Writing a Debt Settlement Offer Letter (8 Best Samples)

- Write your address information as the header of the letter. Provide your personal information and account number on the header of the debt settlement ...

- Outline the amount you wish to pay as settlement.

- Give a reason why you are unable to settle.

- Write the account you wish to pay on and the date.

- Conclude the letter.

Should I write a debt settlement offer letter?

What Your Settlement Letter Should Include

- The letter should be on company letterhead, regardless of whether you’re dealing with a collection agency or the original creditor. ...

- The letter should include a date so you know when the settlement offer was made.

- Make sure the correct account number is listed on the debt settlement letter. ...

How much should I offer to settle a debt?

When entering negotiations, make sure to:

- Know your rights. You can’t be harassed, lied to, threatened, or even spoken to out of business hours.

- Consider your debt. What type of debt do you owe? This will help in understanding what you could ask for.

- Speak calmly and logically.

- Make your offer. Debt collectors may settle for around 50% of your debt. ...

What percentage should I offer to settle debt?

- Credit Cards, Department Store Cards 40%

- Citibank Accounts 65%

- Discover Accounts 65%

- Cell Phones (Collections over $750) 50%

- Apartment Lease Re-letting Fees 40%

- Medical Debts, Collections 50%

- Judgments/Garnishments, Repossessions 80%

- Pay Day Loans, Signature Loans 40%

- Collection Balance Greater than $750 Settlements 40%

How to negotiate a debt settlement?

If you want to make a proposal to repay this debt, here are some considerations:

- Be honest with yourself about how much you can pay each month. ...

- Write down a summary of your monthly take-home pay and all your monthly expenses (including the amount you want to repay each month and other debt payments). ...

- Decide on the total amount you are willing to pay to settle the entire debt. This could be a lump sum or a number of payments. ...

How do I write a debt settlement letter?

Write a debt settlement letter to your creditor. Explain your current situation and how much you can pay. Also, provide them with a clear description of what you expect in return, such as removal of missed payments or the account shown as paid in full on your report.

What percentage should I offer to settle a debt?

When you're negotiating with a creditor, try to settle your debt for 50% or less, which is a realistic goal based on creditors' history with debt settlement. If you owe $3,000, shoot for a settlement of up to $1,500.

How do I make an offer on a debt settlement?

A 6-step DIY debt settlement planAssess your situation. ... Research your creditors. ... Start a settlement fund. ... Make the creditor an offer. ... Review a written settlement agreement. ... Pay the agreed-upon settlement amount.

What should I offer a debt collector for a settlement?

Start by offering cents on every dollar you owe, say around 20 to 25 cents, then 50 cents on every dollar, then 75. The debt collector may still demand to collect the full amount that you owe, but in some cases they may also be willing to take a slightly lower amount that you propose.

What is the 11 word phrase to stop debt collectors?

If you need to take a break, you can use this 11 word phrase to stop debt collectors: “Please cease and desist all calls and contact with me, immediately.” Here is what you should do if you are being contacted by a debt collector.

Will debt collectors settle for 30%?

Lenders typically agree to a debt settlement of between 30% and 80%. Several factors may influence this amount, such as the debt holder's financial situation and available cash on hand.

What is a reasonable full and final settlement offer?

It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

Is it better to settle or pay in full?

Generally speaking, having a debt listed as paid in full on your credit reports sends a more positive signal to lenders than having one or more debts listed as settled. Payment history accounts for 35% of your FICO credit score, so the fewer negative marks you have—such as late payments or settled debts—the better.

Will debt collectors settle for half?

Some want 75%–80% of what you owe. Others will take 50%, while others might settle for one-third or less. Proposing a lump-sum settlement is generally the best option—and the one most collectors will readily agree to—if you can afford it.

Is it worth it to settle debt?

In general, paying off the total amount of debt you owe is a better option for your credit. An account that appears as "paid in full" on your credit report shows potential lenders that you have fulfilled your obligations as agreed, and that you paid the creditor the full amount due.

Can you dispute a debt if it was sold to a collection agency?

Can you dispute a debt if it was sold to a collection agency? Your rights are the same as if you were dealing with the original creditor. If you don't believe you should pay the debt, for example, if a debt is statute barred or prescribed, then you can dispute the debt.

Does Debt Settlement hurt your credit?

Debt settlement can negatively impact your credit score, but it won't hurt you as much as not paying at all. You can rebuild your credit by making all payments on time going forward and limiting balances on revolving accounts.

What percentage should I offer a full and final settlement?

It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

What percentage should I ask a creditor to settle for after a Judgement?

If you decide to try to settle your unsecured debts, aim to pay 50% or less. It might take some time to get to this point, but most unsecured creditors will agree to take around 30% to 50% of the debt. So, start with a lower offer—about 15%—and negotiate from there.

Is it OK to settle a debt?

While settling an account won't damage your credit as much as not paying at all, a status of "settled" on your credit report is still considered negative. Settling a debt means you have negotiated with the lender and they have agreed to accept less than the full amount owed as final payment on the account.

Can I negotiate with debt collectors?

You may have more room to negotiate with a debt collector than you did with the original creditor. It can also help to work through a credit counselor or attorney. Record your agreement. Sometimes, debt collectors and consumers don't remember their conversations the same way.

What should be included in a debt settlement letter?

You should also include all the key information your creditor will need to locate your account on their system, which includes: Your full name used on the account. Your full address.

What is debt settlement?

Debt settlement is something many people consider if they are able to offer a lump sum of money up front – usually less than the total amount owed – in the hope the creditor will agree to this and accept the debt as settled.

How to contact PayPlan?

If you are looking for guidance when dealing with creditors and proposing a debt settlement, our team here at PayPlan can help. Speak to our experts on 0800 280 2816 or use our contact form to get in touch.

What to do if creditor accepts offer?

If the creditor accepts your offer, ensure this is in writing before you send any money to them. Keep this written confirmation safe too in case there is any dispute in the future, so you can offer this as proof of the agreement.

What does it mean when you get your debt removed?

Doing this means your debt can be removed earlier and that you will no longer need to worry about making repayments.

What happens if you settle early on a debt?

It’s important to remember that if you settle early on your debt, this means you are not paying it in full and so it will show as partially settled on your credit report instead of settled. This can affect your ability to obtain credit in the future, as it suggests to future creditors that you may not be able to pay back the full amount borrowed.

When proposing a full and final debt settlement to creditors, it’s important you go about this in the right?

When proposing a full and final debt settlement to creditors, it’s important you go about this in the right way. This means sending a written letter explaining how you wish to settle your debt, how much you are offering to pay and when this can be paid by.

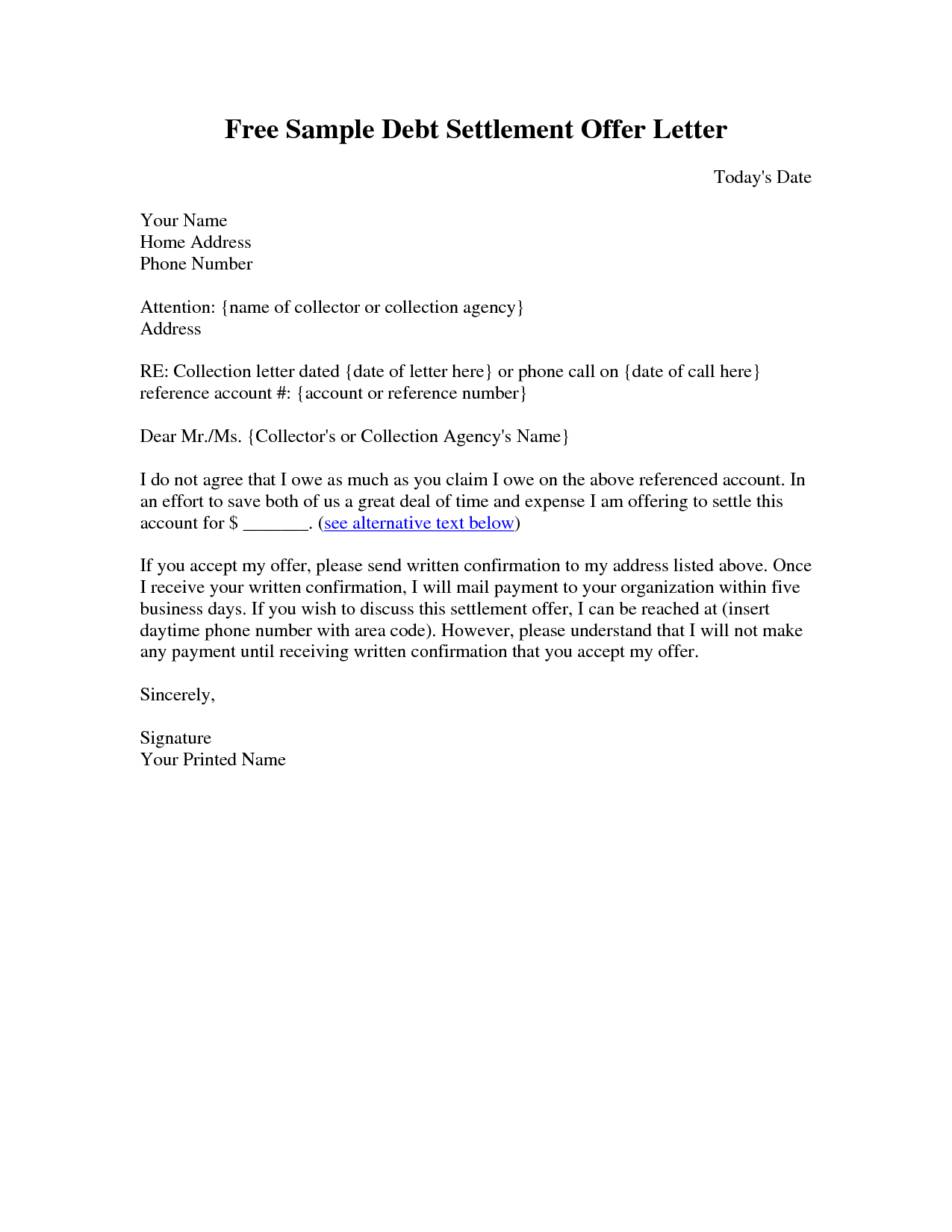

What is a debt settlement offer letter?

A debt settlement offer letter is a written proposal that a debtor or his attorney sends to a creditor or a debt collections agency to offer a specific amount of money to forgive a debt. A creditor may also send a debtor an offer letter. Usually, debt settlement offer letters are sent when a debt is past the due date and has probably been moved to a collection agency, and the debtor is unable to pay all the debt they’ve accumulated.

What information is needed for a debt settlement letter?

Your personal information includes your full legal name, mailing address, and current date.

Why is it beneficial to settle debt?

Settling debt is beneficial to the collector because it implies that they will get a significant part of the total amount owed. As you may already know, the odds of getting an account in collections paid are not good. It is more likely that the debtor will file for bankruptcy and the debt automatically discharged. This means that the debt collector risks getting nothing out of what they are owed. And even if the debtor does not file for bankruptcy, it will still cost a lot of time and money trying to take legal action against the debtor to collect the debt.

Is it bad to settle a debt?

Although settling a debt account is considered negative by many people, it won’t hurt you as much as not paying at all. Suppose you are planning to make a major purchase, for example, buying a home. In that case, you may be required to either settle or clear any outstanding delinquent debts before you can qualify for a loan from any financial lending institution. If paying the debt in full is not an option due to financial constraints, consider settling the account because it is more beneficial to your financial health than letting the debt go delinquent or, worse, to default.

What is the most important part of a debt settlement letter?

One of the most important components of your debt settlement letter is a single number: the amount you decide to offer. You’ll base that number on your assessment of two considerations. Affordability. Never offer more than you can afford to pay.

What is the purpose of the settlement paragraph?

You’ll use this paragraph to present the details of your settlement offer. This will include the dollar amount you’re proposing to pay.

What to do if you can't pay your debt?

If you decide to try to settle your debts, you’ll start the process by writing a debt settlement letter. You’ll use the letter to propose settling the debt for a reduced amount.

What should be the opening paragraph of a letter?

First Paragraph. Your opening paragraph should quickly state the purpose of your letter, which is a proposal to settle the account for less than the full amount. In the next sentence, you’ll explain why you can’t pay the full amount.

What should I say in the last sentence?

In the last sentence, you should provide a reason why you won’t be able to pay the full amount. It should be a circumstance beyond your control. I’ve listed several within the parentheses, but feel free to include whatever situation may be preventing you from making full payment. You don’t need to be long-winded here.

What to do if your proposal is not read?

If that happens, your proposal will never be read, let alone acted upon. You should send a letter to the person you’ve been dealing with at the company. If there’s no specific individual, make a phone call and get the name of a person likely to be in a capacity to work with your proposal.

Can a creditor accept a reduced payment?

If you send a reduced payment without having written confirmation of your settlement proposal from the creditor, they may accept your payment as a partial payment on the full amount owed, then continue efforts to collect the balance.

What is a debt settlement offer letter?

This can be done using a debt settlement offer letter. This is a form that is used when the debtor and creditor want to agree to new terms in settling the outstanding debt. The letter is usually sent by the debtor to the creditor and may offer a lump sum that is not the full amount, but one that is agreeable to the creditor to accept ...

What should a debt settlement letter include?

There are some key details that all debt settlement offer letters should have: The full name used for the credit account. Your full address. Your account numbers or a reference number from the creditor. This information is what your creditor will need to pull up all of the relevant details of your account with them.

How to write a settlement letter?

Make sure your letter has: 1 Header – this should include your full name and address, as well as the date that the letter has been written. 2 Body – this is where you will explain the details of your settlement offer (amount, dates of payments you will make, and how they will be made) and what you are expecting from your creditor. 3 Contact – your contact details, including a current phone, mobile, and e-mail address. 4 Closing – this is where you will sign the letter

Why is it important to have a copy of an offer of acceptance from the creditor?

This is why it is important to have a written copy of an offer of acceptance from the creditor as proof, to stop them from trying to come back and claim the balance afterward.

What percentage of debt should be offered to a creditor?

Typically, an offer of between 30% of the debts outstanding balance should be made to a creditor for them to even consider it. The cre4ditor will normally come back with a counteroffer of 50%.

How long does a partial settlement stay on your credit report?

Negative marks on your credit report, such as a partial debt settlement, can stay on your report for 7 years.

Does settling a debt show up on your credit report?

Be sure to keep this confirmation in a safe place because it is your proof of the agreement should a dispute should arise. Note: Settling a debt early (not paying it in full), will show up on your credit report as a partially settled debt, and not a fully settled one.

How to contact a debt settlement company?

To learn more about debt settlement or to schedule a free consultation, please contact us online or call us today at 888-574-5454.

What is debt settlement?

Debt settlement occurs when a debtor successfully negotiates a payoff amount for less than the total balance owed on a debt. This lower negotiated amount is agreed to by the creditor or collection agency and must be fully documented in writing. The settlement is often paid off in one lump sum, although it can also be paid off over time.

What happens if a creditor accepts a settlement offer?

If the creditor ultimately accepts your offer for debt settlement, make certain that the acceptance is made in writing prior to sending the creditor any amount of money. A written acceptance will serve as confirmation in the event that there are any future disputes.

What does it mean when a debt settlement is negotiated?

It is also important to understand that the nature of a negotiated debt settlement implies that you will have paid less than the full amount of the debt, and that the settled account is likely to be marked on your credit report as “settled,” as opposed to “paid in full.”.

What is the importance of explaining to a creditor?

It is also very important to explain to the creditor the nature of your current circumstances (employment-related, health-related, family-related) and how they financially impact you, your cash flow, your necessary expenses, and your ability to pay the debt in full.

How long does a settlement stay on your credit report?

Accounts marked as “settled” will remain on a credit report for seven years, and often have a detrimental impact on a credit score and profile.

When proposing a full and final settlement offer to a creditor, is it important to explain?

Therefore, when proposing a full and final settlement offer to a creditor, it’s important to be thorough in conveying exactly how much you offer to pay, exactly when you offer to have it paid, and the concessions you want your creditor to grant. It is also very important to explain to the creditor the nature of your current circumstances ...

What is a debt settlement offer letter?

The Debt Settlement Offer Letter is a form that shows a debt is willing to be closed if the parties agree to new terms. Typically, this letter is from the debtor in order to offer a lump sum payment if the creditor is willing to release the burden of the full amount. After the letter is accepted, the parties will enter a debt settlement agreement unless a simple receipt is enough to satisfy the debtor.

What happens after a letter is accepted?

After the letter is accepted, the parties will enter a debt settlement agreement unless a simple receipt is enough to satisfy the debtor.

What Is a Debt Settlement Letter?

If you’re unable or unsure about negotiating a debt settlement over the telephone, negotiating by letter is a reasonable option. It’s not much different negotiating with your creditor by telephone, but it might take longer. There are several ways to prepare a settlement letter, including hiring an attorney to write it for you or going online to download a template to use as a starting point. There are also several sample letters you can look at to get an idea of what your completed letter should look like.

How does debt settlement work?

Luckily, there are many debt relief options. Debt settlement is one of the most advertised and for good reason. It’s often used for credit card debts and allows borrowers with unmanageable debt to pay off one or more debts for less than the full amount. The creditor then forgives the remaining debt. This may sound too good to be true, but it’s not. How well it works for you will depend on your financial situation and whether you choose to hire a debt settlement company to help you or do the debt settlement process yourself. This article will explain how to handle debt settlement on your own and how to write the best debt settlement letter possible.

What is the first step in a debt settlement?

The first step in a debt settlement negotiation with a bank, credit card company, or collection agency is to confirm the debt belongs to you. Some debts pass through multiple collection agencies once they leave the original creditor. During that time, mix-ups can occur or debts can become so old they are past the statute of limitations and legally uncollectible .

How long do you have to be behind on your debt to get a creditor to accept your debt?

To increase your chances of getting a creditor to accept your debt, you need to be at least 90 days behind on your payments with that creditor. And during the negotiation process, you’ll need to continue not making any payments. This will hurt your credit score and the extra fees and interest may increase your overall debt. But it’s easier to convince a creditor that you can’t fully pay off your debt when you haven’t made any payments for several months. Remember, a creditor is willing to settle a debt for less than what you owe because they fear your financial situation is so uncertain that they won’t recover any money from you in the near future.

What is Upsolve for bankruptcy?

Upsolve is a nonprofit tool that helps you file bankruptcy for free. Think TurboTax for bankruptcy. Get free education, customer support, and community. Featured in Forbes 4x and funded by institutions like Harvard University so we'll never ask you for a credit card. Explore our free tool

How to reach out to your creditor?

Now it’s time to reach out to your creditor. You can do this by telephone or by letter. Either way, you’ll need to have some cash saved up beforehand. Most debts get settled after the borrower makes a one-time lump-sum payment of the outstanding debt. In other cases, you’ll need to pay two or three large payments over a short period of time instead. Creditors rarely agree to let borrowers use a payment plan with monthly payments to settle their debts.

How long does it take to settle a debt?

Another major advantage is that the DIY debt settlement process tends to be faster, perhaps six months or less. In contrast, using a debt settlement company can easily take several years. Not only does this extra time mean it takes longer to get debt relief, but that’s more time for your debt to accrue interest and penalties.

What is debt settlement?

In general, debt settlement is usually about half of the total amount of money owed. If the original debt settlement offer from the creditor was less than this, the borrower may want to send a counter offer that is about half of what he or she owes. This amount has a good chance of being accepted by the creditor because it is still within ...

What happens when you make a counter offer to a debt settlement?

When making a counter offer, the borrower should be absolutely sure they cannot meet the offer given. When a counter offer is made, it voids the original offer. The creditor could withdraw the original debt settlement offer ...

What happens if a counter offer letter is arrogant?

If the counter offer letter is arrogant in tone or too full of misery, the creditor may not take it seriously and think that the borrower is just trying to pay as little as possible. It should be professional and accurate. When creditors make a debt settlement offer, they have decided to accept a lower amount.

What is debt settlement counter offer?

If this is the case, the borrower may send a debt settlement counter offer of a lower amount. The letter should explain the reason the borrower cannot pay the amount offered by the creditor. In general, debt settlement is usually about half of the total amount of money owed. If the original debt settlement offer from the creditor was less ...

Why is it important for a borrower to always be courteous and polite?

The borrower should remember that he or she is not entitled to have their debt reduced. It is up to the creditor whether they are willing to negotiate. This is why it is important for the borrower to always be courteous and polite and have a genuine reason for financial difficulty.

What happens if a creditor negotiates with a borrower?

If a creditor is willing to negotiate with a borrower for a lower amount in order to have a debt paid off, the creditor may send a debt settlement offer to the borrower. This settlement amount may still be more than the borrower can pay due to circumstances beyond his or her control. If this is the case, the borrower may send a debt settlement ...

What does it mean when a creditor thinks a debt is overdue?

This means they either need to forget the debt or they need to give it to a collection agency.

What is a settlement offer letter?

A Settlement Offer Letter is a communication between two parties in a dispute. The dispute does not have to be in a court of law, although most of the time, it is. One party sends the other party this Settlement Offer Letter, with the proposed terms for a complete settlement between the parties. Rather than a formal legal document, this letter can ...

What information is entered in a settlement agreement?

The parties' identifying details and contact information will be entered, as well as the proposed settlement terms.

What happens if a dispute is not litigated?

If the dispute is not being litigated, details of the incident at the heart of the parties' dispute will be entered.

Is a settlement agreement a legal document?

Although the terms listed in this letter will generally become the terms of the Settlement Agreement, this letter does not create a legally binding contract.

Is a settlement offer letter legal?

Although settlement agreements can be governed by both state and federal law, this Settlement Offer Letter is not a legal document, so it is simply a best practice to give the recipient of the letter as much information as possible about the terms of the proposed settlement.