Do I have to pay taxes on my insurance settlement?

Once you file an insurance settlement or claim, the money you receive does not tend to be taxable. However, in some cases, this money is subject to taxes. Unfortunately, many people don’t realize they have to pay taxes on their settlement until it is a little too late. The IRS levies taxes based on income alone. If you receive a payment from your insurance, in most cases, you will only receive enough to cover the situation at hand.

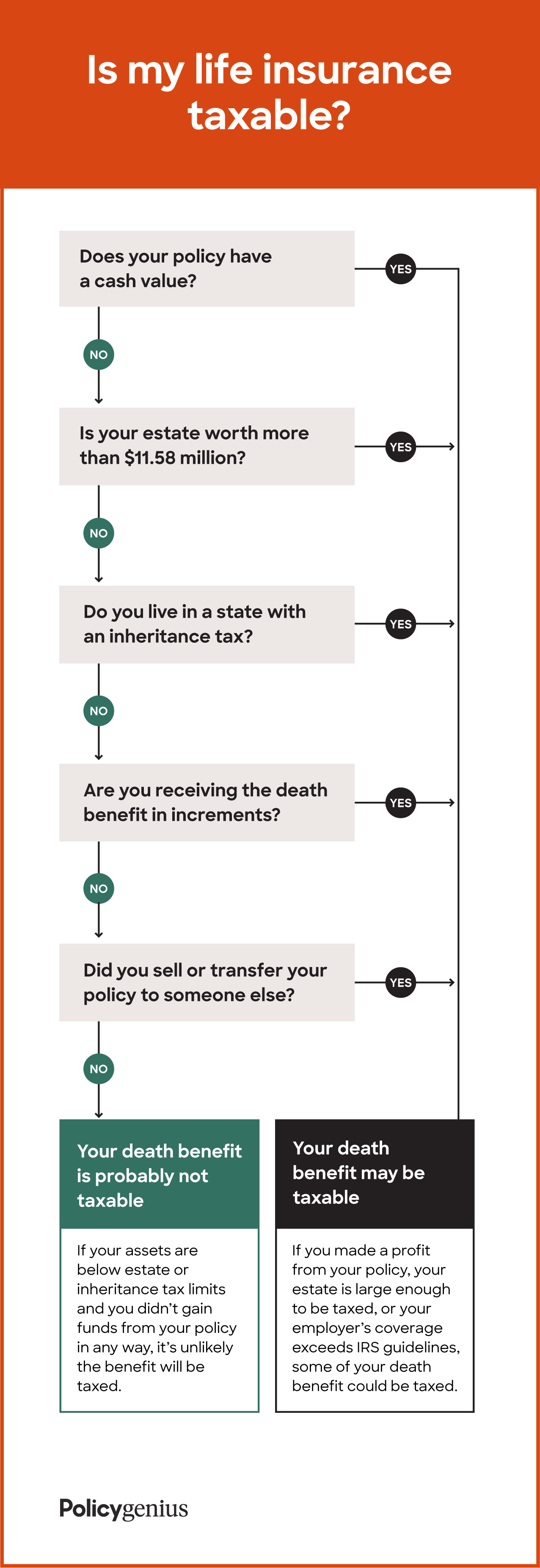

Is a life insurance settlement taxable?

The easy answer is yes, life settlements are taxable to the extent you make a profit. What’s tricky about life settlement taxation, though, is that “profit” can mean different things according to the IRS.

Do beneficiaries pay taxes on life insurance?

The short answer is no, not usually. Beneficiaries generally don’t pay taxes on the proceeds from life insurance. Since beneficiaries don’t have to report the payout as income, it is a tax-free lump sum that they can use freely. However, there are a few aspects to life insurance that won’t get past the tax man.

When are life insurance proceeds taxable?

Whenever you provide life insurance proceeds as a beneficiary in an insured person’s death, these funds are not taxable in your net income, and it is not necessary to report them.Nonetheless, any interest received is taxable. You ought to report any interest received as taxable.

How much tax do you pay on life insurance payout?

Is a life insurance payout taxable? One of the perks of a life insurance policy is that the death benefit is typically tax-free. Beneficiaries generally don't have to report the payout as income, making it a tax-free lump sum that they can use freely.

Do you have to pay taxes on life insurance lump sum?

Life insurance death proceeds are not taxable with respect to income tax as long as the proceeds are paid out entirely as a lump-sum, one-time payment. However, if your beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit.

How do I avoid tax on life insurance proceeds?

If you want your life insurance proceeds to avoid federal taxation, you'll need to transfer ownership of your policy to another person or entity.

Is life insurance considered inheritance?

Life insurance is not considered to be taxable income in the way that an inheritance can be taxed. While there are ways to avoid inheritance tax (such as through a trust), these taxes can be considerable if your estate is large. By using life insurance instead, the death benefit can go entirely to your family members.

Do you have to pay taxes on money received as a beneficiary?

Beneficiaries generally don't have to pay income tax on money or other property they inherit, with the common exception of money withdrawn from an inherited retirement account (IRA or 401(k) plan). The good news for people who inherit money or other property is that they usually don't have to pay income tax on it.

When should you cash out a whole life insurance policy?

Whole life insurance policies are the best option for some people, especially those who will always have dependents due to disabilities and the like. But if you're paying for an expensive policy you don't really need, cashing out may be the best option, even if you have to pay fees and taxes.

What do you do with a life insurance payout?

You received a life insurance benefit: 8 ways to use it wiselyFirst move: Wait.Option 1: Pay off debt.Option 2: Create an emergency fund.Option 3: Purchase an annuity.Option 4: Collect installments.Option 5: Invest for growth.Option 6: Children's education.Option 7: A combination approach.More items...•

Do you have to file a final tax return for a deceased person?

In general, the final individual income tax return of a decedent is prepared and filed in the same manner as when they were alive. All income up to the date of death must be reported and all credits and deductions to which the decedent is entitled may be claimed.

When should you cash out a whole life insurance policy?

Whole life insurance policies are the best option for some people, especially those who will always have dependents due to disabilities and the like. But if you're paying for an expensive policy you don't really need, cashing out may be the best option, even if you have to pay fees and taxes.

What is the general rule for taxation of personal life insurance?

What is the general rule for taxation of personal life insurance policy proceeds? Generally, beneficiaries receive life insurance proceeds tax-free, if received in a lump-sum; however, proceeds from life insurance policies that result from a transfer of value, or were sold to another party, may be subject to taxation.

Are Life Insurance Premiums Taxable?

The life insurance premiums you pay are not taxable. They are also not deductible on your tax return.

Do You Pay Inheritance Tax on Life Insurance?

There is no inheritance tax on life insurance. Life insurance death benefits are paid tax-free to your life insurance beneficiaries.

Is There a Penalty for Cashing Out Life Insurance?

If you surrender a cash value life insurance policy, the only “penalty” is that you may have to pay a surrender fee. The life insurance company wil...

When are life insurance proceeds tax-free?

Generally, your beneficiaries can dodge taxes in these situations.

Are life insurance premiums tax-deductible?

Unfortunately premiums aren’t tax-free, even if you’re paying for an individual policy. You also can’t use a Flexible Spending Account (FSA) or Hea...

When is life insurance taxable?

With so much riding on your life insurance, speak with a licensed accountant if you’re still unsure about the tax implications of your specific pol...

What is the unlimited marital deduction?

The unlimited marital deduction is a provision in the federal Estate and Gift Tax Law that allows you to pass any amount of assets to your spouse d...

What forms do you use to file taxes for a lawsuit?

If you do receive taxable payment from a lawsuit, you'll likely receive a 1099 form to use when filing your taxes. Common taxable payouts from lawsuits include: Punitive damages. Lost wages. Pain and suffering (unless caused by a physical injury) Emotional distress.

Why are insurance claims not taxed?

One of the most common reasons you receive money from an insurance claim is to pay for the repair or replacement of a damaged piece of property.

When does the FSA expire?

But money you put into an FSA generally expires at the end of each year, so you should only put in as much as you think you will spend in a given year.

Is insurance settlement taxed in a lawsuit?

Just like a normal insurance settlement, compensation for medical bills and repair of property are not taxed in a lawsuit.

Do you have to pay taxes if you get hit by an auto accident?

For example, if someone hits you in an auto accident, you wouldn't be taxed for a payment you receive for your medical bills. However, if the judge also awards you punitive damages, you would have to pay tax on those. If you do receive taxable payment from a lawsuit, you'll likely receive a 1099 form to use when filing your taxes.

Do you get a 1099 form if you have insurance?

If you do have to pay taxes on an insurance claim, you'll receive a 1099 form to help you file.

Is life insurance income taxed?

A life insurance payout — the kind that's distributed after the insured person dies — isn't taxed.

What is the Goodman Triangle?

Life insurance beneficiaries are usually exempt from inheritance taxes —but there is an exception called the Goodman Triangle that may prevent them from receiving the full death benefit.

What happens if you cancel your life insurance policy?

If you decide to cancel your life insurance policy before it matures, you’re eligible to gain access to your accrued cash value minus any surrender fees. This is called a “life insurance surrender,” and as long as your settlement amount is less than the total you paid in premiums, your surrender payout is tax-free.

How to avoid estate tax?

To avoid this tax, consider setting up an irrevocable life insurance trust (ILIT). It will stop the proceeds from your policy from being counted as part of your estate. Just keep in mind that if you transfer the policy less than three years before your death, it might still be subject to the estate tax.

What is an accelerated death benefit rider?

Many life insurance policies offer an accelerated death benefit rider, which allows you to access part of your death benefit while you’re alive if you’re diagnosed with a chronic or terminal illness.

How long before death can you transfer a life insurance policy?

Just keep in mind that if you transfer the policy less than three years before your death, it might still be subject to the estate tax. Note that the IRS offers an unlimited marital deduction that allows you to transfer unlimited assets to your spouse, free of any estate or gift taxes.

How much money do you owe if you cancel a life insurance policy?

If you cancel your policy, you’ll likely owe taxes on the $30,000 you’ve earned.

What is cash value gain?

Cash value gains. If you choose a whole or universal life insurance policy, it builds cash value over time. The cash value gains are not subject to any taxation unless the policy is surrendered or transferred to another owner — a scenario referred to as a life insurance settlement.

How to remove life insurance from taxable estate?

Using Life Insurance Trusts to Avoid Taxation. A second way to remove life insurance proceeds from your taxable estate is to create an irrevocable life insurance trust (ILIT). To complete an ownership transfer, you cannot be the trustee of the trust and you may not retain any rights to revoke the trust.

How to transfer insurance policy?

Here are a few guidelines to remember when considering an ownership transfer: 1 Choose a competent adult/entity to be the new owner (it may be the policy beneficiary), then call your insurance company for the proper assignment, or transfer of ownership, forms. 2 New owners must pay the premiums on the policy. However, you can gift up to $15,000 per person in 2020, so the recipient could use some of this gift to pay premiums. 4 3 You will give up all rights to make changes to this policy in the future. However, if a child, family member, or friend is named the new owner, changes can be made by the new owner at your request. 4 Because ownership transfer is an irrevocable event, beware of divorce situations when planning to name the new owner. 5 Obtain written confirmation from your insurance company as proof of the ownership change.

What happens if you get a death benefit of $500,000?

If the death benefit is $500,000, for example, but it earns 10% interest for one year before being paid out, the beneficiary will owe taxes on the $50,000 growth. According to the IRS, if the life insurance policy was transferred to you for cash or other assets, the amount that you exclude as gross income when you file taxes is limited to ...

What is an apportionment clause in a will?

A will can include an "apportionment clause” that leads to tax liabilities for the beneficiary. The clause may state, for instance, that if there are any estate taxes due, they will be paid proportionally by the beneficiaries who receive the assets from the benefactor. Under this circumstance, there would be an estate tax due, but not an income tax. It is possible that some income tax may be due when the life insurance company pays out the proceeds of the policy to the beneficiary over an extended period of time. The face amount of the policy, however, is received income tax-free. The law also requires the insurance company to pay interest to the beneficiary from the date of death until they pay out the proceeds.

What happens when you transfer a life insurance policy?

In transferring the policy, the original owner must forfeit any legal rights to change beneficiaries, borrow against the policy, surrender, or cancel the policy, or select beneficiary payment options. Furthermore, the original owner must not pay the premiums to keep the policy in force.

What is a poor decision that investors seem to frequently make?

One poor decision that investors seem to frequently make is to name "payable to my estate" as the beneficiary of a contractual agreement, such as an IRA account, an annuity, or a life insurance policy.

Can you overpay for life insurance?

According to the IRS, if the life insurance policy was transferred to you for cash or other assets, the amount that you exclude as gross income when you file taxes is limited to the sum of the consideration you paid, any additional premiums you paid, and certain other amounts—in other words, you can't overpay for a policy as a way to cut your taxable income. 1

Do you have to pay tax on a cash surrender value?

The cash surrender value is the cash you have leftover after the fees are taken out when you cancel a life insurance policy. It is also important to know that not all life insurance policies provide a cash value, and this is something you can find out by checking the type of policy you currently have. The short and most simple answer to this question is yes. Although, the better question would be: when is the cash surrender value taxable?

What is capital gains tax on life insurance?

One of the first questions that come to mind for those choosing a life settlement to sell an insurance policy is likely “What is a capital gains tax?” Capital gains are the profits from the sale of an asset (life insurance is considered an asset), meaning that the profit you make from selling your life insurance policy would be taxed. How much you are taxed depends on how long you hold onto this asset.

What is the long term capital gains tax rate?

Long-term capital gains tax is a tax on profits from the sale of an asset held for more than a year (this tax rate is 0%, 15%, or 20% depending on your taxable income and filing status).

How is cash surrender value determined?

The good news is that a cash surrender value is determined by deducting any fees you owe the insurer from your policy’s cash value. Therefore, if you do not have any fees left when you perform a cash surrender, then you will be left with more cash after being taxed.

What are the two types of capital gains tax?

There are two main types of capital gains tax, short-term and long-term.

Is cash surrendered insurance taxed?

Any money that you receive from a cash surrender that is over the policy’s cost basis can be taxed as income. The cost basis (the sum of all your insurance premium payments) is not the only item that can be taxed in a cash surrender. Dividends earned or interest can be taxed as well, this will vary depending on your specific policy.

Can you tax life insurance money?

In a typical life insurance payout, the IRS is not allowed to tax the money given to a beneficiary. However, if you choose to sell your life insurance policy, the IRS no longer views that money under the same circumstances. As a rule of thumb, as the cash value grows inside the policy, it cannot be taxed on the interest or dividends. Although, as mentioned above, this is only the case if the money stays inside the policy. A final piece of advice, it is always recommended that you check with your current financial advisor as well to get their opinion on your options.

What is the purpose of IRC 104?

IRC Section 104 provides an exclusion from taxable income with respect to lawsuits, settlements and awards. However, the facts and circumstances surrounding each settlement payment must be considered to determine the purpose for which the money was received because not all amounts received from a settlement are exempt from taxes.

What is the tax rule for settlements?

Tax Implications of Settlements and Judgments. The general rule of taxability for amounts received from settlement of lawsuits and other legal remedies is Internal Revenue Code (IRC) Section 61 that states all income is taxable from whatever source derived, unless exempted by another section of the code. IRC Section 104 provides an exclusion ...

What is employment related lawsuit?

Employment-related lawsuits may arise from wrongful discharge or failure to honor contract obligations. Damages received to compensate for economic loss, for example lost wages, business income and benefits, are not excludable form gross income unless a personal physical injury caused such loss.

What is a 1.104-1 C?

Section 1.104-1 (c) defines damages received on account of personal physical injuries or physical sickness to mean an amount received (other than workers' compensation) through prosecution of a legal suit or action, or through a settlement agreement entered into in lieu of prosecution.

What is an interview with a taxpayer?

Interview the taxpayer to determine whether the taxpayer provided any type of settlement payment to any of their employees (past or present).

What is the exception to gross income?

For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid on account of physical injury.

What is Publication 4345?

Publication 4345, Settlements – Taxability PDF This publication will be used to educate taxpayers of tax implications when they receive a settlement check (award) from a class action lawsuit.