Can a debt settlement damage my credit score?

The debt settlement process typically hurts your credit scores in two phases: During the negotiation process, and after your accounts are settled and closed. Damage to credit scores begins as you withhold payments to creditors, and missed payments begin appearing on your credit reports.

Will settling a debt affect my credit score?

Settlement of your credit card debt will impact your credit score—but with persistence, determination, and a little bit of luck, you’ll be able to raise your score to new heights. Settling debt for less than the total amount owed is better for your credit than ignoring your debt, but it’s worth taking a closer look at bankruptcy if you can’t afford to settle your debt.

How does a loan settlement impact my CIBIL score?

When a loan is termed settled, it is viewed as a negative credit behaviour and the borrower’s credit score drops by 75-100 points. The CIBIL holds this record for over 7 years. So, if the borrower has to take a loan during that period, it is likely that the lenders will be vary of the borrower and try and stay away from giving the borrower ...

How to improve your credit score after a loan settlement?

- Pay cash. Cash is king. ...

- Use the “3 day rule”. This rule applies to major purchases — things that cost hundreds or thousands of dollars. ...

- Question everything. Do you really need that latte on your way to work each morning or can you survive with a fresh-brewed cup of coffee at home before you leave ...

- Start saving. ...

- Do it now. ...

How many points does a settlement affect credit score?

Debt settlement practices can knock down your credit score by 100 points or more, according to the National Foundation for Credit Counseling. And that black mark can linger for up to seven years.

Do settlements hurt your credit?

While settling an account won't damage your credit as much as not paying at all, a status of "settled" on your credit report is still considered negative. Settling a debt means you have negotiated with the lender and they have agreed to accept less than the full amount owed as final payment on the account.

Is it better to settle or pay in full?

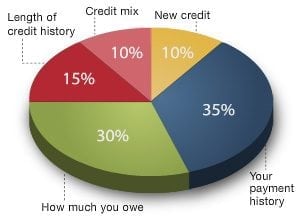

Generally speaking, having a debt listed as paid in full on your credit reports sends a more positive signal to lenders than having one or more debts listed as settled. Payment history accounts for 35% of your FICO credit score, so the fewer negative marks you have—such as late payments or settled debts—the better.

How long does it take for credit score to go up after settlement?

between 6 and 24 monthsHowever, a debt settlement does not mean that your life needs to stop. You can begin rebuilding your credit score little by little. Your credit score will usually take between 6 and 24 months to improve. It depends on how poor your credit score is after debt settlement.

How do I raise my credit score after a settlement?

How to Improve CIBIL Score After Loan Settlement?Build a Good Credit Repayment History. ... Clear off Pending Dues. ... Manage Credit Cards Better. ... Apply for a Secured Card. ... Credit Utilisation. ... Do Not Raise Frequent Loan Queries. ... Apply for a Secured Credit.

How do I get a settled account off my credit report?

Review Your Debt Settlement OptionsDispute Any Inconsistencies to a Credit Bureau.Send a Goodwill Letter to the Lender.Wait for the Settled Account to Drop Off.

Can I get loan after settlement?

The bank or lender takes a look at the borrower's CIBIL score before offering him a loan and if the past record shows any settlement or non-payment, his loan is likely to get rejected.

Can I get a mortgage after debt settlement?

Most lenders won't want to work with you immediately after a debt settlement. Settlements indicate difficulty with managing financial obligations, and lenders want as little risk as possible. However, you can save enough money and buy a new home in a few years with the right planning.

How long does a settled account stay on your credit report?

seven yearsA settled account remains on your credit report for seven years from its original delinquency date. If you settled the debt five years ago, there's almost certainly some time remaining before the seven-year period is reached. Your credit report represents the history of how you've managed your accounts.

Why did my credit score drop 40 points after paying off debt?

Credit utilization — the portion of your credit limits that you are currently using — is a significant factor in credit scores. It is one reason your credit score could drop a little after you pay off debt, particularly if you close the account.

How can I raise my credit score 100 points overnight?

How To Raise Your Credit Score by 100 Points OvernightPay Off Your Delinquent Balances.Keep Credit Balances Below 30%Pay Your Bills on Time.Dispute Errors on Your Credit Report.Set up a Credit Monitoring Account.Report Rent and Utility Payments.Open a Secure Credit Card.Become an Authorized User.More items...•

How does a settlement show on your credit report?

When you settle an account, its balance is brought to zero, but your credit report will show the account was settled for less than the full amount. Settling an account instead of paying it in full is considered negative because the creditor agreed to take a loss in accepting less than what it was owed.

How long do settlements stay on credit report?

seven yearsA settled account remains on your credit report for seven years from its original delinquency date. If you settled the debt five years ago, there's almost certainly some time remaining before the seven-year period is reached. Your credit report represents the history of how you've managed your accounts.

Is it worth it to settle debt?

The short answer: Yes, debt settlement is worth it if all of your debt is with a single creditor, and you're able to offer a lump sum of money to settle your debt. If you're carrying a high credit card balance or a lot of debt, a settlement offer may be the right option for you.

Can I get loan after settlement?

The banks and lenders mainly look for the borrower's past repayments before considering offering him a loan. And if the borrower has the settlement in his credit report, the banks and lenders will reject the loan.

How long does a debt settlement stay on your credit report?

A debt settlement remains on your credit report for seven years. 3 . As with all debts, larger balances have a proportionately larger impact on your credit score. If you are settling small accounts—particularly if you are current on other, bigger loans —then the impact of a debt settlement may be negligible.

What is a debt settlement plan?

A debt settlement plan—in which you agree to pay back a portion of your outstanding debt —modifies or negates the original credit agreement. 1 When the lender closes the account due to a modification to the original contract (as it often does, after the settlement's complete), your score gets dinged.

What Sort of Debt Should I Settle?

Since most creditors are unwilling to settle debts that are current and serviced with timely payments, you're better off trying to work out a deal for older, seriously past-due debt, perhaps something that's already been turned over to a collections department. It sounds counter-intuitive, but generally, your credit score drops less as you become more delinquent in your payments .

How to negotiate a debt settlement?

You can negotiate a debt settlement arrangement directly with your lender or seek the help of a debt settlement company. Through either route, you make an agreement to pay back just a portion of the outstanding debt. If the lender agrees, your debt is reported to the credit bureaus as "paid-settled.".

What is a credit report?

As you know, your credit report is a snapshot of your financial past and present. It displays the history of each of your accounts and loans, including the original terms of the loan agreement, the size of your outstanding balance compared with your credit limit, and whether payments were timely or skipped.

Is debt settlement good for credit?

Facing past due debt can be scary, and you may feel like doing anything you can to get out of it. In this situation, a debt settlement arrangement seems like an attractive option. From the lender’s perspective, arranging for payment of some, but not all, of the outstanding debt can be better than receiving none. For you, a debt settlement packs a punch against your credit report, but it can let you resolve things and rebuild.

Is it better to settle debt or receive none?

From the lender’s perspective, arranging for payment of some, but not all, of the outstanding debt can be better than receiving none. For you, a debt settlement packs a punch against your credit report, but it can let you resolve things and rebuild. Consider the opportunity cost of not settling your debt.

How does a debt settlement affect your credit score?

A debt settlemen t can decrease your credit score by 100 points or more. The amount it drops will depend on your credit history, types of debt, current credit score, and current credit activity. It will also depend on whether the lender reported the settled debt as partially paid or paid in full. When you’re negotiating a debt settlement, ask the lender if they will report the account as “paid in full” as part of the settlement terms. Having an account reported as paid in full, won’t harm your credit score. But if it’s reported as “partially paid,” it will lower your score.

How long does a debt settlement stay on your credit report?

When you apply for new credit, lenders will see that you did not pay that previous balance in full. This will tell them that you might be a risky borrower to lend to. This information stays on your credit report for seven years.

How does debt settlement work?

Debt settlement is a repayment method where you negotiate with a creditor to pay less than you owe to close your account and stop collection activity. You or a debt settlement company can negotiate payment options to close your account. You can use the money you have to settle the debt in one lump sum or work out a plan to make monthly payments. Debt settlement is often used with credit card debt. The part of the debt you don’t pay is forgiven debt. If a lender forgives $600 or more it’s considered “canceled debt” and taxable income by the IRS.

What is the difference between bankruptcy and debt settlement?

An alternative to debt settlement is bankruptcy. The biggest difference between the two is that debt settlement doesn’t require you to give up assets. Although you can often make agreements to keep your house and car during bankruptcy, assets can be sold to pay off debts through a court order. When you settle your debt with a creditor, you’re free to decide what to do with your assets, not the court. One advantage of bankruptcy over debt settlement is that filing bankruptcy stops debt collectors from calling. Creditors can still hound you during debt settlement negotiations.

What happens if you file Chapter 7 bankruptcy?

If you file a Chapter 7 bankruptcy, your unsecured debts and certain secured debts can be discharged. This means you would no longer owe the debt and you’ll have a $0.00 balance. If you don’t have the money to pay the unsecured debt, you don’t pay your debt. The debt still goes away.

What to ask a company about a debt settlement?

Ask if they have company policies governing debt settlement and if they’d be willing to settle the debt for less than the amount owed. Also, ask them if they are willing to report the account as paid in full if a debt sett lement agreement is reached.

How many consumers negotiated a debt settlement between 2007 and 2019?

The CFPB reports that 1 in 13 consumers negotiated a debt settlement between 2007 and 2019. It’s not an unusual practice, and lenders are prepared. Here are some basic best practices to follow before and during negotiations:

How much debt settlement dings your credit score?

Bottom line: How much debt settlement dings your credit score depends on the current state of your finances and the amount of debt you’re settling.

How much does debt affect your credit score?

The amount of debt you owe determines 30% of your FICO score. Part of that 30% equation includes your credit utilization ratio. If your ratio goes down as a result of debt settlement, it could bump up your credit score. For example, if debt settlement leads to the ratio falling from 20% to 10%, you could see your credit score spike.

What Sort of Debt Should I Settle?

Both unsecured and secured debts can be settled. But not all unsecured and secured debts are eligible.

What happens when you settle a debt?

When you settle debts, creditors agree to accept partial payment for your debts rather than possibly receiving nothing at all. In turn, the creditors mark your debts as being paid off. These debts will appear on your credit report as being “settled,” meaning the accounts have been paid in full, but for less than the total balance.

What is the most important factor in determining your credit score?

Payment history — specifically making timely payments on credit card accounts, loans and other lending products — ranks as the most important factor in calculating your credit score. If you’re looking at debt settlement, your payment history and your credit score have undoubtedly been battered already.

What percentage of credit score is payment history?

At FICO, the biggest producer of credit scores in the U.S., payment history makes up 35% of a FICO score. It’s the number one factor among the five factors that FICO considers.

How much does debt relief cost?

Debt relief companies typically earn a fee of 15% to 25% of the full amount of debt that’s owed (rather than the settlement amount).

How to settle credit card debt?

The process of debt settlement gives you the option to negotiate with credit card issuers to settle debt with a lump sum payment that is less than the total amount due on your account. Note that you may have to pay taxes on the forgiven debt of the settled debt if it’s over $600. (The forgiven debt is the amount of the original total debt that you didn’t pay.) However, if you don’t have the funds available to make a lump sum payment or you don’t want to mess with the tax consequences, you have other options available to settle credit card debt.

Why does my credit score drop?

Because the credit card company takes less money than is owed , your credit score will be temporarily lowered because you won’t pay your debt in full. The amount that your credit score will drop will depend on your personal financial situation.

How Long Will Negative Information Be On My Credit Report?

When you settle a debt for less than the total amount owed, that status will likely remain on your credit report for 7 years. That’s also how long a completed Chapter 13 bankruptcy stays on your report. A Chapter 13 bankruptcy lets you make affordable payments on your debt over either a 3 or 5 year period. If the Chapter 13 case is not completed to discharge, it will stay on your report for 10 years. A Chapter 7 bankruptcy also stays on your credit report for 10 years, but this process allows your debt from credit cards and other eligible unsecured debts to be discharged without having to make payments on that debt. When bankruptcy debt is discharged, you’re officially no longer responsible for that debt anymore. If your debt is more than you can afford to pay, you could become debt-free after filing a successful bankruptcy case.

What to do if you don't have the funds to pay your credit card debt?

However, if you don’t have the funds available to make a lump sum payment or you don’t want to mess with the tax consequences, you have other options available to settle credit card debt. To explore options other than debt settlement, consider credit counseling.

How long does bankruptcy stay on credit report?

A Chapter 7 bankruptcy also stays on your credit report for 10 years, but this process allows your debt from credit cards and other eligible unsecured debts to be discharged without having to make payments on that debt. When bankruptcy debt is discharged, you’re officially no longer responsible for that debt anymore.

How does your credit score determine your credit score?

Your credit score is determined by an analysis of your past payments, the total amount owed, credit inquiries, how long you’ve had credit, and new credit that has been recently obtained. Since your total amount owed goes down after debt settlement or bankruptcy, your credit score could improve quickly over time.

What can a credit counselor do?

You can talk to them about working with a debt settlement company, entering into a debt management plan, pursuing debt consolidation, and filing for bankruptcy. They will provide you with personalized guidance after learning about your unique circumstances.

How many points does a debt settlement decrease your credit score?

According to debt.org, when going through debt settlement you can expect to see your credit score decrease by at least 100-125 points.

What percentage of credit score is affected by not making payments?

Payment history makes up 35 percent of your credit score total. When you stop making payments, your credit score drops. Another consequence of not making payments is the effect it has on your credit utilization . Credit utilization makes up 30 percent of your credit score total, and is determined by looking at your ratio of debt to available credit.

What happens if you don't pay your debt?

Another consequence of not making payments is the effect it has on your credit utilization . Credit utilization makes up 30 percent of your credit score total, and is determined by looking at your ratio of debt to available credit. Ideal credit utilization is between 10 and 30 percent of your total available credit. However, if you are carrying an excessive balance due to non-payment and late fees, your credit utilization will be well over that. According to debt.org, when going through debt settlement you can expect to see your credit score decrease by at least 100-125 points.

How to reduce the blow of debt settlement?

How to lessen the blow of debt settlement. Debt settlement is a difficult and risky process, but there are things you can do to soften the blow to your credit score. To begin with, you can try to take care of smaller debts on your own or through a debt management organization. Focus your debt settlement on older debt that is simply out ...

What happens when you stop paying your debt settlement?

Payment history makes up 35 percent of your credit score total. When you stop making payments, your credit score drops.

How long do delinquent payments stay on credit?

Delinquencies stay on your credit report for seven years from the first date a payment was missed. This mark on your credit report will make it difficult for you to get a loan or credit in the future—settling debt won’t hide the record of missed payments.

How long does it take to settle a credit card debt?

This way you can avoid a charge-off, which typically occurs after 180 days of non-payment.

How much does a debt settlement hurt your credit score?

A debt settlement can hurt your credit score. A debt settlement can reduce your credit score by as much as 125 points. This is a big hit to absorb all at once, and may be difficult to recover from quickly in the event you need a high credit score.

How long does a debt settlement last?

Credit history. On your credit report, a debt settlement will appear for 7 years from the original delinquency date of the debt. Other lenders will look at that notation negatively, and it may prevent them from lending money to you in the future. A lower credit score can make it difficult or impossible to borrow money, result in an inability to rent an apartment, higher car insurance premiums, and even cause denial for job opportunities.

What is debt settlement?

A debt settlement is an agreement between a borrower and a lender which allows borrowers to repay a lender less than the amount they owe, and the creditor considers the debt paid off. This might sound like a good way to pay off all your debts and quickly improve your financial situation, but it can…. A debt settlement is an agreement between ...

What should a settlement agreement tell you?

The agreement should tell you how much the original debt is, how much the creditor is willing to accept to settle the account, and how it will be reported to the credit bureaus. Other options. If you decide a debt settlement isn’t your best option for getting out of debt, you have about four other choices:

Is debt settlement bad for your credit?

Dangers of debt settlements. Consumers may be able to get out of debt more quickly if they use a debt settlement, but they have very bad consequences. For example: a debt settlement is reported to the credit bureaus, appears on your credit report, results in a huge drop of your FICO credit score, and can affect your tax situation.

Does a debt settlement result in a large tax bill?

Taxes. A debt settlement can result in a large tax bill when you file your income taxes, because in many situations, the IRS treats the amount of the forgiven debt as income and you will be required to pay income tax on the amount settled.

Can you remain delinquent on your credit card?

You can remain delinquent on your accounts, paying when you can, and hope your situation improves so you can pay off the debts at some point.

How does debt settlement affect credit?

Debt settlement affects your credit for up to 7 years, lowering your credit score by as much as 100 points initially and then having less of an effect as time goes on. The events that typically lead up to debt settlement will affect your credit score, too. Most creditors will not consider debt settlement until the debt holder is severely delinquent on payment or already in default. Missing payments and then defaulting, or charging-off, on debt can cause your credit score to drop by as much as 110 points even before debt settlement negotiations begin.

How many points does a debt settlement drop your credit score?

Missing payments and then defaulting, or charging-off, on debt can cause your credit score to drop by as much as 110 points even before debt settlement negotiations begin. In other words, the extent to which debt settlement will impact your credit standing depends in large part on your current payment status:

What happens if you hire a debt settlement company?

All that a debt settlement company will do if you hire them when delinquent is simply ask you for a payment and then hold onto it until you default – ruining your credit in the process. Only then will they negotiate a deal with your creditor or the debt collector that assumed your debt once the original lender wrote it off its books.

What happens if you are more than 180 days behind on your credit card payments?

If you have fallen more than 180 days behind on your credit card payments, your account has already been classified as being in default on your major credit reports. By that time, you’ve already suffered a lot of credit-score damage, so you won’t risk much by pursuing debt settlement.

What to do when you have credit card debt?

The best thing that you can do when faced with significant amounts of credit card debt is avoid missing any monthly payments. That doesn’t mean you have to pay your full balance right away, but rather that you must submit at least the minimum payment required by the due date each month.

Why is it worth submitting a payment?

At this point, you might be asking yourself why it’s even worth submitting a payment at all. There are two reasons: 1) It’s the right thing to do; and 2) It eliminates the threat of a lawsuit.

Can you settle debt if your credit is damaged?

At the end of the day, you can only rely on debt settlement as a solution to your financial woes if your credit has already been destroyed. If that’s not the case, you should consider other options that might not only minimize the credit score damage that can result from significant debt, but that will also reduce your chances of being sued for amounts owed.