Will I have to pay tax on my settlement?

You will have to pay your attorney’s fees and any court costs in most cases, on top of using the settlement to pay for your medical bills, lost wages, and other damages. Finding out you also have to pay taxes on your settlement could really make the glow of victory dim. Luckily, personal injury settlements are largely tax-free.

Are court ordered settlements taxable?

The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code.

Are legal settlements taxable?

The settlement money is taxable in the first place If your legal settlement represents tax-free proceeds, like for physical injury, then you won't get a 1099: that money isn't taxable. There is one exception for taxable settlements too.

Are business related settlement payments deductible?

Are business related settlement payments deductible? Yes, amounts paid for settlements are deductible as long as the basis of the suit is in fact a business matter and not personal. In other words, the acts that gave rise to the litigation must have been performed in the ordinary course of your business. The settlement amounts also cannot ...

What is deductible on a closing disclosure?

Typically, the only closing costs that are tax deductible are payments toward mortgage interest, buying points or property taxes. Other closing costs are not.

What closing expenses are tax deductible?

Generally, deductible closing costs are those for interest, certain mortgage points and deductible real estate taxes. Many other settlement fees and closing costs for buying the property become additions to your basis in the property and part of your depreciation deduction, including: Abstract fees.

What items from HUD-1 are tax deductible?

The only HUD-1 tax deductions t are mortgage interest or real estate taxes.

What is a payment deductible?

The amount you pay for covered health care services before your insurance plan starts to pay. With a $2,000 deductible, for example, you pay the first $2,000 of covered services yourself. After you pay your deductible, you usually pay only a. copayment.

What home improvements are tax deductible 2021?

"You can claim a tax credit for energy-efficient improvements to your home through Dec. 31, 2021, which include energy-efficient windows, doors, skylights, roofs, and insulation," says Washington. Other upgrades include air-source heat pumps, central air conditioning, hot water heaters, and circulating fans.

What can I write off when buying a house?

Unfortunately, most of the expenses you paid when buying your home are not deductible in the year of purchase. The only tax deductions on a home purchase you may qualify for is the prepaid mortgage interest (points)....These fees include:Title insurance.Appraisals.Abstract fees.Recording fees.Surveys.

How do you read a Settlement Statement for tax purposes?

4:3813:06How To Read A Closing Statement - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo it starts with the agreed upon sale price. And then debits and credits are applied to both buyerMoreSo it starts with the agreed upon sale price. And then debits and credits are applied to both buyer and seller. And then all of the numbers are added and subtracted at the very bottom.

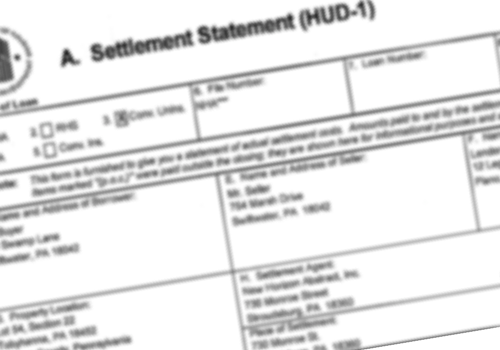

Is a HUD-1 the same as a closing statement?

The HUD-1 form, often also referred to as a “Settlement Statement”, a “Closing Statement”, “Settlement Sheet”, combination of the terms or even just “HUD” is a document used when a borrower is lent funds to purchase real estate.

Is homeowners insurance tax deductible?

Homeowners insurance is typically not tax deductible, but there are other deductions you can claim as long as you keep track of your expenses and itemize your taxes each year.

What are deductions used for?

A deduction is an expense that can be subtracted from a taxpayer's gross income in order to reduce the amount of income that is subject to taxation.

Are deductions good?

And deductions are a good thing because they lower your taxes. They'll help you shave hundreds, maybe even thousands of dollars off your tax bill. Simply put, a tax deduction is an expense or expenditure that can be subtracted from your income to reduce how much you pay in taxes.

How many deductions can I claim?

You can claim anywhere between 0 and 3 allowances on the 2019 W4 IRS form, depending on what you're eligible for. Generally, the more allowances you claim, the less tax will be withheld from each paycheck. The fewer allowances claimed, the larger withholding amount, which may result in a refund.

What part of mortgage is tax deductible?

Taxpayers can deduct the interest paid on first and second mortgages up to $1,000,000 in mortgage debt (the limit is $500,000 if married and filing separately). Any interest paid on first or second mortgages over this amount is not tax deductible.

Are appraisal fees tax deductible?

Generally, appraisal fees will be deductible on your Schedule C or Schedule E if the appraisal is conducted for business reasons. If you are buying or selling a personal property appraisal fees are not deductible.

What mortgage origination fees are tax deductible?

Points may also be called loan origination fees, maximum loan charges, loan discount, or discount points. Points are prepaid interest and may be deductible as home mortgage interest, if you itemize deductions on Schedule A (Form 1040), Itemized Deductions.

Are escrow fees tax deductible?

Escrow accounts. Many monthly house payments include an amount placed in escrow (put in the care of a third party) for real estate taxes. You may not be able to deduct the total you pay into the escrow account. You can deduct only the real estate taxes that the lender actually paid from escrow to the taxing authority.

What is escrow payment?

Escrow Payments. Setting up an escrow often means paying real estate taxes upfront. It pays to know exactly how much you paid towards your real estate taxes at the closing. These funds are tax deductible, just like the real estate taxes you pay directly to the county.

How much is a discount point on a loan?

They are a percentage of your loan amount. One point equals one percent of your loan. On a $100,000 loan, one point equals $1,000. You can deduct these points on your tax returns. Again, you can deduct the full amount of the points on a purchase. If you refinanced, you’ll prorate the deduction over the life of the loan.

What is discount point?

Discount Points. Discount points are different than origination points. These are points you pay in exchange for a lower interest rate. Again, it’s like prepaid interest. It’s how the lender makes money on your loan. Click to See the Latest Mortgage Rates. Discount points look the same as the origination points.

Can you deduct points on your tax return?

Whatever the case may be, you may be able to deduct those points on your tax return. Lenders look at points as prepaid interest. Since you get to deduct the interest you pay on your mortgage on an annual basis, it makes sense that you can deduct the points.

Can you deduct home insurance premiums?

You cannot, however, deduct the homeowner’s insurance premiums you pay upfront, so you’ll need to differentiate from the two. Make sure to ask your lender how much of the escrow account that you set up is comprised of real estate taxes. This way you know exactly how much you can claim on your taxes for deductions.

Can you deduct points on a mortgage?

If you purchased a home, you can deduct the full amount of the points during the year that you paid them. If you refinanced a mortgage, you must prorate the points over the term of the loan. For example, if you took out at 15-year loan, you’d write off a portion of the points every year for 15 years.

Can you deduct interest on a mortgage when closing?

Any interest you pay at the time of the closing can also be deducted. You prepay interest because you will not owe a mortgage payment the next month. Let’s say you close on November 15 th. You would not make a mortgage payment until January 1 st. This leaves all of the interest for the rest of November to be paid. The mortgage payment you make in January will cover December’s interest, though. If you close early in the month, you could pay a decent amount of money for interest that is worth deducting on your taxes.

What Are Seller Deductions?

Any prorated real estate taxes a home seller pays at closing are tax deductible. However, many of the closing costs listed on a settlement statement are deducted from sale proceeds. Lowered net proceeds reduce the capital gains the home seller may have garnered, thus reducing associated taxes. A capital gain is the improvement between a home's past purchase price and its later sale price, minus sale expenses.

What is a HUD-1 settlement statement?

The HUD-1 Settlement Statement is a breakdown of the expenses home sellers and homebuyers incur in a real estate sale. The settlement statement gives both parties a full picture of the expenses attached to the transaction. Some of the expenses assigned to home sellers and buyers on the HUD-1 form might be tax-deductible, and whether they are depends on the specifics of each transaction. Some of the more common examples of deductible expenses include loan origination fees, mortgage insurance premiums, and real estate tax payments.

Can you deduct mortgage insurance premiums?

Prepaid mortgage interest and mortgage insurance premiums are tax deductible, as are upfront real estate tax payments made from mortgage escrow funds.

Can you deduct points on a refinance?

However, on mortgage refinances, points paid are normally deducted as a prorated amount over the life of the loan.

Is a refinance loan deductible?

Homeowners who refinance are also given settlement statements. For homeowners, some of the costs for refinancing a mortgage loan are tax deductible. As with homebuyers, a refinanced mortgage's loan interest prepaid at closing is usually tax deductible. For property located in the San Francisco area, loan interest can become a significant expense and deduction. When you refinance your mortgage, points paid to lower your loan's interest rate can be deducted as well. However, on mortgage refinances, points paid are normally deducted as a prorated amount over the life of the loan.

Do home sellers pay closing costs?

Also, home sellers sometimes pay all or a portion of the buyer's closing costs. The closing costs sellers pay for buyers are deductible by buyers only, though the payment of such costs by sellers reduces those sellers' net capital gains and any taxes due.

Is mortgage interest deductible on HUD?

The mortgage interest paid for the remainder of the month in which the loan funds is also indicated on the HUD-1 statement and is tax deductible. Itemizing your taxes is the best way to take advantage of these deductions.

What expenses are capitalized in closing?

When determining whether you owe taxes on the sale of the property, you will subtract the sale price from the property's cost basis to determine the taxable gain from the sale before applicable exclusions are applied. According to the IRS, expenses such as title insurance, transfer taxes, surveys, and legal fees may be capitalized.

What are the expenses associated with buying a house?

Expenses include title insurance, your share of property taxes, interest, points, loan fees, escrow fees and recording fees, among others. While some of these expenses are not tax ...

Is closing expenses tax deductible?

Some expenses you incur at closing are not deductible. The insurance premium for your home insurance is not tax deductible and neither is your title insurance premium. Remember that private mortgage insurance may or may not be deductible, in whole or in part, depending upon your income level.

Is interest on a loan at closing tax deductible?

Interest on your loan paid at closing is tax deductible. Any prorated property taxes allocated as your expenses are also deductible. You can deduct loan origination fees or points, which are the fees a bank charges you for making the loan.

Is title insurance capitalized at closing?

Some expenses incurred at closing may be capitalized and be included in the cost basis of your property. The cost basis is the amount of money it costs you to acquire the property. When determining whether you owe taxes on the sale of the property, you will subtract the sale price from the property's cost basis to determine the taxable gain from the sale before applicable exclusions are applied. According to the IRS, expenses such as title insurance, transfer taxes, surveys, and legal fees may be capitalized.

How much gain can you exclude from your income?

For the sale of a residence, up to $250,000 ($500,000 on a joint return where you both lived in the residence) of gain can be excluded from income if you lived in and owned the house for two of the last five years.

Is a settlement statement tax deductible?

What items on the sale of home "Settlement Statement" are income tax deductible for the seller? Almost no closing costs incurred on a sale of a residence are deductible. An exception is any mortgage interest or real estate taxes charged at closing to bring them up to the closing date.

What can you deduct on closing statement?

Here’s a guide for you to determine proper treatment of the items you may find on your closing statement. The buyer of a principal residence may deduct interest, loan origination fees (typically referred to as “points,” also note that the IRS allows the buyer to deduct these even if they came out of the seller’s funds) and real estate taxes.

What expenses can be deducted from a sale of a home?

They may also include the following as selling expenses: attorney fees, closing costs, commissions, title fees, survey fees, recording of deed fees, transfer taxes, tax service fees, title policy fees, title insurance and utility service installation.

Can you forward closing statements to CPA?

Now is a great time to dig out those closing statements and forward them along to your CPA. When you do, feel free to contact a Clark Nuber professional if you have any questions regarding the treatment of items on your closing statement.

Can you deduct condo fees on taxes?

The buyer of a business or investment property may deduct condo fees, fees paid out of escrow (for utility bills, insurance, etc.), fire/casualty insurance premiums, interest, and real estate taxes. They can also increase their basis for the same items as the buyer of a principal residence.

What is a settlement statement?

A settlement statement is an itemized list of fees and credits summarizing the finances of an entire real estate transaction. It serves as a record showing how all the money has changed hands line by line.

Who is responsible for preparing the settlement statement?

Whoever is facilitating the closing — whether it be a title company, escrow firm, or real estate attorney — will be responsible for preparing the settlement statement.

Is a settlement statement the same as a closing statement?

Yes, a settlement statement is the same as a closing statement, though “settlement” is the formal term most likely to be used by the real estate industry.

What is an ‘excess deposit’ at closing?

A particular line item that causes confusion on the seller’s settlement statement is the “Excess Deposit.” What is an excess deposit, and who will receive the funds listed on that line?

What does an impound account do at closing?

At closing the buyer sets up an impound account that allows them to bundle the cost of their mortgage principal, taxes, mortgage insurance, and other monthly costs into one payment. The lender likes this because they can make sure the new owner will keep up to date with all the payments associated with the home.

Do you have to pay taxes at closing?

A buyer might be required to pay some charges, like homeowners insurance premiums or county taxes, in advance at closing.

Does the seller get a closing statement?

Buyers tend to sign the bulk of the paperwork at closing, making some sellers wonder if they will even receive a settlement statement.