What is payment card settlement?

One option may be a credit card settlement, which is when your credit card company forgives a portion of the amount you owe in exchange for you repaying the remaining amount.

How do card interchange fees work?

Definition: Interchange fees are transaction fees that the merchant's bank account must pay whenever a customer uses a credit/debit card to make a purchase from their store. The fees are paid to the card-issuing bank to cover handling costs, fraud and bad debt costs and the risk involved in approving the payment.

What is MC settlement?

The settlement is the result of a class action lawsuit against Visa and Mastercard. Under its terms, Visa and Mastercard will pay between $5.54 and $6.24 billion dollars to businesses that accepted Visa and Mastercard between 2004 and 2019.

How much will I get from Bank of America settlement?

What does the Settlement provide? Bank of America has agreed to establish a Settlement Fund of $27.5 million from which Settlement Class Members will receive payments or Account credits. The amount of such payments or Account credits cannot be determined at this time.

Who sets the interchange fee?

Interchange rates are set by credit card companies such as Visa, MasterCard, Discover, and American Express. With Visa and MasterCard, the rate is set on a semiannual basis, usually in April and then in October. Other credit card companies might set their rates annually.

Who keeps interchange fees?

The processor (acquiring bank) deposits the funds into your account, usually within 48 hours. Then the cardholder's bank (issuing bank) takes the money from the customer's account. The issuing bank deducts the interchange fees and sends the rest to the acquiring bank.

What was the outcome of the 2013 class action lawsuit against Visa and Mastercard?

In December 2013, U.S. District Court Judge John Gleeson approved a settlement in the case that amounted to $7.25 billion. The settlement lowers interchange fees for merchants and also protects credit card companies from being sued over the issue again in the future. That settlement was reversed.

What is the difference between settlement and authorization?

Authorization is a conversation between you and the issuer to determine if the transaction should be approved or declined. Settlement is the process of moving money from the cardholder's account to your account. The two processes fit together like this: A customer uses a credit or debit card to make a purchase.

How does Visa settlement work?

0:201:27Visa Direct - Merchant Settlement - YouTubeYouTubeStart of suggested clipEnd of suggested clipWith no need for bank routing or account numbers while traditional methods can take days or weeks toMoreWith no need for bank routing or account numbers while traditional methods can take days or weeks to process visa Direct enables real-time payments 24/7 even on nights weekends.

Can my lawyer cash my settlement check?

While your lawyer cannot release your settlement check until they resolve liens and bills associated with your case, it's usually best to be patient so you don't end up paying more than necessary.

What bank has the biggest lawsuit?

The settlement by BNP Paribas in the U.S. sanctions case for nearly $9 billion ranks among the biggest ever among banks since the early 2000s, and tops the list of those not related to the financial crisis. It is the biggest-ever fine levied against a bank for violating U.S. economic sanctions.

What's going on with the Bank of America lawsuit?

Bank of America is being sued by a customer who claims the bank “misrepresented” its free money transfer service and failed to warn her and others about the fees it could cause, court documents show.

How much do banks make on interchange fees?

In the United States, the average interchange rate is around 0.3% for debit cards and 1.8% for credit cards.

How can I lower my interchange fees?

Merchants can lower their interchange fees by increasing security measures at the moment of payment capture and elsewhere. Debit card transactions that are accepted without PINs or other authentication information will process at a higher interchange rate because the transaction incurs more risk for the card network.

How are interchange fees split?

Interchange fees are split up between some of the money going to the card-issuing bank – like Chase or Bank of America – while the rest of the fees go to the card brand.

What is the average interchange fee?

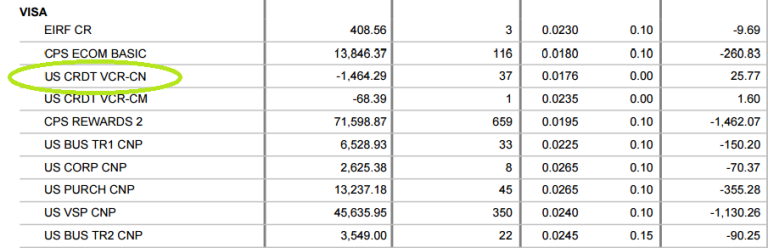

Interchange fees vary by credit card network and by the type of transaction. Currently, the average credit card interchange fees range from 1.15% to 3.25%.

How are interchange fees calculated?

Interchange fees are set by the major credit card associations (Visa, Mastercard, American Express, and Discover). Each association publishes a sch...

Why are interchange fees so high?

Interchange fees reflect the level of risk associated with the given transaction type. Fees for credit card transactions are particularly high beca...

Who sets merchant interchange fees?

Interchange fees are set by the credit card associations (Visa, Mastercard, American Express, and Discover), not the issuing bank. Thus, fees for u...

Are interchange fees negotiable?

No. Interchange fees are established by the major credit card associations and are not subject to negotiation. Be very wary of any sales agent who...

Who decides the percentage of interchange fees?

The credit card associations determine the interchange fee schedules, and neither the cardholder’s issuing bank nor your merchant account provider...

What is the highest interchange rate?

Card-not-present and manually keyed-in transactions typically have the highest interchange rates. Also, any transaction where the customer uses a r...

What is interchange fee?

The truth is that interchange fees (or, more accurately, interchange reimbursement fees) are, in most cases, the single largest expense you’ll have to pay when accepting a customer’s credit or debit card. Interchange reimbursement fees vary widely based on many factors, and you’ll usually have little or no control over them.

Where does the money go for credit card interchange fees?

While your provider collects the interchange fees from you, it doesn’t get to keep them. Interchange fees are ultimately paid to the bank or other business entity that issued the customer’s card . For each transaction, there will also be a small network fee that goes to the credit card association as well as your provider’s markup.

Why were the proposed changes to the fee schedule postponed?

Why were these changes postponed? By all accounts, the proposed changes to the fee schedule would have lowered several retail interchange rates but also would have significantly raised rates for most eCommerce transactions . Online credit card fraud has become a growing problem in recent years, and the proposed higher rates reflected the increased level of risk taken on by the issuing banks. Also, Visa and Mastercard are trying to nudge merchants into using tokenization measures to combat this type of fraud. The proposed rates would have included lower rates for transactions that used tokenization to encourage the adoption of this type of security technology.

What is the difference between Discover and Mastercard?

The main difference here is that Discover and American Express function as both the issuing banks and the sponsoring credit card associations. On the other hand, Visa and Mastercard merely slap their logo on cards that are actually issued by a bank. The issuing bank is the entity that’s advancing credit to consumers and taking on the risk associated with doing so. They end up collecting almost all of the interchange fees charged on a transaction.

Why are credit card fees so high?

Fees for credit card transactions are particularly high because the issuing bank has to loan the funds to the consumer to complete the transaction and then hope that this loan will be fully repaid on time.

How much does Mastercard charge in 2019?

Those small fees add up quickly. In 2019, Mastercard alone racked up a little over $8.1 billion in net revenue. Here’s the important thing that you, the merchant, need to understand: Although you’ll have to pay the interchange on every credit/debit card transaction, it’s only part of your total cost for processing.

What is the average interchange rate for credit cards?

The rates in the table above represent only the tip of the iceberg. In the United States, the average interchange rate is around 0.3% for debit cards and 1.8% for credit cards. However, we’d caution you that these numbers have very little value due to the enormous range of possible rates under which any given transaction might fall.

What is the settlement for Visa?

What is the Payment Card Settlement? The settlement is the result of a class action lawsuit against Visa and Mastercard. Under its terms, Visa and Mastercard will pay between $5.54 and $6.24 billion dollars to businesses that accepted Visa and Mastercard between 2004 and 2019. By settling, the lawsuit will not go to trial.

Who is eligible to get money from the settlement?

Business owners that accepted Visa and/or Mastercard at any point between 2004 and 2019 are eligible to file a claim.

Why was Visa sued?

Visa and Mastercard were sued for allegedly violating antitrust laws. That is, they were accused of putting rules into place that would prevent competition or incentive to lower interchange rates. The lawsuit claims that if Visa and Mastercard had not engaged in that behavior, businesses would have paid lower interchange fees.

Why do businesses overpay for credit card processing?

Even after this settlement, many businesses will still overpay for credit card processing. That’s because there are multiple fees that make up the final cost, and most businesses aren’t sure where they can save .

What is a markup fee?

The markup includes any of the fees tacked on after interchange – monthly fees, statement fees, batch fees, PCI compliance fees. The lower you can get those fees, the less you’ll pay overall. And – unlike interchange – those fees are in your processor’s control. Focus your negotiation efforts on processor’s markup, or join a wholesale processing club to have experts do it for you.

Does CardFellow have a cancellation fee?

Our independent experts have negotiated optimal pricing models and terms for our members, resulting in lower-than-market costs with no cancellation fees, lifetime rate-increase protection, and CardFellow’s complimentary statement monitoring.

Can you lower interchange fees?

Let the lawyers argue about interchange fees. Until and unless they come to an agreement to lower those fees, there’s nothing you can do about them. Instead, focus on the fees you CAN lower: your processor’s markup.

What banks conspired to artificially inflate interchange fees?

Plaintiffs allege that, between January 1, 2004 and the January 25, 2019, Defendants Visa, MasterCard and several banks including Bank of America, JPMorgan Chase and Citigroup conspired to artificially inflate the prices of interchange fees that merchants' acquiring banks pay to customers' issuing banks in a credit or debit card transaction. Since the interchange fees are inflated, the discount fees merchants pay to accept card payments are in turn artificially high, and various rules prevent merchants from challenging the inflated fees.

What is the deadline for a pending settlement?

Pending Settlements: Filing Deadline: $5.54 to $6.24 Billion. Not yet established; Claim forms are not yet available.

What is SRG in class action?

SRG is a third party service that can be hired to file and track claims. We specialize in helping companies file claims to obtain their share of settlement money from class action lawsuits once a settlement has been reached. Our services are voluntary and are not required to file a claim. No-cost assistance will be available from the Class Administrator and Class Counsel during any claims-filing period. Official documents and information on the case can be found on the Court-approved case website www.paymentcardsettlement.com. This summary is not and should not be construed as legal, tax or other professional advice.

Where is the In re Payment Card Interchange Fee and Merchant Discount Antitrust Litigation?

The docket number is 05-md-01720. The United States District Court in the Eastern District of New York in Brooklyn is the venue.

When will the swiping fee be reversed?

That settlement was reversed. Currently one for US$ 6.24 billion is scheduled to go before the district court on November 7, 2019. Terminals for swiping credit cards, and origin of the term "swipe fee".

What was the settlement of the Dodd-Frank bill?

Dodd-Frank required the Federal Reserve to write rules for swipe fees on debit card purchases. Richard Durbin, the senator from Illinois who was the main proponent of those rules, has called the proposed settlement on credit card swipe fees, "gives Visa and MasterCard free rein to carry on their anti-competitive swipe-fee system with no real constraints and no legal accountability. This is not a settlement I would agree to. I hope that the remaining merchant plaintiffs will review the proposed settlement carefully and think hard about whether it will be good for the future of our credit- and debit-card systems.” Barney Frank, a representative from Massachusetts and a primary supporter of legislation to repeal rules on debit card swipe fees said he supports the settlement and stated, "A free-market approach in this area will be better for the economy and all concerned parties.”

What did the plaintiffs argue about the settlement?

The plaintiffs argued that the settlement violated their rights by not allowing them to opt out of some provisions. The inability to opt out of litigation releases that bar future suits was an important point of contention. Jeff Shinder, a lawyer for the plaintiffs said, "The proposed settlement violates the due process rights of millions of merchants by denying them the ability to opt out of the injunction, and this fundamental issue of law should be addressed now before notice goes out to merchants."

What is swipe fee?

Plaintiffs allege that Visa, Mastercard, and other major credit card issuers engaged in a conspiracy to fix interchange fees, also known as swipe fees, that are charged to merchants for the privilege of accepting payment cards, at artificially high levels. In their complaint, the plaintiffs also alleged that the defendants unfairly interfere with merchants from encouraging customers to use less expensive forms of payment such as lower-cost cards, cash and checks.

Who is the senator who proposed the settlement on credit card swipe fees?

Richard Durbin , the senator from Illinois who was the main proponent of those rules, has called the proposed settlement on credit card swipe fees, "gives Visa and MasterCard free rein to carry on their anti-competitive swipe-fee system with no real constraints and no legal accountability.

Who opposes the Safeway settlement?

Opposition. According to court filings, Target, Wal-Mart, Home Depot, Neiman Marcus, Saks, and 1,200 other plaintiffs oppose the settlement. A group of large merchants including Kroger, Walgreens, and Safeway have reached a separate agreement with the defendants over swipe fees.

When did the interchange fees settlement happen?

The Court granted final approval of this Settlement on December 13, 2019, and will establish a claims process whereby eligible merchants will be able to claim their share of the billions in settlement funds.

What is reconciliation with settlement administrator?

Reconcile with the Settlement Administrator to help ensure that you receive a proper and timely recovery.

.jpg)