What is a Settlement Cost Booklet?

What is a booklet for a home loan?

What is a RESPA booklet?

How long do you keep a booklet in your loan application?

How long do you have to deliver a booklet to a lender?

Can you change the name of HUD?

Do you have to send a booklet to a borrower?

See 2 more

What kind of loan transaction requires the settlement cost booklet?

The Real Estate Settlement Procedures Act (RESPA) requires lenders and mortgage brokers to give you this booklet within three days of applying for a mortgage loan. RESPA is a federal law that helps protect consumers from unfair practices by settlement service providers during the home-buying and loan process.

What is the difference between a HUD and a settlement statement?

The HUD-1 form, often also referred to as a “Settlement Statement”, a “Closing Statement”, “Settlement Sheet”, combination of the terms or even just “HUD” is a document used when a borrower is lent funds to purchase real estate. Another acronym used in relation to the HUD form is GFE, which means 'Good Faith Estimate'.

What is a HUD settlement agreement?

The HUD-1 Settlement Statement is a document that lists all charges and credits to the buyer and to the seller in a real estate settlement, or all the charges in a mortgage refinance. If you applied for a mortgage on or before October 3, 2015, or if you are applying for a reverse mortgage, you receive a HUD-1.

What replaced the HUD settlement statement?

The Closing Disclosure combines and replaces the HUD-1 Settlement Statement and the final Truth-in-Lending (TIL) statement. The form mirrors the information provided on the Loan Estimate.

When should I receive the HUD-1 Settlement Statement?

In such case, the completed HUD-1 or HUD-1A shall be mailed or delivered to the borrower, seller, and lender (if the lender is not the settlement agent) as soon as practicable after settlement.

Are HUD-1 Settlement Statements still used?

The HUD-1 Settlement Statement is a standard government real estate form that was once used by settlement agents, also called "closing agents," to itemize all charges imposed upon a borrower and seller for a real estate transaction. The statement is no longer used, with one exception: reverse mortgages.

What is the primary purpose of the settlement statement?

A settlement statement provides a breakdown of all the closing costs and credits involved in a real estate transaction or refinance.

How do I get my HUD payoff statement?

Requests for payoff statements, subordinations, releases, and other documentation specific to these programs can be submitted to:Payoff Requests: [email protected] Requests: [email protected] Requests: [email protected] Partial Claim document submittal: [email protected] items...

Is a settlement statement the same as a closing statement?

A settlement statement is a document listing the terms and conditions of a settlement agreement and details all related costs or credits due to each party. A mortgage loan settlement statement is commonly known as a closing statement.

Is the CD the same as the HUD?

The Closing Disclosure (CD - formerly the HUD-1 Uniform Settlement Statement) is a three-page, government-mandated form that details the costs associated with a real estate transaction. The borrower should receive a copy of the CD at least one day prior to the closing.

What is a final HUD statement?

A HUD-1 form, also called a HUD-1 Settlement Statement, is a standardized mortgage lending document. Creditors or their closing agents use this form to create an itemized list of all charges and credits to the buyer and to the seller in a consumer credit mortgage transaction.

What is the difference between a HUD-1 and hud1a?

Differences. As the HUD 1A form is used in refinancing transactions, its principle section is L, pertaining to the loan. The HUD 1 form is longer by about a page. The additional sections in HUD 1 relate to the sale transaction.

Is a settlement statement the same as a closing statement?

A settlement statement is a document listing the terms and conditions of a settlement agreement and details all related costs or credits due to each party. A mortgage loan settlement statement is commonly known as a closing statement.

What is the difference between a closing disclosure and a settlement statement?

While closing disclosures provide information about a borrower's loan, settlement statements do not include loan information. Settlement statements are used for commercial transactions and cash closings.

Which type of loan will use a HUD-1 instead of a closing disclosure?

A HUD-1 form is most commonly used for reverse mortgages and mortgage refinance transactions. Now, for most kinds of mortgage loans, borrowers receive a form called the Closing Disclosure instead of a HUD-1 form.

What does HUD mean in real estate?

U.S. Department of Housing and Urban DevelopmentHUD Homes | HUD.gov / U.S. Department of Housing and Urban Development (HUD)

Settlement cost booklet - Wells Fargo

Table Of Contents Table Of Contents 2 1. Introduction 4 2. Before You Buy 5 2.1 Are You Ready to Be a Homeowner? 5 3. Determining What You Can Afford 6

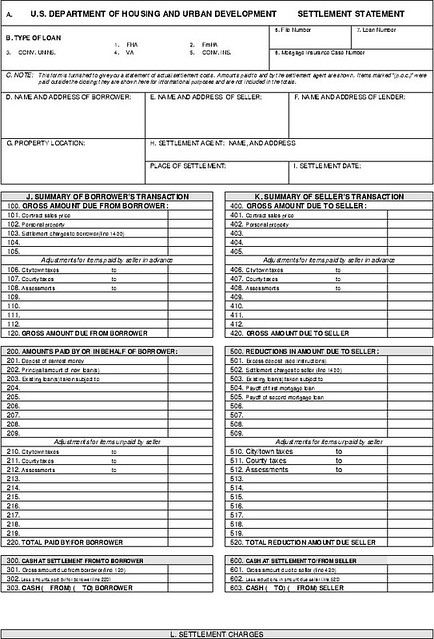

A. Settlement Statement (HUD-1)

A. Settlement Statement (HUD-1) Previous edition are obsolete Page 1 of 3 HUD-1 B. Type of Loan J. Summary of Borrower’s Transaction 100. Gross Amount Due from Borrower C. Note:

Your home loan toolkit - Consumer Financial Protection Bureau

2. OUR HOME LOAN TOOLKITY. Page 2. This booklet was created to comply with federal law pursuant to 12 U.S.C. 2604, 12 CFR 1024.6, and 12 CFR 1026.19(g).

I. Introduction

The Real Estate Settlement Procedures Act (RESPA) requires lenders and mortgage brokers to give you this booklet within three days of applying for a mortgage loan. RESPA is a federal law that helps protect consumers from unfair practices by settlement service providers during the home-buying and loan process.

II. Before You Buy

Buying a home is one of the most exciting events in your life and is likely to be the most expensive purchase that you will ever make. Before you make a commitment, make sure you are ready.

III. Determining What You Can Afford

To determine how much you can afford, you first need to know your monthly income. Second, you will need to calculate your monthly expenses which may include credit card bills, car payments, insurance premiums and all other debts.

IV. Shopping for a House

Frequently, the first person you consult about buying a home is a real estate agent or broker. Although these agents and brokers provide helpful advice, they may legally be representing the interests of the seller and not yours. You can ask your family and friends for recommendations.

V. Shopping for a Loan

Your choice of mortgage lender or broker, as well as type of loan itself, will influence your settlement costs and your monthly mortgage payment. You may find a listing of local lenders and mortgage brokers in the yellow pages and a listing of rates in your local newspaper.

VI. Good Faith Estimate (GFE)

The GFE is a three page form designed to encourage you to shop for a mortgage loan and settlement services so you can determine which mortgage is best for you. It shows the loan terms and the settlement charges you will pay if you decide to go forward with the loan process and are approved for the loan.

VII. Shopping for Other Settlement Services

There are other settlement services that the lender will require for your loan. You may be able to shop for these services or you may choose providers identified on the written list you receive from the loan originator. If you select providers on the list, the charges shown on the GFE must be within the 10% tolerance.

How much is one point on a $100,000 loan?

one point on a $100,000 loan, the loan officer is talking about one percent of the loan, which equals $1,000. Lenders offer different interest rates on loans with different points. There are three main choices you can make about points. You can decide you don’t want to pay or receive points at all.

How much of your credit score is based on how much you owe?

About 35% of your credit scores are based on whether or not you pay your bills on time. About 30% of your credit scores are based on how much debt you owe.

Do lenders charge for credit report?

Lenders can charge you only a small fee for getting your credit report—and some lenders provide the Loan Estimate without that fee. ¨ Compare Total Loan Costs Review your Loan Estimates and compare Total Loan Costs, which you can see under Section D. at the bottom left of the second page of the Loan Estimate.

Is the interest rate on a loan estimate a guarantee?

The interest rate on your Loan Estimate is not a guarantee. If your rate is floating and it is later locked, your interest rate will be set at that later time. Also, if there are . changes in your application—including your loan amount, credit score, or verified income—your rate and terms will probably change too.

What is section 19 of RESPA?

2617 (a)), the Bureau may issue a revised or separate special information booklet that deals with these transactions, or the Bureau may choose to endorse the forms or booklets of other Federal agencies.

Can special information booklets be reproduced?

The special information booklet may be reproduced in any form, provided that no change is made other than as provided under paragraph (d) of this section. The special information booklet may not be made a part of a larger document for purposes of distribution under RESPA and this section.

What is a Settlement Cost Booklet?

Settlement Cost Booklet is an informational booklet that helps the borrowers become familiar with the home-buying and mortgage process so that they make informed decisions and avoid common pitfalls. It includes topics such as steps in buying a home, mortgage process, fees, disclosures, understanding GFE and HUD-1, and other information.

What is a booklet for a home loan?

The booklet is a good place to start for first time homebuyers and those looking to refinance. It provides a general overview of the process for buying a home and obtaining a mortgage loan. You will get familiar with some of the documents and disclosures. However, the guide is a general purpose document. You should work with your real estate agent and loan originator to understand the loan terms, fees, disclosures, and important steps in the process that allow to your particular circumstance.

What is a RESPA booklet?

The lender is required to provide a special information booklet as per §1024.6 Regulation X, which implements Real Estate Settlement Procedures Act (RESPA). Regulation X and provisions of RESPA are enforced by Consumer Finance Protection Bureau (CFPB). Settlement Cost Booklet is the special information booklet designed by HUD to meet the requirements of Regulation X.

How long do you keep a booklet in your loan application?

We recommend maintaining the evidence of delivery of booklet in the loan file for a period of at least five years from the date of settlement. The document retention period will be consistent with other record-keeping requirements of Regulation X. For declined, cancelled, or withdrawn applications, the evidence of delivery should be maintained for as long as the loan application file is maintained, which would normally be at least 25 months from date of action taken to be consistent with Regulation B recordkeeping requirements.

How long do you have to deliver a booklet to a lender?

Regulation X requires you to deliver or place the booklet in the mail not later than three business days following receipt of the loan application. If you deny the loan application before the end of the three-business-day period, then you need not provide the booklet to the borrower. Business day means a day on which your offices are open to the public for carrying on substantially all of its business functions.

Can you change the name of HUD?

Do not make any changes to the content of the booklet. The only change allowed is to replace HUD’s name and address with that of CFPB. See the specific requirements of Regulation X before making any changes.

Do you have to send a booklet to a borrower?

If the borrower is using a broker then the broker is required to send the booklet. In that case, you are not required to send the booklet and you can rely on the broker. However, you run the risk of non-compliance if the broker is not able to provide evidence of the delivery of the booklet. Therefore, we recommend sending the booklet yourself for all loans, irrespective of whether the broker is sending the booklet or not.