Will I have to pay tax on my settlement?

You will have to pay your attorney’s fees and any court costs in most cases, on top of using the settlement to pay for your medical bills, lost wages, and other damages. Finding out you also have to pay taxes on your settlement could really make the glow of victory dim. Luckily, personal injury settlements are largely tax-free.

How much will the IRS usually settle for?

The IRS can seize up to the total amount of your tax debt from your bank account. For many taxpayers, this means the IRS can totally wipe out their account. How much will the IRS usually settle for? The average amount of an IRS settlement in an offer in compromise is $6,629.

How to negotiate a tax settlement with the IRS?

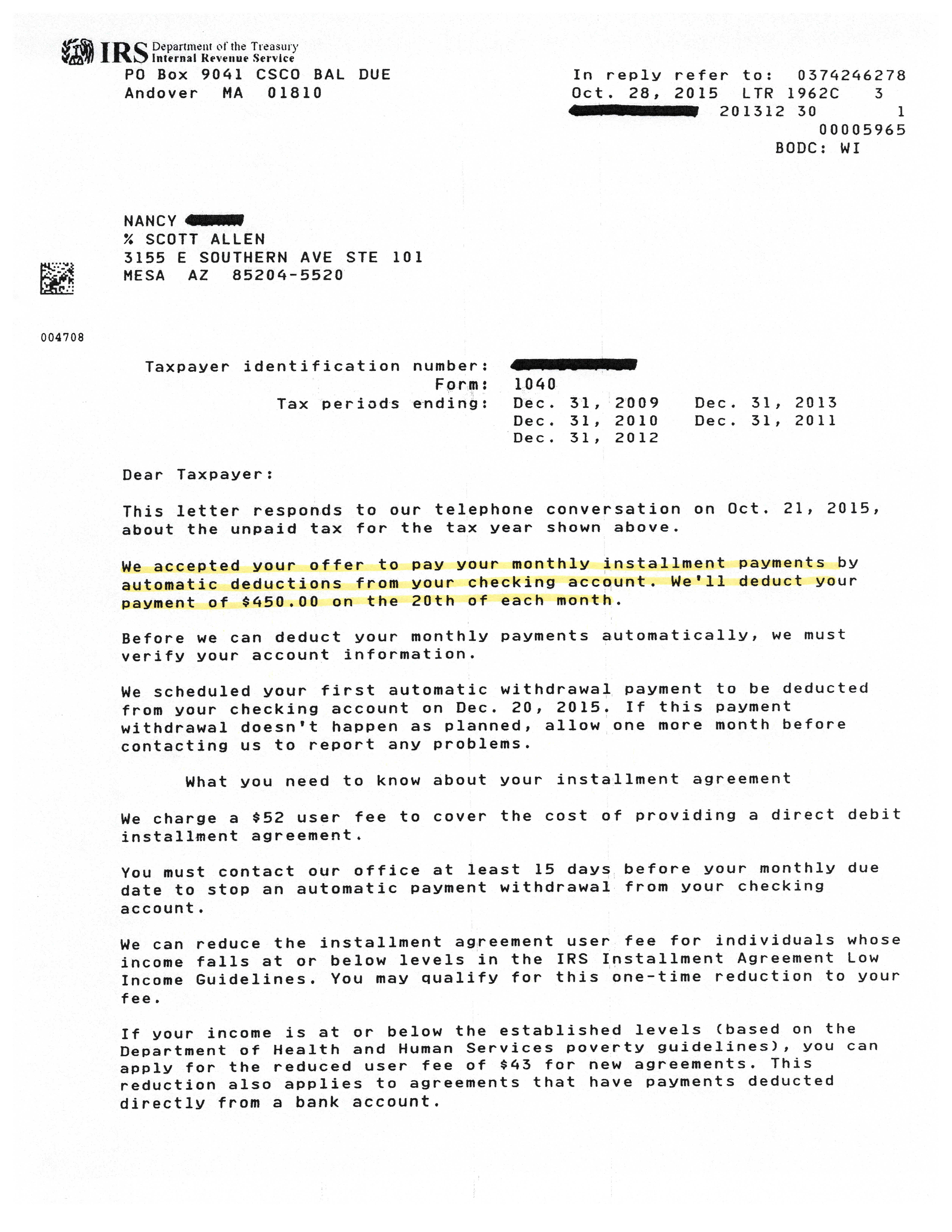

- Let the IRS know you'll pay the debt off within six years—but ideally within three years. 7

- Aim high. ...

- The regular (usually monthly) tax payment you introduce to the IRS should be tied to existing IRS criteria. ...

How often does IRS accept offer in compromise?

How often does IRS Accept offer in compromise? In general, IRS OIC acceptance rate is fairly low. In 2019, only 1 out of 3 were accepted by the IRS. In 2019, the IRS accepted 33% of all OICs. How hard is it to get an offer in compromise with the IRS? But statistically, the odds of getting an IRS offer in compromise are pretty low.

See more

Will IRS take a lump sum settlement?

A "lump sum cash offer" is defined as an offer payable in 5 or fewer installments within 5 or fewer months after the offer is accepted. If a taxpayer submits a lump sum cash offer, the taxpayer must include with the Form 656 a nonrefundable payment equal to 20 percent of the offer amount.

Will the IRS take a settlement offer?

Yes – If Your Circumstances Fit. The IRS does have the authority to write off all or some of your tax debt and settle with you for less than you owe. This is called an offer in compromise, or OIC.

How likely is the IRS to accept an offer in compromise?

A rarity: IRS OIC applications and acceptances for 2010-2019 In 2019, the IRS accepted 33% of all OICs. There are two main reasons that the IRS may not accept your doubt as to collectibility OIC: You don't qualify. You can't pay the calculated offer amount.

How much will the IRS usually settle for?

Each year, the Internal Revenue Service (IRS) approves countless Offers in Compromise with taxpayers regarding their past-due tax payments. Basically, the IRS decreases the tax obligation debt owed by a taxpayer in exchange for a lump-sum settlement. The average Offer in Compromise the IRS approved in 2020 was $16,176.

What happens if I owe the IRS 100000?

The IRS may take any of the following actions against taxpayers who owe $100,000 or more in tax debt: File a Notice of Federal Tax Lien to notify the public of your delinquent tax debt. Garnish your wages or seize the funds in your bank account. Revoke or deny your passport application.

What happens if you owe the IRS more than $50000?

If you owe more than $50,000, you may still qualify for an installment agreement, but you will need to complete a Collection Information Statement, Form 433-A. The IRS offers various electronic payment options to make a full or partial payment with your tax return.

What do I do if the IRS rejects my offer in compromise?

Remember to mail your appeal to the office that sent you the rejection letter. You can request an Appeals conference by preparing either a Form 13711, Request for Appeal of Offer in CompromisePDF, or a separate letter with the following information: Name, address, Tax Identification Number and daytime telephone number.

How long does it take for IRS to Accept Offer in Compromise?

about six monthsIn most cases, the IRS takes about six months to decide whether to accept or reject your offer in compromise. However, if you have to dispute or appeal their decision, the process can take much longer.

Can a tax attorney negotiate with IRS?

However, tax lawyers can negotiate agreements with the IRS, such as offers in compromise, that allow you to pay less than your total balance. As a result, you can save hundreds or thousands of dollars while resolving your back taxes at the same time. Tax attorneys can guide you through an audit.

Does IRS ever forgive debt?

The short answer is Yes, but it's best to enlist professional assistance to obtain that forgiveness. Take a look at what every taxpayer needs to know about the IRS debt forgiveness program.

Who qualifies for IRS Fresh Start?

People who qualify for the program Having IRS debt of fifty thousand dollars or less, or the ability to repay most of the amount. Being able to repay the debt over a span of 5 years or less. Not having fallen behind on IRS tax payments before. Being ready to pay as per the direct payment structure.

Is there a one time tax forgiveness?

One-time forgiveness, otherwise known as penalty abatement, is an IRS program that waives any penalties facing taxpayers who have made an error in filing an income tax return or paying on time. This program isn't for you if you're notoriously late on filing taxes or have multiple unresolved penalties.

How do I negotiate a settlement with the IRS?

Apply With the New Form 656 An offer in compromise allows you to settle your tax debt for less than the full amount you owe. It may be a legitimate option if you can't pay your full tax liability or doing so creates a financial hardship. We consider your unique set of facts and circumstances: Ability to pay.

How do I write an offer in compromise letter to the IRS?

You must provide a written statement explaining why the tax debt or portion of the tax debt is incorrect. In addition, you must provide supporting documentation or evidence that will help the IRS identify the reason(s) you doubt the accuracy of the tax debt.

Can you negotiate with IRS to remove penalties and interest?

First, you should know that it is possible to negotiate for an abatement of penalties and interest, but it is at the discretion of the IRS agent with whom you are working. Second, it takes time, sometimes a year or two, to negotiate with the IRS for a reduction of interest or penalties.

How can I avoid paying taxes on debt settlement?

According to the IRS, if a debt is canceled, forgiven or discharged, you must include the canceled amount in your gross income, and pay taxes on that “income,” unless you qualify for an exclusion or exception. Creditors who forgive $600 or more are required to file Form 1099-C with the IRS.

How Does a Tax Settlement Work?

You determine which type of settlement you want and submit the application forms to the IRS. The IRS reviews your application and requests more information if needed. If the IRS does not accept your settlement offer, you need to make alternative arrangements. Otherwise, collection activity will resume. If the IRS accepts your settlement offer, you just make the payments as arranged.

How to settle taxes owed?

These are the basic steps you need to follow if you want to settle taxes owed. File Back Taxes —The IRS only accepts settlement offers if you have filed all your required tax returns. If you have unfiled returns, make sure to file those returns before applying.

What is a tax settlement?

A tax settlement is when you pay less than you owe and the IRS erases the rest of your tax amount owed. If you don’t have enough money to pay in full or make payments, the IRS may let you settle. The IRS also reverses penalties for qualifying taxpayers.

How long do you have to pay back taxes?

If you personally owe less than $100,000 or if your business owes less than $25,000, it is relatively easy to get an installment agreement. As of 2017, the IRS gives taxpayers up to 84 months (7 years) to complete their payment plans.

What is partial payment installment agreement?

A partial payment installment agreement allows you to make monthly payments on your tax liability. You make payments over several years, but you don’t pay all of the taxes owed. As you make payments, some of the taxes owed expire. That happens on the collection statute expiration date.

What happens if you default on a settlement offer?

At that point, you are in good standing with the IRS, but if you default on the terms of the agreement, the IRS may revoke the settlement offer . To explain, imagine you owe the IRS $20,000, and the IRS agrees to accept a $5,000 settlement.

Why do you settle taxes if you don't qualify?

If you don’t qualify for a tax settlement for less money, then it will ensure you are paying back a lower amount of taxes and penalties that are due.

What is the tax rule for settlements?

Tax Implications of Settlements and Judgments. The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code. IRC Section 104 provides an exclusion ...

What is the exception to gross income?

For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury.

What is the purpose of IRC 104?

IRC Section 104 provides an exclusion from taxable income with respect to lawsuits, settlements and awards. However, the facts and circumstances surrounding each settlement payment must be considered to determine the purpose for which the money was received because not all amounts received from a settlement are exempt from taxes.

What is employment related lawsuit?

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example lost wages, business income and benefits, are not excludable form gross income unless a personal physical injury caused such loss.

What is an interview with a taxpayer?

Interview the taxpayer to determine whether the taxpayer provided any type of settlement payment to any of their employees (past or present).

Is a settlement agreement taxable?

In some cases, a tax provision in the settlement agreement characterizing the payment can result in their exclusion from taxable income. The IRS is reluctant to override the intent of the parties. If the settlement agreement is silent as to whether the damages are taxable, the IRS will look to the intent of the payor to characterize the payments and determine the Form 1099 reporting requirements.

Is emotional distress taxable?

Damages received for non-physical injury such as emotional distress, defamation and humiliation, although generally includable in gross income, are not subject to Federal employment taxes. Emotional distress recovery must be on account of (attributed to) personal physical injuries or sickness unless the amount is for reimbursement ...

How long does it take to pay IRS offer in compromise?

The first option requires that you pay 20% of your offer amount upfront and then remit the remainder of the offer within 5 months from the date that an Offer in Compromise is accepted. The second option doesn’t require the 20% upfront deposit but instead requires the first payment to be paid with the submission of the offer and for the remaining amount to be paid within 6 to 24 months in accordance with your proposed offer terms. The formula to calculate your offer is below depending on which option is chosen.

What is interest and penalties?

Interest and penalties are imposed by law to incentivize people to timely pay their taxes each year. With limited exceptions, interest and penalties cannot be removed. Settling outstanding tax debt is most often accomplished by pursuing an Offer in Compromise.

Can you settle your tax debt with the IRS?

In closing, you can settle your tax debts with the IRS if you can demonstrate that you are unable to pay back the amount of tax, interest, and penalty in full and you submit an offer based on a Reasonable Collection Potential that is lower than the amount owed.

Can the IRS settle back taxes?

The IRS will agree to settle back tax debt in cases where a person is unable to pay back the tax debt in full within the time allowed by law. IRS tax settlements are often accomplished through use of the Offer in Compromise program (also sometimes referred to as the Fresh Start Program).

What happens if you accept a tax offer?

You must meet all the Offer Terms listed in Section 7 of Form 656, including filing all required tax returns and making all payments; Any refunds due within the calendar year in which your offer is accepted will be applied to your tax debt;

How long does it take for an IRS offer to be accepted?

Your offer is automatically accepted if the IRS does not make a determination within two years of the IRS receipt date.

Do you have to pay the application fee for low income certification?

If accepted, continue to pay monthly until it is paid in full. If you meet the Low Income Certification guidelines, you do not have to send the application fee or the initial payment and you will not need to make monthly installments during the evaluation of your offer. See your application package for details.

Does the IRS return an OIC?

The IRS will return any newly filed Offer in Compromise (OIC) application if you have not filed all required tax returns and have not made any required estimated payments. Any application fee included with the OIC will also be returned. Any initial payment required with the returned application will be applied to reduce your balance due. This policy does not apply to current year tax returns if there is a valid extension on file.

What happens if you owe back taxes to the IRS?

When you owe back taxes to the IRS, you’re indebted to the government itself – and there are very few ways out of that debt. In some cases, taxpayers can argue that the debt they’re facing isn’t valid and argue doubt as to their own liability.

What to do if you owe IRS money?

If you owe the IRS money, you may be able to negotiate a settlement in order to resolve the debt. This can be a tricky process, so you want to consider hiring a professional to handle the offer in compromise.

What happens when you have proof of wrongfully charged?

When a taxpayer has definitive proof that they’ve been wrongfully charged, such as having the paperwork to back up a deduction the IRS rescinded, they may be able to negotiate a reduced or completely pardoned debt.

Why do you offer in compromise?

An offer in compromise can be an effective way to reduce what you owe, and help you get back into good standing with the IRS. But offers in compromise are not always necessary, when there are other, potentially easier alternatives.

When neither a payment plan nor an offer in compromise is in the cards, what is your best bet?

When neither a payment plan nor an offer in compromise is in the cards, your best bet might be to just focus on fighting back against the IRS’s collection actions, until you can get back on your feet.

Can you negotiate with the IRS about debt?

There are very few ways around a debt with the IRS. The government expects you to pay them one way or another, and even in the most desperate cases, your best bet is to negotiate for a reduced debt rather than a full pardon. Working with experienced tax professionals is key, as the IRS can be particularly picky about tax debt settlements and won’t accept just any offer.

Is a compromise a part of negotiating a tax settlement?

Drafting an effective offer in compromise is still just one part of negotiating a tax settlement with the IRS, albeit a crucial one.

What are the chances that the IRS will approve my request for an OIC?

In 2019, the IRS received 54,225 offers in compromise and accepted only 17,890 of them — that’s a success rate of roughly 33%.

How does the IRS calculate the minimum offer it will accept?

The IRS formula to calculate your OIC is a two-step process based on your monthly income and the value of your assets, so the IRS can estimate your “reasonable collection potential.” The OIC formula, which determines what you’re able to pay, looks like this:

What do I need to know as a low-income business owner with tax debt?

If you have a past-due tax bill for your business and personal tax returns, it’s important to know how to pay the IRS. This depends on the legal structure of your business.

How does the IRS determine your OIC?

The IRS then subtracts your allowable living expenses from your income to assess your ability to pay. This amount, your monthly disposable income, will be used to determine the offer amount for your OIC.

How much is the IRS offering in compromise 2020?

In 2020, the IRS approved 17,890 offers in compromise with a total value of $289.4 million ( source ). Divide $289.4 million by 17,890, and, presto, you get an average offer in compromise of $16,176. Of course, that number is meaningless. The real question is, “how much will the IRS settle for in my case?”.

What is an OIC payment?

Unfortunately, not everyone with tax debt qualifies for the program. In a nutshell, the OIC is a settlement or agreement between you and the IRS. The IRS is like any other creditor.

What is the acceptance rate for tax relief?

Professional tax relief firms often have acceptance rates of 90% and higher. This is because they only submit applications when they know the taxpayer meets the requirements and they know the IRS is likely to say yes. The best tax relief companies have tax lawyers and enrolled agents on staff, provide a money-back guarantee and charge competitive rates. Using a professional tax relief company could help you save time and money on pointless applications.

What is IRS offer amount?

The offer amount also includes what the IRS will receive in monthly payments over a certain period of time. The amount of time depends on several factors, including how long the IRS has to collect and the payment method you’re using to pay the offer amount.

What is it called when you write off all your taxes?

The IRS does have the authority to write off all or some of your tax debt and settle with you for less than you owe. This is called an offer in compromise, or OIC.

Do you have to pay the OIC amount?

This is called the “offer amount.” This amount often largely depends on the value of your assets. People who have built up equity in their home or 401 (k) may have to pay their “net equity” in these assets to the IRS as part of their offer amount.

Is hardship status better than payment plan?

For many people, a payment plan or hardship status is likely a better option.

Can you get an OIC if you don't have money to pay?

To qualify for an OIC based on “doubt as to collectability” (that’s IRS speak for, “You owe, but you don’t have the money to pay.”), you have to prove to the IRS that it can’t collect all the taxes you owe before its time runs out.

IRC Section and Treas. Regulation

- IRC Section 61explains that all amounts from any source are included in gross income unless a specific exception exists. For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury. IRC Section 104explains that gross income does not include damages received on account of personal phys…

Resources

- CC PMTA 2009-035 – October 22, 2008PDFIncome and Employment Tax Consequences and Proper Reporting of Employment-Related Judgments and Settlements Publication 4345, Settlements – TaxabilityPDFThis publication will be used to educate taxpayers of tax implications when they receive a settlement check (award) from a class action lawsuit. Rev. Rul. 85-97 - The …

Analysis

- Awards and settlements can be divided into two distinct groups to determine whether the payments are taxable or non-taxable. The first group includes claims relating to physical injuries, and the second group is for claims relating to non-physical injuries. Within these two groups, the claims usually fall into three categories: 1. Actual damages re...

Issue Indicators Or Audit Tips

- Research public sources that would indicate that the taxpayer has been party to suits or claims. Interview the taxpayer to determine whether the taxpayer provided any type of settlement payment to any of their employees (past or present).