Debt consolidation and debt settlement are strategies consumers use to get out of debt. The main difference between the two is debt consolidation incorporates the debt into one fixed monthly payment. In contrast, debt settlement only takes care of the highest interest rate and leaves the rest of the debt intact.

Full Answer

Is a debt consolidation loan good or bad?

Debt consolidation loan is an effective way to get out of debt. However, it is only a good idea to use it if you have the right debt and financial situation. Before you choose any of the debt relief options available, you have to understand your financial position first.

Should you do debt consolidation, bankruptcy or settlement?

If you’ve exhausted all other options trying to pay off your debts, your last resort may be to either settle your debt or file for bankruptcy. These options should only be considered if you’ve tried everything else and cannot pay down or eliminate your debt.

Is debt relief and debt settlement the same thing?

NOTE: To avoid confusion, a debt relief company and a debt settlement company are the same thing. The general concept with debt settlement is you negotiate a mutually acceptable settlement amount (for less than full balance) with a creditor or collection agency to resolve an outstanding balance.

Which is better, debt consolidation or debt management?

“A debt consolidation loan may be a better option for someone with a high credit score and a modest amount of debt,” McClary said. “Debt management plans are most appropriate for those who are in danger of falling behind on their creditor payments due to debt balances that have grown beyond the point where they are under control.”

Is debt settlement and debt consolidation the same thing?

Key Takeaways. Debt consolidation and debt settlement help you reduce your debt load, but they do so in different ways and by using different strategies. Debt settlement is helpful in cutting your total debt owed, while debt consolidation is useful for cutting the total number of creditors that you owe.

Is it better to pay a debt in full or settle?

It is always better to pay off your debt in full if possible. While settling an account won't damage your credit as much as not paying at all, a status of "settled" on your credit report is still considered negative.

What is the downside to consolidating debt?

You may pay a higher rate Your debt consolidation loan could come at a higher rate than what you currently pay on your debts. This could happen for a variety of reasons, including your current credit score. “Consumers consolidating debt get an interest rate based on their credit rating.

What is a difference between debt settlement and debt management plans?

Debt management programs (DMPs) are administered by nonprofit credit counseling companies, as opposed to debt settlement companies, which are for-profit. In a DMP, the credit counseling company negotiates with your creditors to reduce your interest rates and fees, or lower monthly payments for you.

How long does it take to improve credit score after debt settlement?

between 6 and 24 monthsHowever, a debt settlement does not mean that your life needs to stop. You can begin rebuilding your credit score little by little. Your credit score will usually take between 6 and 24 months to improve. It depends on how poor your credit score is after debt settlement.

How Much Does debt settlement hurt your credit?

Does Debt Settlement Hurt Your Credit? Debt settlement affects your credit for up to 7 years, lowering your credit score by as much as 100 points initially and then having less of an effect as time goes on. The events that typically lead up to debt settlement will affect your credit score, too.

Why you should never consolidate debt?

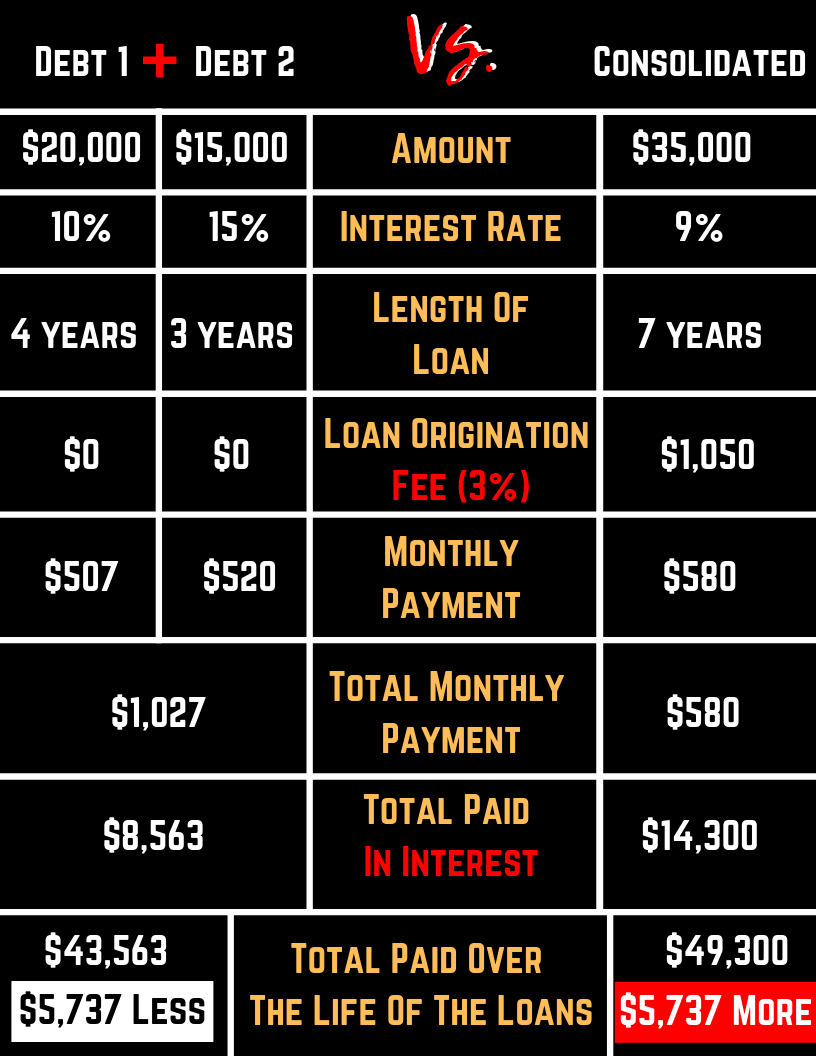

Debt consolidation is a bad idea if it does not save you any money. This happens when the interest rate on your new loan or line of credit ends up being higher than that of your existing debts, which mostly defeats the purpose of consolidation. In that case, the only benefit would be having all your debts in one place.

How long does debt consolidation stay on your record?

Debt settlement can cause your credit score to fall by more than 100 points, and it stays on your credit report for seven years. If your creditors close accounts as part of the settlement process, this can cause your credit utilization to increase, which also negatively affects your credit score.

Can I still use my credit card after debt consolidation?

Yes, although it depends on your situation. If you have good credit and a limited amount of debt, you probably won't need to close your existing accounts. You can use a balance transfer or even a debt consolidation loan without this restriction.

What is the meaning of a debt settlement?

Debt settlement is an agreement between a lender and a borrower to pay back a portion of a loan balance, while the remainder of the debt is forgiven. You may need a significant amount of cash at one time to settle your debt. Be careful of debt professionals who claim to be able to negotiate a better deal than you.

What is the debt settlement program?

Debt settlement companies, also sometimes called "debt relief" or "debt adjusting" companies, often claim they can negotiate with your creditors to reduce the amount you owe.

What are the disadvantages of a debt management plan?

Disadvantages of debt management plans your debts must be repaid in full – they will not be written off. creditors don't have to enter into a debt management plan and may still contact you asking for immediate repayment. mortgages and other 'secured' debts are not covered by a debt management plan.

Does paid in full increase credit score?

Some credit scoring models exclude collection accounts once they are paid in full, so you could experience a credit score increase as soon as the collection is reported as paid. Most lenders view a collection account that has been paid in full as more favorable than an unpaid collection account.

Does Paid in Full hurt your credit?

"Paid in full will have a positive effect on your credit score, and even more so if all payments were made on time," Castleman said. That's because out of all the factors that are used to calculate your credit score, payment history is the most heavily weighted at 35% of the total score.

Will a paid in full collection help my credit score?

When you pay or settle a collection and it is updated to reflect the zero balance on your credit reports, your FICO® 9 and VantageScore 3.0 and 4.0 scores may improve. However, because older scoring models do not ignore paid collections, scores generated by these older models will not improve.

What is the difference between paid in full and settled in full?

Paying in full means paying the total amount of your debt. Settling in full means coming to an agreement with your creditor or collection agency on an updated payment plan. While this may seem simple, there are nuances to how lenders look at the two on your credit report.

How does debt consolidation work?

Debt consolidation works by combining your existing debts into one new debt, ideally at a lower interest rate. For example, let’s say you owe $2,50...

What is a consumer credit counseling service?

Consumer credit counseling organizations are generally nonprofit organizations offering certified and trained counselors. These counselors can help...

Can I negotiate a debt settlement on my own?

The first step of the DIY debt settlement negotiation process is to dig into your debts to assess how much you owe and whether it’s possible to pay...

How does debt settlement affect my credit score?

Debt settlement can be harmful to your credit score because the process requires you to stop paying your bills and go delinquent on your debts. Alo...

What is debt consolidation?

Debt consolidation is a form of debt relief that combines multiple debts into one new consolidated debt. Instead of owing money to multiple creditors and having multiple monthly payments, debt consolidation lets you reorganize those debts into a single combined total. A couple of the most common ways to consolidate debt include 0% balance transfer credit cards and debt consolidation loans, or personal loans, from a bank or credit union.

What is debt settlement?

Debt settlement is an option that you can manage on your own if you are comfortable talking with your creditors and asking to make a deal on your debts.

How to get a better deal on debt settlement?

Instead of hiring a debt settlement company, you’ll often get a better deal for your overall financial situation by working with a consumer credit counseling agency. Instead of going delinquent on your debts and potentially taking a hit on your credit score, consumer credit counseling can help you stay current on your bills and pay off debt without the potential risks and longer-term consequences of debt settlement.

How does consumer credit counseling work?

If you sign up for this type of program, the consumer credit counseling service will work with your creditors and attempt to reduce your interest rate and fees.

How does debt management work?

With a debt management plan, you generally make one monthly payment to the consumer credit counseling agency, which then forwards payment to your creditors. They do not renegotiate the total amount of debt, but they help you make a plan to pay off your debt, while potentially helping reduce fees and costs.

What is credit counseling?

Some credit counseling organizations will help you create and implement a debt management plan for your debts. With this type of plan, you still pay the total amount of principal you owed. You make a single payment to the organization each month and the organization makes a payment to your creditors.

How long does it take to settle a debt?

And keep in mind that the debt settlement process can take two to four years, depending on the overall amount of your debt and the complexity of your situation.

What is the difference between debt settlement and debt consolidation?

Debt settlement is helpful in cutting your total debt owed, while debt consolidation is useful for cutting the total number of creditors that you owe. With debt consolidation, multiple loans are all rolled into a new consolidation loan that has one monthly interest rate.

What is secured debt consolidation?

Secured debt consolidation loans require you to use one or more assets as collateral, such as your home, car, retirement account, or insurance policy. For example, if you take out a home equity loan to consolidate debt, then your home would secure the loan.

What Is Debt Settlement?

While debt consolidation allows you to combine multiple debts into a single loan, debt settlement utilizes a very different strategy, When you settle debt, you’re effectively asking one or more of your creditors to accept less than what’s owed on your account. If you and your creditor (s) reach an agreement, then you would pay the settlement amount in a lump sum or a series of installments.

What is consolidation loan?

This is a single loan that rolls all of your prior debts into one monthly payment at one interest rate. Consolidation loans are offered through financial institutions —including banks, credit unions, and online lenders—and all of your debt payments are made to the new lender going forward.

Why is debt settlement important?

Debt settlement is helpful in cutting your total debt owed, while debt consolida tion is useful for cutting the total number of creditors that you owe.

What is the advantage of debt settlement?

The advantage of debt settlement is that you can eliminate debts without having to pay the balance in full. This may be an attractive alternative to bankruptcy if you’re considering a Chapter 7 filing as a last resort when in dire financial straits.

How to get a settlement if you are behind on a debt?

If you’re behind on one or more debts, then you would begin by reaching out to your creditor to ask if they’re open to negotiating a settlement. You can do this over the phone, but if you prefer to have a paper trail, then you can send a written request.

What is debt consolidation?

In debt consolidation, several consumer debts are rolled into a single new one. You can use a balance-transfer credit card, debt consolidation loan, home-equity loan or 401 (k) loan.

Why is debt settlement risky?

Debt settlement is risky because you withhold payments from a creditor and then, once your account is severely delinquent, try to negotiate a smaller payment to satisfy the debt.

What to do if you have unsuccessfully tried debt management?

If you’ve unsuccessfully tried a debt management plan, you might explore debt settlement companies. But proceed with caution. This is the riskiest debt-relief option.

Can you settle debt on your own?

You can try debt settlement on your own or hire a company, but beware: This field is rife with shady players. The Federal Trade Commission recently ordered 11 such companies to halt their marketing, saying they took tens of millions of dollars from consumers and gave them little benefit.

What is debt consolidation?

Debt consolidation is a way to combine one or more debts and pay them off with a single monthly payment, ideally with more favorable terms. A debt settlement, on the other hand, is a way to renegotiate the terms of what you owe so a creditor is willing to accept less than what is owed.

How to consolidate debt?

Here are common ways to consolidate debt: Home equity loanor home equity line of credit (HELOC):With a home equity loan, you can cash in on the equity in your home to pay off other debts, often at a lower (and fixed) interest rate than you’d get with credit cards or a personal loan.

How does debt consolidation help your credit score?

Debt consolidation can streamline your finances by taking the confusion out of juggling multiple creditors and payments, various due dates and different terms. Plus, you can potentially shorten your repayment period and improve your credit score while repaying debt.

What are the two ways to pay off debt?

Learn about two popular debt payoff strategies: debt consolidation and debt settlement. See if either option is right for you, and how to pursue them.

What is debt settlement?

Debt settlement is a type of debt relief in which you either negotiate on your own to settle debtwith your creditors – or work with a for-profit company that will attempt to do the same on your behalf. The goal is to get creditors to agree to settle accounts for less than what is due, on the grounds that some payment is better than no payment at all.

How does debt settlement work?

How debt settlement works. Debt settlement is a type of debt relief in which you either negotiate on your own to settle debtwith your creditors – or work with a for-profit company that will attempt to do the same on your behalf.

How much is debt settlement fee?

Fees are typically high. Debt settlement fees are typically 18% to 25% of the total debt enrolled in the program, but companies can also charge you a portion of that fee for debt that’s been settled.

How does debt settlement work?

Additionally, you will pay less than what you really owe. While consolidation pays off your debts in a full lump sum payment, settlement means negotiating with your creditors to lower the amount you owe them. You can do this by negotiating a settlement agreement with your creditor on your own or working with a debt settlement company.

What does "consolidate" mean?

Let’s start with the definition of “consolidate.” According to Merriam-Webster, “to consolidate” means “to join together into one whole.” So, how does this apply to your debts? Debt consolidation works by combining all of your debts together to make them easier to pay off. This means you’re only dealing with one payment and one interest rate instead of multiple monthly bills and varying rates and fees. There are a few main ways to do this:

How long does debt settlement stay on credit report?

When you start debt settlement, you will likely see your credit scores drop. After you settle your debt, it will usually remain on your credit report for up to 7 years .

What is a lump sum loan?

This is a type of personal loan to pay off all of your debt in a lump sum payment. Then the only interest rate you have to worry about is on the loan. No more individual interest rates and bills – you will only have one monthly payment.

Is debt settlement better than consolidation?

The answer to this question depends on your amount of debt and your ability to make the monthly payments. If you are going through a financial hardship that makes it impossible to pay off your high level of debt, then debt settlement may be the right option for you. If you think you can afford to pay off all of your debt and make the monthly payments, consolidation could be better for you. It really all depends on the specifics of your financial situation and if you want to save money. Give us a call to get connected to the debt relief service that fits you best.

Do credit card addicts have zero debt?

In more than 20 years as a financial adviser, educator, and author, I’ve seen literally thousands of former credit cards addicts emerge from their DMPs with not only zero debt, but zero addiction. Some get new credit cards and use them responsibly. Some find no need for them any longer.

Is there a catch to employing a debt consolidation firm?

Of course, Peter, there are also “catches” to employing a debt consolidation firm.

Debt Settlement

Debt settlement is a strategy where you reach an agreement with your creditors to pay less than the amount you owe. This is usually done when you have cash on hand and can pay off your debt with a lump sum or are able to save for a lump sum payment while ceasing payments to your creditors.

Debt Consolidation

Debt consolidation, on the other hand, is a process where you roll multiple debts into one. Through a consolidated loan or a nonprofit debt management program. We’ll review both types of debt consolidation programs.

Pros and Cons of Debt Settlement

Pay a reduced amount: One advantage of debt settlement is that you get to pay an amount that’s lower than your original debt, provided your creditor agrees to your offer.

Pros and Cons of Debt Consolidation

Simplified process: Instead of making multiple separate payments, debt consolidation allows you to pay for all your bills to one lender. You have one monthly deadline instead of having many that you must keep track of separately. Also, with nonprofit debt consolidation programs you can still consolidate your debt, even if you have bad credit.

Which Debt Repayment Strategy Is Right for You?

As with any financial strategy or debt repayment program, you need to first take stock of your overall financial standing before choosing one approach over the other.

What is the difference between debt consolidation and debt settlement?

The biggest difference between debt settlement and consolidation is how you pay off your debt. In debt settlement, you negotiate with your creditors, offering to pay less than what you owe. For instance, say you owe $10,000 to one of your credit card providers. You and your creditor might agree on a $7,000 payment.

How does debt consolidation work?

In this payoff strategy, you may work with a debt consolidation lender to gather all your debts into one single loan, with interest. You then make a payment that you can afford each month until you pay off all that you owe.

What to do if your debt is soaring?

But there is hope for getting back on track! If your financial debt is soaring, you can turn to debt settlement or debt consolidation to help boost your financial health and cut down on the amount you owe to creditors.

What is the benefit of debt settlement?

The obvious benefit of debt settlement is that your creditors might forgive a portion of your debt. If you owe a lender $14,000 and you only have to pay $8,000 to make that entire debt disappear, that can sound like a good deal.

How much does a debt settlement company charge?

Debt settlement companies charge varying fees, but you can expect to pay 15% – 20% of your total debt. If you owe $20,000, you can expect your debt settlement provider to charge you $3,000 – $4,000. The Federal Trade Commission warns that you should only work with debt settlement companies that list their fees in writing. And you should never work with one that charges its fees before it settles debt for you, the FTC says.

What happens if you stop paying on a debt settlement?

If a debt settlement company asks you to stop making payments on your loan until your account becomes delinquent and they make an offer to your creditors, you run the risk of not only being rejected by the creditors, but also accruing a hefty amount of interest and late fees as well as driving your credit score so low that it could take years for you to rebuild it enough to be approved for future lines of credit.

How long do missed payments stay on credit report?

A single missed payment can send your credit score falling by 100 points or more, and these missed payments remain on your three credit reports for 7 years. If you miss several payments while your debt settlement company negotiates on your behalf, your score can take a serious dive.