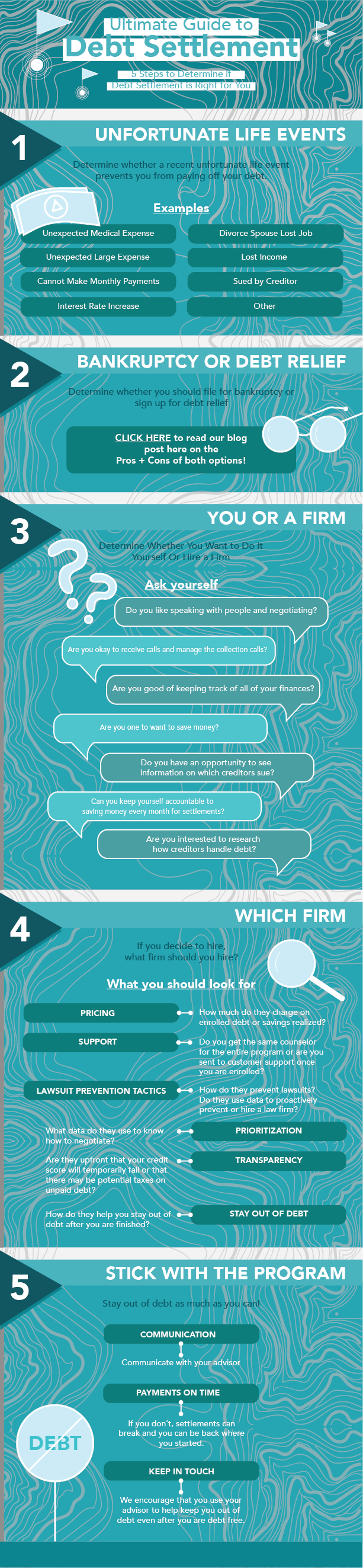

What is a Debt Settlement Plan?

- There are 5 main options:

- Debt Settlement Plans (DSPs) A DSP is the only type of debt-relief program, outside of bankruptcy, that can reduce or eliminate a substantial amount of your debt without making payment ...

- No Upfront Costs. ...

- Recent Debt Settlement Industry Results. ...

What is the best way to settle debt?

Part 1 of 3: Negotiating the Debt Amount Download Article

- Read the judgment. Debtors and creditors should review the court order (judgment) to determine the total amount due and any specific payment instructions ordered by the court.

- Evaluate your financial situation. Whether you are the creditor or the debtor, you should review your finances before negotiating the amount of the debt.

- Contact the other party. ...

Is debt settlement necessarily a bad thing?

While there can be consequences to debt settlement, it is not always a bad thing, and sometimes it might be your best option. If you are drowning in debt, settlement can relieve your burden and help you get on with your life. Even when debt settlement is a net positive, however, there are long-term consequences. In ...

What are the tips for debt settlement?

Tips On IRS Debt Settlement

- Look for an Offer in Compromise This is the most common solution that is found when it comes to IRS debt settlement. ...

- Look at All of Your Options Don’t think you are going to have one or two options in a situation such as this. ...

- Speak to a Professional

Is a debt settlement worth it?

The short answer: Yes, debt settlement is worth it if all of your debt is with a single creditor, and you’re able to offer a lump sum of money to settle your debt. If you’re carrying a high credit card balance or a lot of debt, a settlement offer may be the right option for you. There are numerous debt settlement and credit card companies that promise to help you settle your debt for half or even a small fraction of the total balance you owe, but is debt settlement really a good idea?

Is it a good idea to settle debt?

In general, paying off the total amount of debt you owe is a better option for your credit. An account that appears as "paid in full" on your credit report shows potential lenders that you have fulfilled your obligations as agreed, and that you paid the creditor the full amount due.

What is a debt settlement fee?

Debt settlement companies typically charge a 15% to 25% fee to tackle your debt; this could be a percentage of the original amount of your debt or a percentage of the amount you've agreed to pay.

What happens after a debt settlement?

Once you've started the debt settlement process, you're typically advised to halt payments with your creditors. Instead, you should pay into the dedicated account set up by the debt settlement company until that account has reached the agreed amount for the lump sum payment.

What do debt settlement companies do?

Debt settlement companies are companies that say they can renegotiate, settle, or in some way change the terms of a person's debt to a creditor or debt collector.

Is it better to settle or pay in full?

Generally speaking, having a debt listed as paid in full on your credit reports sends a more positive signal to lenders than having one or more debts listed as settled. Payment history accounts for 35% of your FICO credit score, so the fewer negative marks you have—such as late payments or settled debts—the better.

Can I get loan after settlement?

The bank or lender takes a look at the borrower's CIBIL score before offering him a loan and if the past record shows any settlement or non-payment, his loan is likely to get rejected.

How can I get out of debt without paying?

Ask for a raise at work or move to a higher-paying job, if you can. Get a side-hustle. Start to sell valuable things, like furniture or expensive jewelry, to cover the outstanding debt. Ask for assistance: Contact your lenders and creditors and ask about lowering your monthly payment, interest rate or both.

Can I remove settled debts from credit report?

That's a common question. Yes, you can remove a settled account from your credit report. A settled account means you paid your outstanding balance in full or less than the amount owed. Otherwise, a settled account will appear on your credit report for up to 7.5 years from the date it was fully paid or closed.

How Much Does debt settlement hurt your credit?

Does Debt Settlement Hurt Your Credit? Debt settlement affects your credit for up to 7 years, lowering your credit score by as much as 100 points initially and then having less of an effect as time goes on. The events that typically lead up to debt settlement will affect your credit score, too.

How long does it take to rebuild credit after debt settlement?

Your credit score will usually take between 6 and 24 months to improve. It depends on how poor your credit score is after debt settlement. Some individuals have testified that their application for a mortgage was approved after three months of debt settlement.

How long does it take to settle a debt?

If you're wondering how long it takes to pay off debt, Century can help you to set a plan. In general, a debt settlement program takes about 18-48 months, depending on your circumstances.

How long do settlements stay on credit report?

seven yearsA settled account remains on your credit report for seven years from its original delinquency date. If you settled the debt five years ago, there's almost certainly some time remaining before the seven-year period is reached. Your credit report represents the history of how you've managed your accounts.

How Much Does debt settlement hurt your credit?

Does Debt Settlement Hurt Your Credit? Debt settlement affects your credit for up to 7 years, lowering your credit score by as much as 100 points initially and then having less of an effect as time goes on. The events that typically lead up to debt settlement will affect your credit score, too.

How long does it take to improve credit score after debt settlement?

between 6 and 24 monthsHowever, a debt settlement does not mean that your life needs to stop. You can begin rebuilding your credit score little by little. Your credit score will usually take between 6 and 24 months to improve. It depends on how poor your credit score is after debt settlement.

How long does a debt settlement company have to make payments?

The debt payment schedule proposed by the company is as follows: After three months of making payments to the debt settlement company, ...

What would a debt settlement company advise the borrower to do?

During the process, the debt settlement company would advise the borrower to stop making payments to their creditors and instead make payments to the debt settlement company (albeit at a lower payment rate).

What is a debt covenant?

Debt Covenants Debt covenants are restrictions that lenders (creditors, debt holders, investors) put on lending agreements to limit the actions of the borrower (debtor). Intercreditor Agreement. Intercreditor Agreement An Intercreditor Agreement, commonly referred to as an intercreditor deed, is a document signed between one or more creditors, ...

What happens if a debt settlement falls through?

If a debt settlement falls through, the borrower will end up with more than the initial debt owed.

How to settle a debt?

In a debt settlement, the borrower may engage with a debt settlement company, who would act on the borrower’s behalf. The typical process for a debt settlement is as follows: 1 The borrower explains their financial situation to a debt settlement company. 2 During the process, the debt settlement company would advise the borrower to stop making payments to their creditors and instead make payments to the debt settlement company (albeit at a lower payment rate). 3 The debt settlement company would put the payments made by the borrower into a savings account#N#Savings Account A savings account is a typical account at a bank or a credit union that allows an individual to deposit, secure, or withdraw money when the need arises. A savings account usually pays some interest on deposits, although the rate is quite low.#N#. 4 Once the savings account’s reached a certain threshold, the debt settlement company would engage with the borrower’s creditors to negotiate a debt settlement. 5 If negotiations are successful, the debt settlement company would retain a portion of the money in the savings account (it is collected as fees by the debt settlement company) and distribute the remainder to the borrower’s creditors.

How long does bankruptcy last?

Avoiding bankruptcy. A debt settlement allows the borrower to avoid bankruptcy. Depending on the country, consumer bankruptcy can last up to ten years – significantly impacting the credit score of a borrower. In addition, declaring bankruptcy can potentially impact employability.

What is the legal status of a non-human entity that is unable to repay its outstanding debts?

Bankruptcy Bankruptcy is the legal status of a human or a non-human entity (a firm or a government agency) that is unable to repay its outstanding debts. , the borrower may attempt to reach a debt settlement with their creditors. In a debt settlement, the borrower may engage with a debt settlement company, who would act on the borrower’s behalf.

Where does the money come from in a debt settlement?

The money for those payments comes from an FDIC-insured escrow account — established in your name and managed by a bank or other third-party service provider. Each month, you deposit an agreed amount of money into that escrow account to fund the debt settlement effort. Those funds represent a portion of the monthly minimum payments you had been making before entering into the debt settlement plan.

Why are settlements greater than DSP fees?

of all settlements produced savings greater than the related DSP fees — in part because clients have the power to veto any proposed settlement for any reason.

What is DSP in bankruptcy?

The DSP option enables debtors to discharge their debts one at a time — an option not available either through DMPs or Chapter 13 bankruptcies. In those cases, debts are paid down simultaneously, and a failure to complete the program means no debts ever get discharged and collection activity — for the original loan terms — resumes. With that in mind, the 2017 AFCC report found that:

What is a DSP?

A DSP is the only type of debt-relief program, outside of bankruptcy, that can reduce or eliminate a substantial amount of your debt without making payment in full. The concept is simple. A debt settlement company reviews your finances and your debts and identifies which lenders are likely to accept an offer-in-compromise — payment of less than the full balance — in exchange for canceling the debt.

How many DSP clients settled at least one?

That number rises to 67 percent when still active accounts are included in the mix. And 42 percent of terminated cases settled at least one account.

How long does a client stay in the DSP program?

More than half of the clients that stay active for six months or more complete the program. And that rate increases to more than 60 percent for clients that stay in the program for more than two years.

What is debt relief?

Debt relief provides consumers repayment relief so they can get out of debt. Repayment relief can come in many forms like interest concessions, lower payments, and reduction of what’s owed. If you have money coming in every month but are struggling to make all your payments on time or are unable to pay down your debt, getting professional help can be a good idea.

What is debt settlement?

Debt settlement is an agreement made between a creditor and a consumer in which the total debt balance owed is reduced and/or fees are waived, and the reduced debt amount is paid in a lump sum instead of revolving monthly. Get Debt Help.

What do debt settlement companies have to explain?

Debt settlement companies must explain price and terms, including fees and any conditions on services.

Why Work with a Debt Settlement Company?

Often there’s a good reason – a layoff or reduction in pay, big medical bills, an unexpected emergency expense. No matter what the reason, it can be difficult to get out from under overwhelming debt on your own. This is particularly true for credit card debt or other revolving debt, that never seems to decrease, even if you’re paying monthly.

How long does it take for a debt settlement to pay?

Meanwhile, the company will negotiate with your creditors to settle for a lower amount. Once you’ve paid the amount the agreement is for into the escrow account, the debt settlement company will pay your creditor. This process can take 2-3 years.

How much does a debt settlement company charge?

Debt settlement companies charge a fee, generally 15-25% of the debt the company is settling. The American Fair Credit Council found that consumers enrolled in debt settlement ended up paying about 50% of what they initially owed on their debt, but they also paid fees that cut into their savings. The report gives an example of a debt settlement client whose $4,262 account balance was reduced to $2,115 with the settlement. So, at first it would seem she saved $2,147, the different between what she owed and what the settlement amount was. But she also paid $829 in fees to the debt settlement company, so she ended up saving $1,318.

What happens when you settle a debt?

In debt settlement, the company will instruct you to stop making payments to the creditors. Your accounts become delinquent, and the debt settlement company tries to negotiate a settlement on your behalf. In the meantime, you give your money to the debt settlement company, who also is not paying the creditor with it.

How much money did a debt settlement save?

The report found that debt settlement clients settled an average of about 50% of what was originally owed, but realized savings of about 30%.

What Is Debt Settlement?

Debt settlement refers to the process of clearing your debt with creditors for less money than you owe.

How Long Does Debt Settlement Take?

Clients of Level Financing typically complete their debt settlement program in 24 to 48 months. Settled debt may stay on your credit report for up to seven years; however, by comparison, a Chapter 7 bankruptcy can remain on your credit report for up to 10 years.

How much does level financing reduce credit card debt?

Clients of Level Financing who engage in debt settlement typically reduce their credit card debt by 45%-50%. It’s important to realize that a creditor has no legal obligation to negotiate outstanding debt, so there are no guarantees.

What happens if you stop paying debt?

Debt settlement is built around the idea that if you stop making regular monthly debt payments a creditor will accept less than the full amount due as settlement. In fact, creditors will often perceive it to be in their best interest to do so.

What is the first step toward a future free of perpetual debt?

Knowledge is power, and understanding your debt relief options is the first step toward a future free of perpetual debt. The next step is to take action.

How long does it take to settle a debt?

Be aware that settlement negotiations with creditors can take time – sometimes up to two years. Patience is critical.

How many people have been saved by level financing?

Since 2009, Level Financing’s experienced credit counseling experts have saved more than 20,000 people from financial ruin and the repressive burden of debt.

What is debt settlement?

Key Takeaways. Debt settlement is an agreement between a lender and a borrower to pay back a portion of a loan balance, while the remainder of the debt is forgiven. You may need a significant amount of cash at one time to settle your debt. Be careful of debt professionals who claim to be able to negotiate a better deal than you.

What are the downsides of debt settlement?

The Downsides of Debt Settlement. Although a debt settlement has some serious advantages, such as shrinking your current debt load , there are a few downsides to consider. Failing to take these into account can potentially put you in a more stressful situation than before.

Why do credit cards keep putting you on a debt?

It is usually because the lender is either strapped for cash or is fearful of your eventual inability to pay off the entire balance. In both situations, the credit card issuer is trying to protect its financial bottom line—a key fact to remember as you begin negotiating.

How long to cut down on credit card spending?

To raise your chances of success, cut your spending on that card down to zero for a three- to six-month period prior to requesting a settlement.

How to negotiate a credit card?

Start by calling the main phone number for your credit card’s customer service department and asking to speak to someone, preferably a manager, in the “debt settlements department.”. Explain how dire your situation is.

Is debt settlement good for you?

Although a debt settlement has some serious advantages, such as shrinking your current debt load, there are a few downsides to consider. Failing to take these into account can potentially put you in a more stressful situation than before.

Can a credit card company seize a debt?

Credit cards are unsecured loans, which means that there is no collateral your credit card company—or a debt collector —can seize to repay an unpaid balance. While negotiating with a credit card company to settle a balance may sound too good to be true, it’s not.

What is debt settlement?

Debt settlement is a practice that allows you to pay a lump sum that’s typically less than the amount you owe to resolve, or “settle,” your debt. It’s a service that’s typically offered by third-party companies that claim to reduce your debt by negotiating a settlement with your creditor. Paying off a debt for less than you owe may sound great at first, but debt settlement can be risky, potentially impacting your credit scores or even costing you more money.

How does debt settlement work?

The companies generally offer to contact your creditors on your behalf, so they can negotiate a better payment plan or settle or reduce your debt.

What is a resolve?

Why Resolve stands out: Resolve is a debt management service that provides users with features such as debt settlement and negotiation as well as budgeting tools and credit score monitoring.

How many payments do you have to make to a debt collector?

Once the debt settlement company and your creditors reach an agreement — at a minimum, changing the terms of at least one of your debts — you must agree to the agreement and make at least one payment to the creditor or debt collector for the settled amount.

What happens if you stop paying debt?

If you stop making payments on a debt, you can end up paying late fees or interest. You could even face collection efforts or a lawsuit filed by a creditor or debt collector. Also, if the company negotiates a successful debt settlement, the portion of your debt that’s forgiven could be considered taxable income on your federal income taxes — which means you may have to pay taxes on it.

How much debt has Freedom Financial resolved?

Why Freedom Financial stands out: Freedom Financial says it has resolved over $12 billion in debt since 2002. The company offers a free, “no-risk” debt relief consultation to help you decide if its program might work for you.

Can a company make a lump sum payment?

The company may try to negotiate with your creditor for a lump-sum payment that’s less than the amount that you owe. While they’re negotiating, they may require you to make regular deposits into an account that’s under your control but is administered by an independent third-party. You use this account to save money toward that lump payment.

What Is a Debt Management Plan?

A debt management plan lets you make a single monthly payment that covers all of your unsecured debts that are included in the plan. It’s not a loan and it won’t allow you to pay less than you owe, but a debt repayment plan can simplify the repayment process and shorten the time it takes you to get out of debt.

How long does it take to pay off a debt management plan?

You’ll also have to agree not to open any new credit cards during the debt management plan’s term. When the last payment is made, in three to five years, you’ll have paid off all the unsecured creditors covered by the plan.

How to get out of unsecured debt?

Debt management plans can be effective ways to get out from under unsecured debts. They involve fees, commitment and some restrictions on your ability to use credit. They also typically take a few to several years to complete, and won’t help you with mortgages and other secured loans or student loans. Before signing up with a consumer credit counseling agency, check the company’s reputation and resources and make sure you wouldn’t be better off using another method of handling debt, such as a consolidation loan or even bankruptcy.

What should be written in a credit counseling agreement?

An agreement with a credit counseling agency, including any oral promises made by a counselor or other representative, should be put in writing. There should be no pressure on a prospective client to sign an agreement immediately or without taking adequate time to read and consider the agreement.

How long does it take to pay off a debt?

The debt management plan generally aims to pay off all the unsecured debts within three to five years. Four years is a typical time to complete payoff. Debt management plans are only for unsecured debts such as credit cards and personal loans. They don’t include mortgages, auto loans and other debts secured with collateral.

What are the options for debt relief?

Options for debt relief include debt consolidation, debt settlement or filing for bankruptcy.

How much does a debt management agency charge?

The agency will also charge you a setup fee plus a monthly fee for the debt management service. The setup fee will usually be less than $75. The monthly fees may be a percentage of the monthly payment or a flat amount. A typical monthly fee will be less than $50. You may be able to negotiate a reduced fee or waiver if you are experiencing severe financial stress.

What is debt settlement?

What is a debt settlement program? Under a debt settlement plan, you’ll stop making payments to your creditors and you’ll begin paying a debt settlement company instead. After several months, as your accounts become delinquent, the debt settlement company will approach your creditors to try to settle the debt for a fraction of what you owe. The downside of a debt settlement plan is that your credit score will take a hit, and you may be unable to get credit or loans for years. And because creditors are not obligated to settle your debt, a debt settlement plan may leave you more deeply in debt.

How effective is debt management?

For many consumers, a debt management plan is a more effective approach to getting out of debt than a debt settlement plan. With a debt management plan, you’ll work with our credit counselors to create a budget you can live with while you pay down your debt quickly – usually in five years or less. Rather than paying your creditors directly each month, you’ll make one payment to ACCC, and our team will take responsibility for paying your creditors on your behalf. This helps to ensure your payments are made on time while simplifying your financial life and reducing your stress. We’ll also work with your creditors to ask for reductions in finance charges, interest rates, late fees and over-limit fees to reduce the amount you owe. We’ll also work with you to develop financial habits and practices that will let you live debt-free in the future. And with service fees that are among the lowest in the industry, you can be sure that a debt management plan with ACCC will help you save money over the cost of a debt settlement plan.

Is a debt settlement plan a good idea?

When you find yourself deeply in debt and can’t see a clear way out, a debt settlement plan may seem like a good idea. Perhaps you’ve been contacted by a debt settlement company or seen an advertisement that promised to show you how to settle debt for pennies on the dollar. But before you enter a debt settlement plan, it’s wise to seek advice from a professional credit counselor, because debt settlement programs aren’t always what they seem to be.

What are the risks of debt settlement?

Debt settlement comes with significant risks that you should be aware of before entering into an agreement. These risks include: 1 Damage to your credit. Debt settlement companies often encourage you to stop making payments to your creditors. This can severely damage your credit. It can also cause you to accrue interest, late fees and penalties on your existing debt, pushing you deeper into debt. You could receive calls from creditors or, in some cases, be sued for repayment. 2 High costs. Programs for debt settlement may require you to put money away for many months or years before your debt is settled. This can be very costly and, if you can’t afford the monthly payments, you may have to drop out of the program. Ensure you can truly afford to put away a significant amount of cash per month before entering into a debt settlement program. 3 No guarantee. Your creditors are not obligated to negotiate with you or a debt settlement company. There’s a chance that the debt settlement company you hire won’t be able to settle all of your debts, leaving you with growing debt during and after the process.

How does debt settlement affect credit?

Damage to your credit. Debt settlement companies often encourage you to stop making payments to your creditors. This can severely damage your credit. It can also cause you to accrue interest, late fees and penalties on your existing debt, pushing you deeper into debt.

How long has New Era Debt Solutions been in business?

New Era Debt Solutions has been in business for 22 years and settled more than $250 million in debt for its clients. With an A+ rating from the Better Business Bureau and a 4.9 out of 5 star rating on Trustpilot, it ranks high for customer satisfaction and tends to be well regarded by clients.

How many clients does Freedom Debt Relief have?

Freedom Debt Relief, the largest debt settlement service provider in the nation, has resolved more than $10 billion in debt for more than 650,000 clients since 2002. Those clients seem to be mostly satisfied with their experience, giving it 4.6 stars out of 5 on Trustpilot.

How long does it take to get a debt settlement with New Era?

The average time to complete a program with New Era is 28 months. It doesn’t disclose if there’s a minimum amount of qualifying debt to enroll in its program.

How long does it take Century Support Services to settle debt?

It’s been in business for nearly a decade, served more than 250,000 customers and settled more than $1.3 billion in debt. It typically takes around 24 to 48 months to complete debt settlement with this company.

Is debt settlement a last resort?

This service may sound attractive, but it comes with significant risks—it can damage your credit, be very costly and isn’t guaranteed to work. Because of the risks, debt settlement is typically considered an option of last resort. Yet, if it’s your only option, it’s crucial that you work with a reputable company.