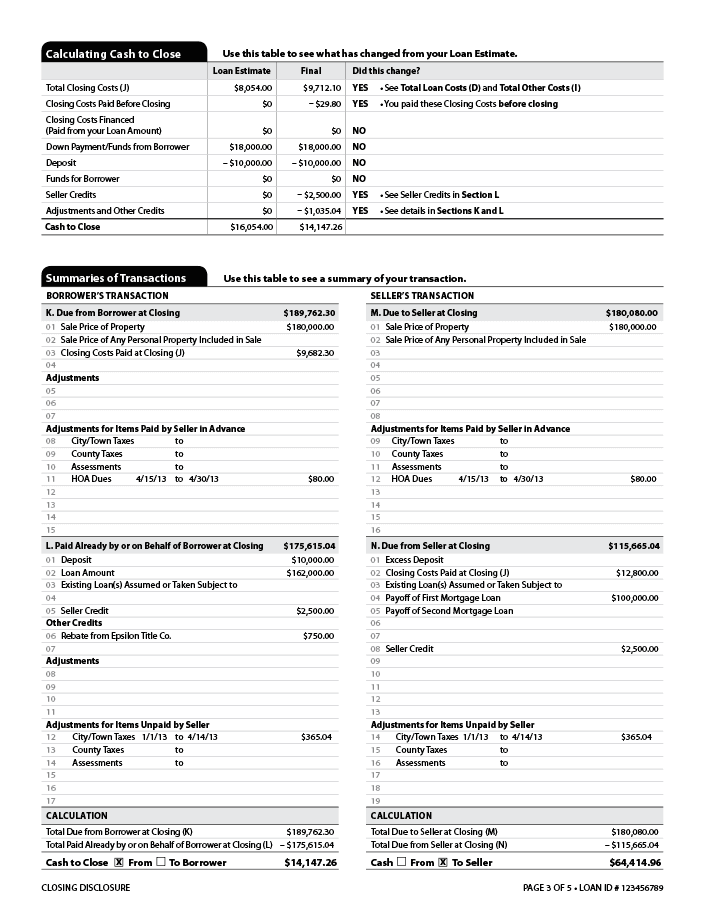

What is a loan settlement statement?

A loan settlement statement is the document that describes the amount of a loan, typically for a mortgage, given to the borrower once the loan has been settled. In addition to the amount, the settlement statement will also contain the frequency of installments expected from the lender in regards to repayment.

Is a loan settlement statement different from a normal settlement statement?

Quick answer: yes. It's not uncommon to mix the two up, though, because a "settlement statement" is another document that's involved in buying a home. So how do you keep track of which one is which?

Is there any downside to settling a loan early?

On the surface, paying off your loan before the terms agreed to seems like an obvious decision. If you're looking at a mortgage, it's likely that this is going to be the largest debt that you encounter in your lifetime, and the faster you settle your debt, the less interest you'll pay. Seems like a clear-cut decision, right?

What is Loan Settlement?

Loan settlement is also known as debt arbitration. It is an approach, through which both debtor and creditor come to a middle ground on the final loan settlement amount, which is less than the total outstanding amount, to close the loan account.

How does Loan Settlement Work?

The one-time loan settlement option is not offered to all debtors. First, the lender needs to verify and confirm, the default happened due to a genuine reason that is beyond the control of the debtor.

How Does Loan Settlement Affect Your Credit Score?

Accepting a one-time loan settlement offer and repaying the loan amount along with interest within the due date are two different scenarios.

How to Avoid Loan Settlement and Deal with the Situation?

A one-time loan settlement offer may look like an attractive option because of the reduced pay, but accepting the offer is not a financially wise decision. It should be your last option.

How to Improve Your Credit Score?

A low credit score always exposes a lender to a high risk of default. Therefore, banks or lenders are often unwilling to offer credits to individuals who have a low credit score and who have defaulted on loan payments in the past.

How to avoid multiple credit cards?

Avoid taking multiple credit cards or loans unless you really need to. Pay off your monthly EMIs on time. Keep monitoring your CIBIL Score at regular intervals to keep a track of your financial performance. When you opt for loan settlement, don’t apply for a new loan immediately.

What is personal loan settlement?

Personal loan settlement process, also known as personal loan defaulter settlement refers to an agreement between a lender and a borrower wherein the loan is ‘settled’ by repaying only a part of the loan. The lender may forgive a part of the debt in order to help the borrower repay the loan at least partially.

What happens if you settle a personal loan?

When you opt for a personal loan defaulter settlement, it negates the original credit agreement between you and your lender. Also, when your lender reports the same to credit rating agencies as ‘ settled’ instead of ‘paid as agreed’ or ‘paid in full’- it will have a negative impact on your credit score, and discourage other lenders ...

What is loan closure?

Loan closure is a term that refers to the closing of an existing loan account after the borrower repays the loan fully on time. This will have a positive impact on one’s credit score.

How does a loan settlement affect your credit score?

Loan settlement process can negatively affect your credit history and reduce your credit score drastically thereby limiting your chances of receiving credit in the future. When you opt for a loan settlement, even if it is for a genuine reason, the amount paid will be lesser than the original amount which reduces your creditworthiness.

What to do if you can't repay a loan?

In case you are unable to repay your loan due to unavoidable circumstances, then one of the options available is loan settlement. However, this is not a recommended option due to various reasons, one of which includes the adverse impact on your credit score.

How do settlement loans work?

To take out a settlement loan, you apply for a loan after filing an eligible lawsuit. The lawsuit loan company evaluates your case’s merit, weighs your chances of winning the suit or the case being settled, and estimates how much you can expect to receive. Based on that information, it may offer you an advance.

What is settlement loan?

Settlement loans give you a cash advance against an expected legal settlement. While you can get the cash you need to pay for necessary expenses right away, there are significant drawbacks to keep in mind.

What are some alternatives to settlement loans?

If you need cash, there may be other ways to get the money without resorting to a lawsuit advance. Consider a personal loan. If you have good credit, taking out a traditional personal loan can be a smart option.

How much interest do settlement loans cost?

Most notably, they can come with very high costs. Settlement loans typically have high interest rates. Interest rates commonly range from 20% to 60% a year. A study by University of Texas School of Law researchers found the average interest rate for settlement loans is 44%. Lawsuits can take years to settle.

What happens if you get injured in a medical malpractice case?

If you were injured in an accident or as a result of medical malpractice, there’s a chance that you’re unable to work. As a result, you could fall behind on your bills. A settlement advance gives you the cash you need to cover your living expenses and bills before a judgment is issued or the case is settled.

What does a lawsuit advance cover?

You’ll get money for living expenses. With a lawsuit advance, you’ll get cash to cover your necessary expenses, which can help you keep up with your bills.

How long does it take to get a settlement loan?

You can generally get the loan quickly. Some settlement lenders may be able to approve and fund your advance within hours or days.

What is a loan settlement statement?

A loan settlement statement is the document that describes the amount of a loan, typically for a mortgage, given to the borrower once the loan has been settled. In addition to the amount, the settlement statement will also contain the frequency of installments expected from the lender in regards to repayment.

Is a loan settlement statement different from a normal settlement statement?

Quick answer: yes. It's not uncommon to mix the two up, though, because a "settlement statement" is another document that's involved in buying a home. So how do you keep track of which one is which?

What does a loan settlement statement look like?

As an example, let's say you were approved for a mortgage valued at $200,000 to be paid back over 10 years with a 4% interest rate for the purchase of a property worth $235,000. Now let's say that you and your lender agreed that you would make monthly payments on your loan.

When will I receive my loan settlement statement?

You will receive your loan settlement statement at closing, when all parties involved in the sale are signing forms and making sure everything is in order.

Is there any downside to settling a loan early?

On the surface, paying off your loan before the terms agreed to seems like an obvious decision. If you're looking at a mortgage, it's likely that this is going to be the largest debt that you encounter in your lifetime, and the faster you settle your debt, the less interest you'll pay. Seems like a clear-cut decision, right?

What about a property settlement statement?

A property settlement statement is a third thing entirely: an agreement between divorcing spouses that divides their assets between both parties.

What does debt settlement mean?

Debt settlement means a creditor has agreed to accept less than the amount you owe as full payment. It also means collectors can’t continue to hound you for the money and you don’t have to worry that you could get sued over the debt. It sounds like a good deal, but debt settlement can be risky:

What happens if your credit score is shredded?

Your credit scores will have been shredded, you will feel hopelessly behind and your income won’t be enough to keep up with your debt obligations. Debt settlement companies negotiate with creditors to reduce what you owe, mostly on unsecured debt such as credit cards.

How long does a delinquent account stay on your credit report?

Delinquent accounts and debt charged off by lenders stay on your credit reports for seven years. Penalties and interest continue to accrue: You’ll likely be hit with late charges and penalty fees as well. Interest will keep racking up on your balance.

What are the two largest debt settlement companies?

There’s no guarantee of success: The two largest debt settlement companies are National Debt Relief and Freedom Debt Relief. Freedom Debt, for instance, says it has settled more than $8 billion in debt for more than 450,000 clients since 2002.

How does a settlement work?

Settlement offers work only if it seems you won’t pay at all, so you stop making payments on your debts. Instead, you open a savings account and put a monthly payment there. Once the settlement company believes the account has enough for a lump-sum offer, it negotiates on your behalf with the creditor to accept a smaller amount.

What to do if you don't want to use a debt settlement company?

If you don’t want to use a debt-settlement company, consider using a lawyer or doing it yourself.

What to do if you don't want to settle debt?

If you don’t want to use a debt-settlement company, consider using a lawyer or doing it yourself. A lawyer may bill by the hour, have a flat fee per creditor, or charge a percentage of debt or debt eliminated. Once you’re significantly behind, it usually doesn’t hurt to reach out to your creditors.

Student Loan Forgiveness For Some Navient Private Student Loans

The settlement agreement for Navient provides for $1.7 billion in private student loan cancellation. Here are the details:

Restitution For Some Federal Student Loan Borrowers

While no federal student loans are being forgiven or cancelled under the settlement agreement with Navient, many borrowers will receive a modest financial award called restitution. About 350,000 borrowers will be eligible for around $95 million in restitution, which comes out to around $260 to $270 per borrower. There are eligibility criteria:

Do Student Loan Borrowers Need To Do Anything To Get Relief Under the Navient Settlement?

The relief being provided under the Navient student loan settlement will be distributed automatically. Borrowers should be notified sometime this summer if they qualify.