A life settlement provider is a regulated “matchmaker” in the sale of a life insurance policy in a life settlement transaction. What does this mean? Insurance is regulated at the state level, not by the federal government. As a result, each state decides on its own insurance rules and regulations.

Who qualifies for a life settlement?

- You should be at least 70 years old (unless you have a serious or terminal illness) Most licensed life settlement providers require you to be at least 70 years old ...

- The face amount of your policy should be at least $100,000. ...

- Your policy type must be eligible. ...

How can a life settlement help me?

HOW CAN A LIFE SETTLEMENT HELP ME? Selling your policy can supplement your retirement income, free up cash that was being used to pay premiums, fund a long-term care policy, cover unexpected medical expenses or pay off debt. If you still need insurance, you can retain a portion of your coverage while eliminating your ongoing premium payments. ...

Are life settlements bad for insurance companies?

This is bad for you, the customer because it jeopardises the chances of your claims being honoured. So, when comparing life insurance companies, you should check the claim settlement ratio of each company. Companies which have a high ratio should be favoured because those companies are more likely to settle your life insurance claims than ...

How do I invest in life settlements?

To decide, consider the following:

- Life settlements typically are mid- to long-term investments.

- If the fund plans to frequently resell policies, rather than buying and holding them, the investments may be subject to fluctuations in investor demand, among other things.

- Capital is required to purchase the policy and pay the premiums while the policy is in force.

Is life settlement the same as life insurance?

A life settlement, or senior settlement, as they are sometimes called, involves selling an existing life insurance policy to a third party—a person or an entity other than the company that issued the policy—for more than the policy's cash surrender value, but less than the net death benefit.

What do life settlement companies do?

Life settlement companies purchase active life insurance policies from seniors, offering cash settlements to secure the death benefit rights to the policies. The companies become the beneficiaries of purchased life insurance policies and are responsible for paying the premiums required to keep the policies in force.

What is the primary purpose of a life settlement contract?

A life settlement refers to the sale of an existing insurance policy to a third party for a one-time cash payment. The policy's purchaser becomes its beneficiary and assumes payment of its premiums, and receives the death benefit when the insured dies.

How much do life settlement brokers make?

Life Settlement Broker Salary According to ZipRectuiter, the average salary is around $65,000 per year. For reference, that is about $31 per hour or $5300 per month, pre-tax. However, top earners can make over six figures, and even the 75th percentile are bringing home upwards of $75,000 annually, or $6000 per month.

Are life settlements safe?

Some clients who hear about the idea of a life settlement may ask you: Are life settlements safe and secure? The answer is yes: Life settlement transactions are among the safest and most secure financial transactions in both the insurance and financial services markets. One reason is regulation.

How much can you get from a life settlement?

It's typical for a life settlement to pay anywhere from 10% to 25% of the policy benefit amount. So if you were to sell a $200,000 policy you may get anywhere from $20,000 to $50,000 in cash. But there's a catch. Any money you receive from a life settlement would be subject to taxation at your ordinary income tax rate.

Who is the owner of a life settlement contract?

Owner The individual or entity that holds all rights to a life insurance policy. May also be called a “policy owner.” Provider A party entering into a life settlement contract with a policy owner and paying the policy owner when the life settlement transaction closes.

What happens when the owner of a life insurance policy dies?

Typically, the beneficiary or beneficiaries named in the policy will receive the payout. The money will go to the deceased's estate if no beneficiary is listed. It's important to note that life insurance policies are not subject to income tax, so beneficiaries typically receive 100% of the payout.

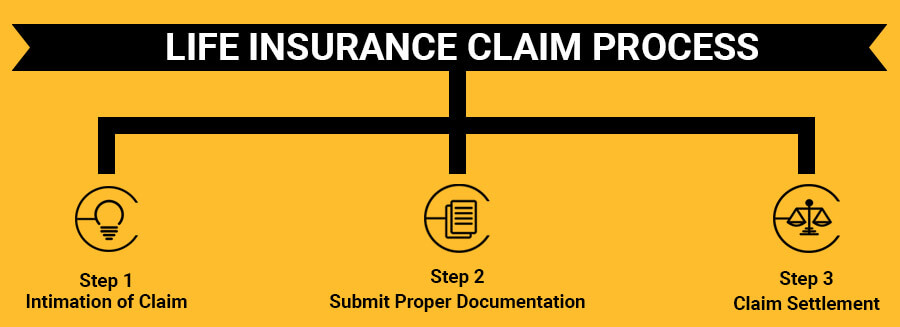

How do I get a life settlement?

The life settlement process starts with a policyholder presenting their policy to a provider, broker, or life settlement company to determine their eligibility. During this time, the third party will review medical records and policy information to see if the person qualifies for a life settlement.

Is a life settlement tax Free?

Is A Viatical Settlement Taxable? Most of the time, viatical settlements are not taxable. Settlement proceeds for terminally ill insureds are considered an advance of the life insurance benefit. Life insurance benefits are tax-free, and so it follows that the viatical settlement wouldn't be taxed, either.

What is the Commission on a life settlement?

Percentage of face valuecalculates the fee based on the insurance policy's face value. The face value is the policy's original death benefit, not including any loans outstanding. If a life settlement broker earns a commission of 6% against a face value of $200,000, the fee is $12,000.

Are life settlements taxable?

To recap: Sale proceeds up to the amount of the cost basis are not taxable. Sale proceeds above the cost basis and up to the policy's cash surrender value are taxed as ordinary income. Any remaining sale proceeds are taxed as long-term capital gains.

How are life settlements regulated?

Under the terms of California Insurance Code, sections 10113.1 through 10113.3, life settlement brokers and providers are required to obtain a license from the California Insurance Commissioner to transact life settlement business in California and are subject to both licensing and consumer disclosure requirements.

What is a life insurance settlement option?

Definition: Under a settlement option, the maturity amount entitled to a life insurance policyholder is paid in structured periodic installments (up to a certain stipulated period of time post maturity) instead of a 'lump-sum' payout.

Who is the owner of a life settlement contract?

Owner The individual or entity that holds all rights to a life insurance policy. May also be called a “policy owner.” Provider A party entering into a life settlement contract with a policy owner and paying the policy owner when the life settlement transaction closes.

Are life settlements taxable?

To recap: Sale proceeds up to the amount of the cost basis are not taxable. Sale proceeds above the cost basis and up to the policy's cash surrender value are taxed as ordinary income. Any remaining sale proceeds are taxed as long-term capital gains.

What Is a Life Settlement?

A life settlement refers to the sale of an existing insurance policy to a third party for a one-time cash payment. Payment is more than the surrender value but less than the actual death benefit. After the sale, the purchaser becomes the policy's beneficiary and assumes payment of its premiums. By doing so, they receive the death benefit when the insured dies.

How does a life insurance settlement work?

How Life Settlements Work. When an insured party can no longer afford their insurance policy, they can sell it for a certain amount of cash to an investor— usually an institutional investor. The cash payment is primarily tax-free for most policy owners. The insured person essentially transfers ownership of the policy to the investor.

What happens to a viatic settlement after the insured dies?

After the insured party dies, the new owner receives the death benefit. Viatical settlements are generally riskier because the investor basically speculates on the death of the insured. Even though the original policy owner may be ill, there's no way of knowing when they will actually die.

What happens when you sell a life insurance policy?

By selling it, the insured person transfers every aspect of the policy to the new owner. This means the investor who takes over the policy inherits and becomes responsible for everything related to the policy including premium payments along with the death benefit. So, once the insured party dies, the new owner—who becomes the beneficiary after the transfer—receives the payout.

Why do people sell life insurance?

There are many reasons why people choose to sell their life insurance policies and are usually only done when the insured person doesn't have a known life-threatening illness. The majority of people who sell their policies for a life settlement tend to be older people—those who need money for retirement but haven't been able to save up enough. That's why life settlements are often called senior settlements. By receiving a cash payout, the insured party can supplement their retirement income with a largely tax-free payout.

Why do people choose life settlements?

Other reasons for choosing a life settlement include: The inability to afford premiums.

What happens when you take a life settlement?

This is typical for people who no longer work for the company. By taking a life settlement, the company can cash out on a policy that was previously illiquid. Life settlements generally net the seller more than the policy's surrender value, but less than its death benefit.

What is life settlement?

A life settlement is the sale of a life insurance policy to an investor for cash. The amount received is more than the policy’s cash surrender value, but less than the death benefit. People often pursue life settlements when they need money to pay for retirement, long-term care, or other expenses.

What does a life insurance settlement provider decide?

The life settlement provider will decide whether or not they want to purchase your policy and what they are willing to pay. It is possible that during the review process, a settlement provider will determine that it doesn’t make sense to purchase your policy.

What is a traditional life settlement?

A traditional life settlement is the most common way to sell your life insurance policy. If you are over 65 years old and have a permanent life insurance policy (or a convertible term policy) that is worth over $100,000, you are potentially eligible for a traditional life settlement. Viatical Settlement.

What is retained death benefit?

A retained death benefit allows the policyholder to retain a portion of the death benefit after a life settlement. Since they are not selling the full policy, they receive a smaller settlement.

What is included in a life settlement closing package?

Some of the most common documents in a closing package include a letter of competency (LOC), verification of coverage (VOC), life settlement contract, life expectancy reports, change of ownership form (COO), and change of beneficiary form (COB).

What is LISA insurance?

LISA is an industry association that acts as a governing body for the most respected life insurance settlement companies in the marketplace.

What is the best way to sell a life insurance policy?

The most common life settlements options are traditional, viatical, and retained death benefit settlements. Traditional Life Settlement. A traditional life settlement is the most common way to sell your life insurance policy.

What is life settlement?

A life settlement occurs when you sell your existing life insurance policy to a third party for a one-time payment. Life settlements offer an alternative to cashing out your policy—a.k.a. getting the policy’s cash surrender value or cash value. After selling your policy, the buyer pays your premiums and receives the death benefit when you die. You may qualify for a life settlement if you are over 65 years old and have had your policy long enough to meet your state’s minimum. Typically, the death benefit of your policy must be at least $100,000.

What is the number one life insurance settlement provider?

Coventry earned the top spot on our list because of the company’s size and strong reputation. The company pioneered the life settlement industry by creating a secondary market for life insurance over 35 years ago. It’s the country’s biggest life settlement provider by a large margin—accounting for 40% of all transactions in 2020. Coventry was named the number-one life settlement provider in 2020 by The Deal. 2

How to start a life insurance settlement?

You can start the life settlement process by submitting a questionnaire, authorization, insurance carrier illustrations, and your past five years of medical records. The company does complete a background check to prevent fraud. Coventry also offers a retained death benefit, allowing you to keep part of your policy’s payout after you stop paying premiums.

Why do people give up life insurance?

As you get older, your life insurance policy only becomes more costly. It may even become unaffordable, so it's easy to see why so many people give up their policies. A 2019 study from the Society of Actuaries and LIMRA found that 4% of life insurance policies—worth billions of dollars—lapse every single year. 1 But if you need money, there is an alternative you may not have considered: life settlements.

How long does it take to sell Coventry insurance?

The sales process may take up to 30 days. Coventry also offers a retained death benefit, allowing you to keep part of your policy’s payout after you stop paying premiums. To qualify, you must be at least 65 years old or have a serious health condition with a life expectancy of less than 20 years.

How long does it take to get a life settlement from Abacus?

You may also accomplish the same thing by calling their team. The company completes a federal background check with the sales process taking 14 to 21 days.

What is death benefit?

Death benefit. This is the amount paid out to the beneficiary (in this case, the life settlement company) upon the death of the insured.

What is life settlement?

A life settlement is the legal sale of an existing life insurance policy (typically of seniors) for more than its cash surrender value, but less than its net death benefit to a third party investor. . The investor assumes the financial responsibility for ongoing premiums and receives the death benefit when the insured passes away. The primary reason the policy owner sells is because they can no longer afford the ongoing premiums, they no longer need or want the policy, or they need money for expenses.

Who do life settlement brokers represent?

Most providers represent multiple investors. Life settlement brokers represent the original policy owner on the sale of a life settlement contract. They shop the policy to life settlement providers (who then shop the policy to their investor network).

How many life insurance policies are there in 2020?

Life settlements remain a niche asset class. For the year ending 2020, according to the Life Settlement Report by the Deal, there were 3,241 policies purchased with a total face value of $4.6B on the secondary market (from the original policy owner). This was up from 2019 when 2,878 policies for a total face value of $4.4B were purchased on the secondary market. In contrast, as of 2018, there were 267M life insurance policies in force in the United States. Moreover, it is estimated that roughly 10M policies a year lapse. Since the policy owner would always be better off selling rather than lapsing, many believe the life settlement market has tremendous growth potential.

Why are life insurance settlements so rare?

Despite the Supreme Court ruling, life settlements remained extremely uncommon due to lack of awareness from policy holders and lack of interest from potential investors. That changed in the 1980s when the U.S. faced an AIDS epidemic. AIDS victims faced short life expectancies, high unanticipated expenses related to medical care, and selling a life insurance policy that they no longer needed as a way to pay these expenses made sense. However, by the mid-1990s, this investment strategy had faded away because of the rise of antiviral drugs .

How to increase awareness of life settlement options?

To increase market individuals' awareness of the life settlement option, providers are utilizing marketing and advertising strategies to reach them. By eliminating the intermediate financial advisors and other professionals hired to identify potential policy owners, the policy supply has increased and transaction costs paid by policy owners have decreased. This results in a greater return on investment for buyers.

What is the age limit for life insurance?

Most commonly, universal life insurance policies are sold. Policyholders are generally 65 or older and own a life insurance policy worth $100,000 or more.

Why are life settlements uncommon?

Despite the Supreme Court ruling, life settlements remained extremely uncommon due to lack of awareness from policy holders and lack of interest from potential investors. That changed in the 1980s when the U.S. faced an AIDS epidemic.

What are the two types of life settlement companies?

There are two main types of life settlement companies: providers and brokers.

What is life settlement payout?

Life settlement payouts are typically for an amount higher than your policy’s cash surrender value, but less than the net death benefit. Once the life settlement company secures ownership of your policy, they’re in charge of paying the premiums to keep the policy in effect.

How many companies buy life insurance?

There are more than 30 companies that buy life insurance policies and even more brokers who can help you find a buyer and navigate the process. There are unique advantages to working with companies, and there are unique advantages of working with a broker.

How to sell life insurance?

To sell your insurance policy, you need to contact a life settlement company. You’ll submit an application with the required paperwork, and the company will come back with an offer. If you accept that offer, you’ll receive a cash payout in exchange for ownership rights of your policy.

How long does it take for Genesis to settle?

Genesis has a lot of unique qualities that made them an obvious choice for our top 5 list. First off is speed. While many companies take 90-120 days to finalize a settlement, Genesis can put money in your pocket in half that amount of time.

Why do people pursue life insurance settlements?

People often pursue life settlements because they no longer need their life insurance policy and would rather have cash in their pocket.

Is life settlement growing?

The life settlement industry is growing every year, meaning there are more providers and brokers than ever before.

What is a settlement in a mortgage?

With regards to your language of “loan transaction,” in context, this is a process, called a “settlement,” or a “closing,” or “escrow,” that has procedures for executing legally binding documents relating to a lien on a property that is subject to a federally related mortgage loan.

What is a RESPA settlement?

RESPA provides quite a broad definition of a settlement service, starting with the meaning of a “Settlement Service.”. That is, whoever provides a settlement service is obviously a settlement service provider. With regards to your language of “loan transaction,” in context, this is a process, called a “settlement,” or a “closing,” or “escrow,” ...

Is a settlement service provider a provider?

Any provider of a settlement service is , mutatis mutandis, a settlement service provider. The following list is a guide, certainly not meant to be exclusive, that forms a basis for RESPA’s broad way of defining a settlement service. [24 CFR § 3500.2 (b)]