Settlement costs (also known as closing costs) are the fees that the buyer and/or seller have to pay to complete the sale of the property. Responsibility for payment of this fee can be negotiated between the seller and the buyer. Laws require lenders to provide a loan estimate that discloses the closing costs for the transaction.

How to pay for closing costs?

- Present A Strong Offer: The easiest way to get the other party to cover closing costs is to present them with a strong offer. ...

- Offer A Quick Close: Truly great real estate deals favor both parties. ...

- Make Fewer Demands: No seller appreciates too many demands. ...

How much are closing costs for the buyer?

What are the typical real estate closing costs for buyers?

- Closing costs for buyers. Here is a quick breakdown of home buyer closing costs.

- Appraisal fees. ...

- Credit report fees. ...

- Mortgage origination fee. ...

- Title insurance policy fees. ...

- Escrow fees. ...

- Home inspection fee. ...

- Attorney fees. ...

- Documentation fees. ...

- Loan discount point fees. ...

What is the average closing cost for a buyer?

New data reveals the average closing costs are $6,693 across all home buyers, and slightly less for first-time buyers. You may be able to negotiate part of your closing costs.

Are closing costs negotiable?

Some closing costs are negotiable: attorney fees, commission rates, recording costs, and messenger fees. Check your lender’s good-faith estimate (GFE) for an itemized list of fees. You can also use your GFE to comparison shop with other lenders.

What is the difference between settlement and closing?

A closing is often called "settlement" because you, as buyer, along with your lender and the seller are "settling up" among yourselves and all of the other parties who have provided services or documents to the transaction.

What does it mean to negotiate closing costs?

Anytime you're making a large purchase, it's your responsibility to negotiate for the best deal possible. Your lender will not offer to charge you fewer fees, and the seller will not offer to step in and help pay for the closing costs – you have to make the request.

Who pays closing cost?

Typically, buyers and sellers each pay their own closing costs. A home buyer is likely to pay between 2% and 5% of their loan amount in closing costs, while the seller could pay 5% to 6% of the sale price to their real estate agent.

How can I get around closing costs?

The best ways to avoid closing costsLook for a loyalty program. Some banks offer help with their closing costs for buyers if they use the bank to finance their purchase. ... Close at the end the month. ... Get the seller to pay. ... Wrap the closing costs into the loan. ... Join the army. ... Join a union. ... Apply for an FHA loan.

How do you negotiate lower closing costs?

7 strategies to reduce closing costsBreak down your loan estimate form. ... Don't overlook lender fees. ... Understand what the seller pays for. ... Think about a no-closing-cost option. ... Look for grants and other help. ... Try to close at the end of the month. ... Ask about discounts and rebates.

Can closing costs be included in loan?

Including closing costs in your loan — or “rolling them in” — means you are adding the closing costs to your new mortgage balance. This is also known as financing your closing costs. Lenders may refer to it as a “no-cost refinance.” Financing your closing costs does not mean you avoid paying them.

Who pays closing costs in Oklahoma?

Buyers and sellers in Oklahoma pay an average of $381.83 in tax combined for the closing. This accounts for 12.97% of the total average closing cost in Oklahoma.

Can I roll closing costs into my VA loan?

That's OK! The VA loan allows you to include some of the closing costs into your total loan amount. The big thing is that you can roll your funding fee into the total mortgage amount. Although you'll pay more in interest, this can help you get into a home now.

What is settlement fee?

In real estate, a settlement fee is a charge that covers expenses in excess of the amount a person pays to purchase or sell a property. Settlement fees can encompass many types of expenses, but often include such things as application and attorney ’s fees, loan origination fees, and fees for title searches.

What is a point fee?

Points are fees that are charged a single time and can be negotiated with a lender to lower the interest rate a borrower will pay on a mortgage in exchange for paying a particular sum up front.

What is a point in a mortgage?

Points are fees that are charged a single time and can be negotiated with a lender to lower the interest rate a borrower will pay on a mortgage in exchange for paying a particular sum up front. For example, paying $1,000 US Dollars (USD) up front might lower a person’s interest paid over the life of his loan by one percent. Points paid at settlement are tax deductible in some jurisdictions as well.

Do appraisers charge fees?

Appraisers and home inspectors charge fees, which are often included in settlement fee totals. In most cases, the settlement fees a seller pays are negotiable. In order to make his home more attractive or easier to buy, a seller may agree to pay one or more of the settlement fees usually paid by the buyer.

Is it legal to have a seller assist with a settlement fee?

Having the seller assist with a settlement fee is usually legal, as long as the seller's contribution is detailed in the official agreement between the buyer and seller and doesn't violate any terms set by the lender.

Is an appraisal included in settlement fees?

Lenders may also require an inspection by a professional home inspector in order to analyze the structure of the property and look for evidence of issues such as termites. Appraisers and home inspectors charge fees, which are often included in settlement fee totals.

What is settlement fee?

Definition of Settlement Fee. When you're buying a home with a mortgage, it's important to understand the type of fees you might incur. Most people are familiar with the term closing costs, or the genuine third-party costs that are associated with the closing of a real estate transaction, and expect to pay these expenses when they purchase ...

What are closing costs?

Closing costs are the legitimate third-party expenses you incur when you buy a property. These are expenses that you would never get back even if you sold the home a day after you closed on it. Examples include the loan application fee, points, title search fees, appraisal fee, home inspection fees, escrow fees, credit reports, courier fees, ...

How Do You Calculate Settlement Costs?

Right at the beginning of your loan application, you'll get a good faith estimate. This document outlines all the fees you should expect to pay for your mortgage such as the loan application fee, appraiser's fees, points, title insurance, mortgage insurance and accrued mortgage interest from the closing date until the end of the month. It's an estimate of the total cost of buying the property and it's provided to help you compare the cost of different mortgage providers.

What are closing costs when buying a home?

Most people are familiar with the term closing costs, or the genuine third-party costs that are associated with the closing of a real estate transaction, and expect to pay these expenses when they purchase a property.

What happens when you close a mortgage?

When you close the mortgage loan, on top of the closing costs, you're going to pay interest on the new mortgage from the day you close until the day the first monthly mortgage payment is due. You're also going to pay your share of the property taxes and HOA fees the seller has paid upfront for the property from the closing date to the end of the month. On top of that, the lender will collect escrow reserves upfront on account of future property taxes and homeowner's insurance. And don't forget the down payment. That's required at closing, too, and it goes towards the equity in your home.

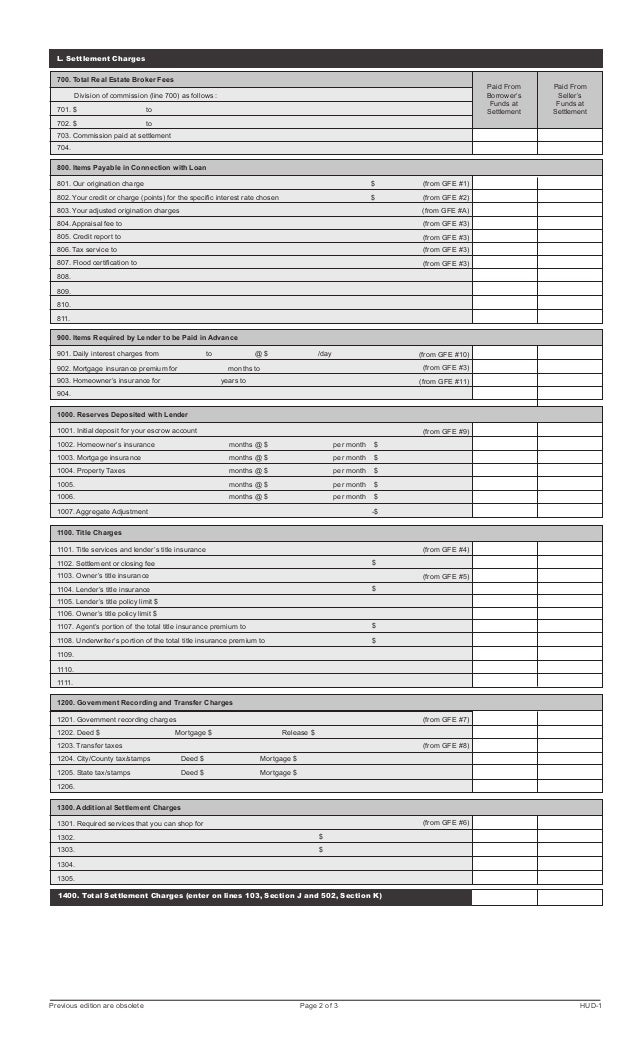

What is the HUD-1 settlement statement?

This looks a bit like the good faith estimate, only now it shows the true closing costs, including the final cost of items that could only be estimated before.

What happens when you combine closing costs?

If you combine all these various sums together and add them to the genuine closing costs, you get a complete account of everything you need to purchase the property. This total amount is what real estate professionals are referring to when they talk about "settlement costs," "settlement expenses" or "settlement fees."

Origination Costs

Title Settlement Closing Fee and Other Costs

- Additional costs may also apply whenever you take out a loan. Many of the title costs vary from company to company, allowing you to shop around to get a good deal on title as some are owned by attorneys, while others are not. Usually, you will pay a fee for title services, sometimes there are costs the seller will pay as well. A title is a document...

Administrative Settlement Fees

- Before finalizing a home sale, lenders and other agents must perform a range of administrative tasks. These imply additional fees. Financial institutions, for instance, have to ensure that they have collateral for making any loan. This usually involves an appraisal fee to confirm the value of your property. Banks and brokers will also need to check your credit history to determine if they …

How to Find Your Title Settlement Closing Fee

- You can find title settlement closing fees on your loan estimate and closing disclosure. This legally required document lists all the costs, risks and features associated with your mortgage. Lenders are obliged to provide you with a loan estimate within three days of making your application. Learning more about title settlement closing fees lets you plan for the transaction b…