Impound is an account maintained by mortgage companies to collect amounts such as hazard insurance, property taxes, private mortgage insurance, and other required payments from the mortgage holders. ... A settlement statement is a document given to borrowers at closing that itemizes services and fees charged to the borrower by the lender or ...

What does impound mean in real estate?

By Investopedia Staff. Impound is an account maintained by mortgage companies to collect amounts such as hazard insurance, property taxes, private mortgage insurance and other required payments from the mortgage holders.

What is a settlement statement?

What is a settlement statement? A settlement statement is an itemized list of fees and credits summarizing the finances of an entire real estate transaction. It serves as a record showing how all the money has changed hands line by line.

What is the difference between escrow and impound?

What is an escrow or impound account? An escrow account, sometimes called an impound account depending on where you live, is set up by your mortgage lender to pay certain property-related expenses. The money that goes into the account comes from a portion of your monthly mortgage payment.

Do I need an impound account if I have low down payment?

Because low down-payment borrowers are considered high risk, the impound account assures the lender that the borrower will not lose the home because of liens or loss, as the lender pays insurance, taxes, etc., from the impound account when they are due. However, buyers don't need to maintain impound accounts forever.

What does impound mean in accounting?

What Does Impound Mean? Impound is an account maintained by mortgage companies to collect amounts such as hazard insurance, property taxes, private mortgage insurance, and other required payments from the mortgage holders. These payments are necessary to keep the home but are not technically part of the mortgage.

What happens to Prepaids?

As the name suggests, prepaids are upfront cash payments made before your down payment to obtain a mortgage. Prepaid costs are paid at closing and placed into an escrow account to cover mortgage expenses that are typically included in monthly homeownership-related fees.

What is your escrow balance?

Your escrow balance is the amount of money that is held for you in your escrow account (also called an impound account in some areas of the country). You pay into your escrow account each month as part of your regular mortgage payment. Not all lenders require an escrow account, though many do.

What are escrow Prepaids?

Prepaids are expenses or items that the homebuyer pays at closing before they are technically due. They are necessary to create—or "pre-fund"—an escrow account or to adjust the seller's existing escrow account. Prepaids can include taxes, hazard insurance, private mortgage insurance, and special assessments.

What is the difference between prepaid and escrow?

Prepaid items are one-time charges, paid at the time a real estate transaction is closed, or finalized. Escrow accounts are a continuing expense, typically billed monthly by the lender.

Why is homeowners insurance prepaid at closing?

Most of your monthly escrow payment goes toward your mortgage, but a portion of it gets set aside for your home insurance and taxes. That way, when your annual insurance premium is due, you've built up an amount of money to pay it. This is also how prepaid homeowners insurance at closing works.

Can you take money out of escrow?

Escrow accounts offer the benefit of security. No party may withdraw money from the account. One party makes payment into the account while another party receives payments form the account. Neither may withdraw money from the account at any time, meaning the money held in the escrow account is completely secure.

Should I pay off my escrow balance?

Both the principal and your escrow account are important. It's a good idea to pay money into your escrow account each month, but if you want to pay down your mortgage, you will need to pay extra money on your principal. The more you pay on the principal, the faster your loan will be paid off.

Will I get a refund from my escrow account?

Paid off mortgage completely: If you have a remaining balance in your escrow account after you pay off your mortgage, you will be eligible for an escrow refund of the remaining balance. Servicers should return the remaining balance of your escrow account within 20 days after you pay off your mortgage in full.

Is escrow an expense?

Escrow Expenses means those expenses in respect of real and personal property taxes and assessments, Insurance Premiums and such other Impositions as the Lender pays from time to time directly from the Escrow Fund using monies accumulated through the collection of Monthly Escrow Payments. Escrow Expenses .

What is escrow example?

Example of Escrow In return, the seller takes the property off the market and finalizes repairs, etc. All goes well and at the time of the purchase the escrow money is transferred to the seller and the purchase price is reduced by $5,000.

What are escrow items?

Prepaid Items or Escrows Prepaids are expenses that you will pay at closing before they technically come due. You might be required by your lender to pay monthly or annually in advance for taxes, hazard insurance, private mortgage insurance, or special assessments.

Can Prepaids be rolled into loan?

Costs known as prepaids must be paid upfront and may not be rolled in. Often, this is because prepaid costs must go into an escrow account.

How is prepaid income treated?

Accounting for Prepaid Income Prepaid income is considered a liability, since the seller has not yet delivered, and so it appears on the balance sheet of the seller as a current liability. Once the goods or services have been delivered, the liability is cancelled and the funds are instead recorded as revenue.

Where do prepayments go in the balance sheet?

Where Do Prepaid Expenses Appear on the Balance Sheet? Prepaid expenses are first recorded in the prepaid asset account on the balance sheet as a current asset (unless the prepaid expense will not be incurred within 12 months).

Where do prepaid assets go on a balance sheet?

Prepaid expenses represent future expenses paid in advance — so, until the associated benefits are realized, the expense remains a current asset. The prepaid expense is listed within the current assets section of the balance sheet until full consumption (i.e. the realization of benefits by the customer).

What does an impound account do at closing?

At closing the buyer sets up an impound account that allows them to bundle the cost of their mortgage principal, taxes, mortgage insurance, and other monthly costs into one payment. The lender likes this because they can make sure the new owner will keep up to date with all the payments associated with the home.

What is a settlement statement?

A settlement statement is an itemized list of fees and credits summarizing the finances of an entire real estate transaction. It serves as a record showing how all the money has changed hands line by line.

Is a settlement statement the same as a closing statement?

Yes, a settlement statement is the same as a closing statement, though “settlement” is the formal term most likely to be used by the real estate industry.

What is an ‘excess deposit’ at closing?

A particular line item that causes confusion on the seller’s settlement statement is the “Excess Deposit.” What is an excess deposit, and who will receive the funds listed on that line?

What information is needed to complete a closing document?

At the top of the document (before you get to the portion that looks like a spreadsheet) you’ll see a few boxes for inputting information that records basic details about the transaction, such as the names of the buyer and seller, the property address, and the closing date.

When are property taxes prorated?

For instance, say you get billed for property taxes in February to cover the previous year. If you’re closing on a sale on April 30, the yearly property tax is “prorated” or calculated for the first four months of the year, and it’s reflected in this section.

Who is responsible for preparing the settlement statement?

Whoever is facilitating the closing — whether it be a title company, escrow firm, or real estate attorney — will be responsible for preparing the settlement statement.

What happens if you don't pay property taxes?

If you fail to pay your property taxes, your state or local government may impose fines and penalties or place a tax lien on your home. You could also face foreclosure. In addition, if you fail to pay your taxes or insurance, your lender may: Add the amounts to your loan balance. Add an escrow account to your loan.

Is force placed insurance more expensive than home insurance?

This lender-purchased insurance, known as force-placed insurance, is typically more expensive than homeowners insurance you pay on your own. Even if your lender does not require an escrow account, consider requesting one voluntarily.

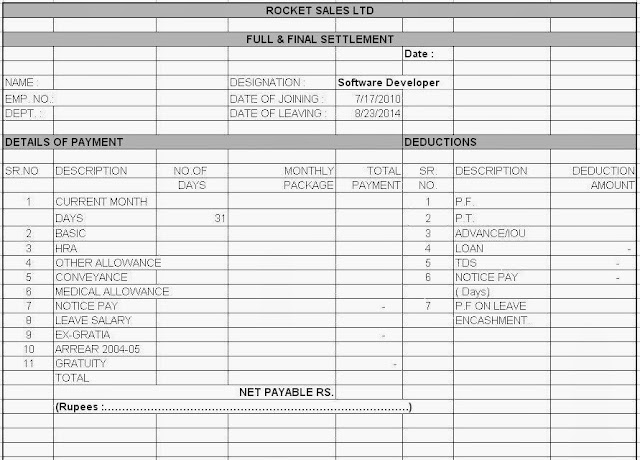

What Is a Settlement Statement?

A settlement statement is a document that summarizes the terms and conditions of a settlement, most commonly a loan agreement. A loan settlement statement provides full disclosure of a loan’s terms, but most importantly it details all of the fees and charges that a borrower must pay extraneously from a loan’s interest. Different types of loans can have varying requirements for settlement statement documentation. Generally, loan settlement statements can also be referred to as closing statements .

What is insurance settlement?

Insurance settlement: An insurance settlement is most commonly documentation of the amount an insurer agrees to pay after reviewing an insurance claim. Banking: In the banking industry, settlement statements are produced on a regular basis for internal banking operations.

What is a RESPA?

The Real Estate Settlement Procedures Act (RESPA) govern s the formulation of both closing disclosures and HUD-1 statements for the mortgage lending market. RESPA has been revised and updated throughout history to help manage mortgage lending disclosures and protect borrowers. RESPA requires a HUD-1 settlement statement for borrowers involved in a reverse mortgage. For all other types of mortgage loans, RESPA requires the mortgage closing disclosure.

What is included in HUD-1?

These forms also include comprehensive information about the borrower’s loan, detailing the principal and interest as well as all of the upfront costs, commission charges, service costs, and any deductions associated with the loan. Loan terms are also included, such as details on principal, interest, variable rates, prepayment penalties, and any special clauses associated with a loan such as escrow requirements.

What is debt settlement?

Debt settlement: A debt settlement statement can provide a summary of debts written off, reduced, or otherwise amended after a debt settlement has completed. Lawyers and debt settlement companies work on behalf of borrowers with overwhelming amounts of debt, in order to help them reduce some or all of their obligations.

What is a settlement statement in stock trading?

Trading: In financial market trading, settlement statements provide proof of a security’s ownership transfer. Typically, stocks are transferred with a T+2 settlement date meaning ownership is achieved two days after the transaction is made.

When are settlement statements created?

Beyond just loans, settlement statements can also be created whenever a large settlement has taken place, such as with a large business transaction or potentially in the legal, insurance, banking, and trading industries.

What is a Settlement Statement?

The settlement statement, also known as the closing statement, is a legal document that outlines what a buyer needs to pay to the seller or vendor on settlement. The statement also has a good faith estimate. The settlement statement lists all charges and credits to both the buyer and the seller in a property or real estate settlement.

Meet some of our Real Estate Lawyers

Possesses extensive experience in the areas of civil and transactional law, as well as commercial litigation and have been in practice since 1998. I addition I have done numerous blue sky and SEC exempt stock sales, mergers, conversions from corporations to limited liability company, and asset purchases.

How long does it take to pay insurance on an impound?

INSURANCE: The lender requires that one full year of insurance be paid in advance and through the escrow during the time the account is set up. The lender will also collect an additional 2-3 months upfront for the Impound Account, as the next premium will not become due until 12 months from the close of the escrow.

What is estimated settlement statement?

At the time of signing loan documents, the buyer is presented with an estimated settlement statement by their escrow holder. This statement includes the initial amount the lender will collect in order to establish the Impound Account. This amount often brings up questions from the buyer, as it sometimes appears that they are paying for months of taxes before they are the owner of the property. In this blog, we explain how a lender calculates the initial amount they request from the buyer through the close of escrow.

How much upfront do you have to collect from a buyer for a mortgage?

As the lender would have received at least six monthly mortgage payments, including monthly impound amounts, from the buyer at this time, then the lender would only need to collect 2 to 3 months upfront from the buyer through the escrow.

How is yearly property insurance determined in California?

The yearly insurance premium is determined by the buyer’s insurance agent and provided to the lender as a condition of the loan. TAXES: Property Taxes in California are billed once a year and are payable in two parts. The Tax bills are sent out by October each year.

How much money does a lender need to collect from the buyer?

The lender usually requires an amount equal to a two months reserves to remain in the Impound Account at all times for both property taxes and insurance. Depending on how many monthly mortgage payments the buyer would have made at the time the bill will be due, will determine how many months the lender would need to collect upfront from the buyer.

What is an impound?

Impounds are nothing but a consolidated bundle of charges incurred to process the mortgage.

What is the disbursement date?

Disbursement Date. The day when the seller is supposed to receive the payment in their bank account. The disbursement date is the same as the settlement date in most cases. Other Dates: Dates given for recording or anything that relates to transferring the title of the property.

How many sections are there in an ALTA settlement statement?

There are a total of 11 sections in the ALTA settlement statement. Each of them highlights a particular type of cost associated with closing. Note that the debit and credit sections are listed against the seller and buyer on their respective sides from the second section which is where the costs are highlighted. Let’s go through all the sections.

What are points in a mortgage?

Points. Mortgage points are given to the lender for which they reduce the interest rate for the buyers. This amount is paid upfront during closing.

What does escrow charge?

The escrow or title company charges buyers for settlement charges and escrow costs. These costs are debited from the buyer’s side.

What is flood determination fee?

Flood Determination Fee to. It is paid to get government approval on the property and that it is not located in an area prone to flooding.

Where are miscellaneous costs debited?

Miscellaneous costs are debited from the buyer’s account most of the time. However, a lot of time the sellers may agree to pay apart as well, and the costs are debited from the seller’s side. Here is the list of all miscellaneous costs. Pest Inspection Fee.

What information is provided on a HUD-1 Settlement Statement?

Aside from the basic details of the involved parties, consisting of the buyer and seller , the lender , property details and settlement agent details, unsurprisingly the majority of the settlement statement consists of figures. Lots of figures.

What is HUD-1 form?

The HUD-1 form, often also referred to as a “ Settlement Statement ”, a “ Closing Statement ”, “ Settlement Sheet ”, combination of the terms or even just “ HUD ” is a document used when a borrower is lent funds to purchase real estate. Another acronym used in relation to the HUD form is GFE, which means ‘ Good Faith Estimate ’.

What are the bank charges/escrows?

Bank Charges are fees paid to the bank for processing the loan. These fees are typically an origination fee or a processing fee which may be a fixed rate or based upon a % of the loan, (ie 1%) range from Credit reports, or fees that the bank expends while trying to get the loan approved. Examples are Appraisal fees, credit report fees, flood certification fees, etc.Bank Escrows are different from fees. Bank escrows are money that the bank wants on reserves that will be used to pay your upcoming bills for the home. These escrows are usually for property taxes, school taxes, county taxes and home owners insurance. They can range from one month to 4 months depending upon the date of the closing.

What is title insurance?

A title insurance policy is a mandatory insurance policy taken out when you are taking out a mortgage. The philosophy behind it is that there are issues that can arise relating to the title ownership of the land. Be it, problems with the past deeds, i.e. missing signatures or invalid information or more extreme issues like the detection of fraud relating to the title ownership of land. The title insurance is there to protect you up to the value of the policy when something does go wrong. And bear in mind, since humans are involved – things do go wrong.

What is a RESPA?

Another term linked with the HUD is RESPA. RESPA is an acronym for Real Estate Settlement Procedures Act and represents a set of legislative statutes relating to real estate transactions put in place by the government to enforce disclosure of charges and fees to the consumer.

What is HUD 1?

HUD is an acronym for Housing and Urban Development, and represents the arm of the U.S. government department responsible for legislation relating to home ownership and property development within the United States of America. The HUD-1 form, often also referred to as a “ Settlement Statement ”, a “ Closing Statement ”, “ Settlement Sheet ”, ...

What is an adjustment for items paid in advance?

Adjustments for items paid in advance by the seller primarily calculated from taxes paid. Amounts paid for by or in behalf of the borrow, and reductions in the amount due to the seller. Adjustments for items unpaid by the seller. Cash at settlement due from or to the buyer and seller.

What is an impound at closing?

Impounds are expenses that the buyer pays at closing before they’re due , such as:

What Information Does the ALTA Settlement Statement Contain?

The charges listed in the ALTA Settlement Statement are broken down into ten different categories, including:

What is the ALTA Settlement Statement?

The ALTA Settlement Statement is a form that itemizes all of the credits and costs associated with a real estate transaction. There are four different versions of this form, including:

What is excess deposit?

Excess Deposit—any money in escrow over the amount the buyer and seller agreed to pay

Why do buyers and sellers get different versions of closing disclosure forms?

This is partly because the Closing Disclosure contains personal information like your social security number you may not want others to know.

What is personal property?

Personal Property—the amount of money the buyer is paying to buy personal items like furniture from the seller. Existing Loans Assumed or Taken Subject To—only relevant if the buyer is taking over the seller’s mortgage. Excess Deposit—any money in escrow over the amount the buyer and seller agreed to pay.

Do points appear in a debit?

Sometimes a seller agrees to pay for the buyer’s points, so they may appear in the seller’s column as a debit.