Any lump-sum settlement is considered a final payout from the insurance company. This means that your relationship with the insurance company is over. You will not receive additional money from the carrier and you will not be able to sue the insurance company.

Full Answer

What is a lump sum settlement from an insurance company?

Lump sum settlements may be offered by an insurance company to compensate workers for permanent injuries following a work-related accident. If a lump sum payment is accepted by the injured worker the insurance company may avoid paying on-going, monthly, cash settlements to the worker.

Can I take a lump sum settlement for long-term disability?

Typically, lump sum settlement offers are only for a portion, rather than the full value, of your future long-term disability benefits. If you accept such a settlement, you will not receive any further monthly benefits.

What is long-term disability insurance lump sum?

Long-term disability insurance protects a portion of your income in the event that a medical condition renders you unable to work. Once your LTD claim is approved, you will typically begin receiving monthly benefits. However, at some point, the insurance company may offer you a lump sum settlement in lieu of continued monthly benefits.

What makes an insurance company more likely to offer a settlement?

The nature of your disability: If the nature of your disability is such that your condition is not likely to improve, the insurance company may be more likely to offer you a settlement.

What is the highest deductible for flood insurance?

Policies with building coverage limits of $100,000 or less will have a fixed $1,000 deductible, and policies with building coverage limits over $100,000 will have a fixed $1,250 deductible....NFIP flood insurance deductibles.Building deductibleContents deductibleInitial discount$10,000$10,00040%5 more rows•Oct 15, 2021

Which flood insurance form provides only actual cash value coverage?

A Standard Flood Insurance Policy is a single-peril (flood) policy that pays for direct physical damage to your insured property up to the replacement cost or Actual Cash Value (ACV) (See “How Flood Damages Are Valued”) of the actual damages or the policy limit of liability, whichever is less.

Which of the following property items is not covered by flood insurance?

Anything that is outside the walls of your primary structure, except for a detached garage, is usually excluded from flood insurance. Trees, plants, wells, decks, patios, fences, pools, and hot tubs are typically not covered.

How will a flood policy respond if a flood is already in progress when the policy becomes effective?

The Standard Flood Insurance Policy (SFIP) excludes from coverage a loss caused by a flood that is already in progress at the time and date the policy is purchased.

What does substantially damaged mean?

The term “substantial damage” applies to a structure in a Special Flood Hazard Area – or floodplain – for which the total cost of repairs is 50 percent or more of the structure's market value before the disaster occurred, regardless of the cause of damage. This percentage rule can vary among jurisdictions.

Is the National Flood Insurance Program ending?

The NFIP is currently authorized until September 30, 2022. Unless reauthorized or amended by Congress, the following will occur on September 30, 2022: The authority to provide new flood insurance contracts will expire.

What is excluded on the flood insurance policy?

Coverage is now excluded for water, moisture, mildew, or mold damage caused by the policyholder's failure to inspect and maintain the insured property after the flood waters recede.

How much water is considered a flood?

A general and temporary condition of partial or complete inundation of 2 or more acres of normally dry land area or of 2 or more properties (at least 1 of which is the policyholder's property) from: Overflow of inland or tidal waters; or.

What is not considered a flood?

Notice that the NFIP policy covers the "unusual and rapid accumulation or runoff of surface waters ...." So, if there is no surface water, there is no coverage. Water that enters the home through the ground below the surface is not a covered flood if it also does not accumulate on the surface.

Which loss would not be covered by the National Flood Insurance Program?

According to the NFIP, the following kinds of damage are not covered by flood insurance: Damage caused by moisture, mildew, or mold that could have been avoided by the property owner or which is not attributable to the flood. Damage caused by earth movement, even if the earth movement is caused by flood.

Which of the following is not considered to be a flood under a flood policy?

A separate deductible applies to contents and building losses. Underground leakage is not considered a flood under the policy. Which Statement is true regarding a Difference In Conditions Policy?

What must a lender do if the borrower disputes that the property is in an SFHA?

Answer: If a borrower disputes a lender's determination that the building securing the loan is located in an SFHA requiring mandatory flood insurance coverage, the parties involved in making the determination are encouraged to resolve the flood zone discrepancy before contacting FEMA for a final determination.

Are NFIP policies replacement cost or actual cash value?

NFIP offers two types of coverage for homeowners: building property coverage up to $250,000 and contents coverage up to $100,000. A standard flood insurance policy pays for the replacement cost of your home or the actual cash value of damages, up to the policy limit.

Which three values are considered in the amount of flood insurance required by the FDPA?

NFIP, (2) the insurable value of the property, and (3) the principal loan amount(s) outstanding. The lesser of the three is the minimum required amount of coverage.

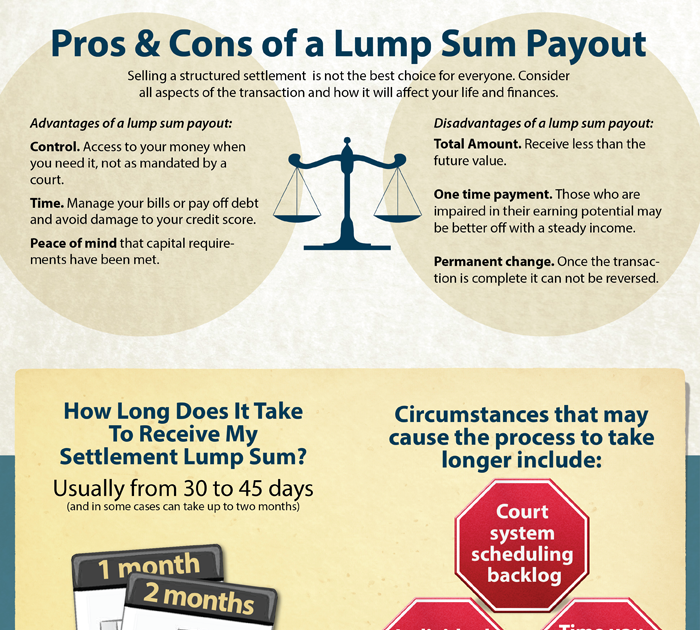

What does Lump Sum Settlement mean?

Lump sum settlements may be offered by an insurance company to compensate workers for permanent injuries following a work-related accident. If a lump sum payment is accepted by the injured worker the insurance company may avoid paying on-going, monthly, cash settlements to the worker. In some states the insurance company may also include payment for medical bills and no longer be responsible for the workers' medical expenses.

Can you settle a lump sum claim with a lawyer?

Prior to agreeing to a lump sum settlement, workers may want to seek legal help from a workers' compensation lawyer. The lump sum settlement should not be accepted until the injured worker is assured it includes adequate compensation for any disputed amounts, past-due temporary disability payments, and unreimbursed medical expenses.

Do you get a lump sum payout if you win a trial?

Additionally, if you do decide to proceed to trial in some state you are not able to receive a lump sum payout after you win at court, only weekly payouts. Another benefit, assuming you do not need medical care in the future, is you may receive money for future medical benefits that you will not have to use.

What is a Lump Sum Settlement Offer?

A lump sum settlement is when your insurance company offers to pay you your future long-term disability benefits in one lump sum now, rather than continuing to send you monthly benefits. Typically, lump sum settlement offers are only for a portion, rather than the full value, of your future long-term disability benefits. If you accept such a settlement, you will not receive any further monthly benefits. There are advantages and disadvantages to accepting a lump sum settlement offer, and while a sizable, immediate sum of money may seem tempting at first, it is important to fully evaluate your options before making your decision.

Why do insurance companies offer lump sum settlements?

Insurance companies typically offer lump sum settlements because they believe, in the long run, it will save them money compared to paying you monthly benefits for the duration of your disability. Not all claimants are offered lump sum settlements.

What is Chisholm and Kilpatrick?

Chisholm Chisholm & Kilpatrick LTD has a team of legal professionals with expertise in long-term disability and ERISA law. If you need guidance on how to handle a lump sum settlement offer with your insurance company, they are ready to assist you. Our attorneys know how insurance companies operate and are experienced with the ways they seek to save money by offering settlements. A member of our team can evaluate your claim and help you navigate this process if you have been offered a settlement.

What happens if you accept a lump sum settlement?

After you accept, you will no longer have to worry about dealing with them regarding payments, requests for updated records and documentation, or policy changes.

Can you get a lump sum settlement for long term disability?

The nature of your disability: If the nature of your disability is such that your condition is not likely to improve, the insurance company may be more likely to offer you a settlement. This is because you are likely to receive LTD benefits for the maximum benefit period, and thus the insurance company is almost guaranteed to pay you the full value of your future long-term disability benefits if you remain on claim. Because settlement offers are typically only for a portion of your future LTD benefits, an accepted lump sum settlement allows the insurance company to reduce the overall amount it must pay on your claim.

Can you invest in a lump sum settlement?

You can invest the lump sum settlement to grow your rate of return funds for the future. The lump-sum settlement becomes part of your estate and can be passed down in the event of your death, while your long-term disability benefits would simply end if you passed away while on claim.

Do all claimants get lump sum settlements?

Not all claimants are offered lump sum settlements. This is because insurance companies consider a number of factors when determining whether a one-time payment is more cost-effective for their business than continuing monthly payments. These factors include: