Insurance settlement offers are sent by an at-fault party’s insurance company to provide compensation to the injured party. A settlement usually contains a lump sum of money or a structured payment plan covering medical bills, lost work time, and other costs.

Should you accept a settlement offer from an insurer?

When it comes to settlement offers from an insurance company, you should only accept the right offer. Settling the case puts money into your bank account faster than going to trial. You also avoid the risk of getting an unfavorable verdict from a jury. But what makes an offer fair? An offer should fairly compensate you for your damages.

How to counter offer an insurance settlement?

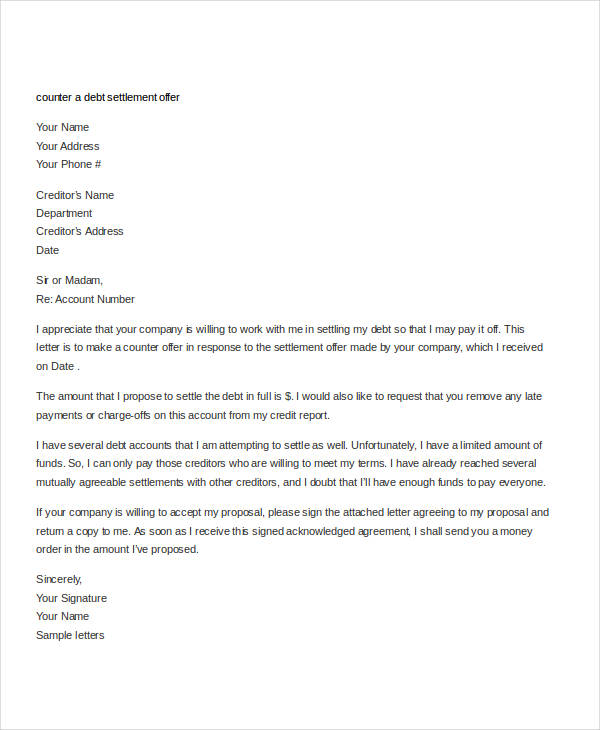

How to Counter-Offer an Insurance Settlement. From the standpoint of procedure, you will need to make a counter-offer in writing. Be sure you send your letter to the appropriate person, whether that be an insurance adjuster or an attorney. Make it clear that you are rejecting their initial offer and include your reasons for doing so.

What to know before signing an insurance settlement?

Before you sign a car insurance settlement agreement, keep the following things in mind: Know the value of your claim: Before you agree to receive insurance money after a car accident, you will need to be confident that the insurance money satisfies the value of your claim. Include in your calculations your medical bills, property damage, lost ...

Should you accept a settlement offer?

You can accept the settlement offer and pay the settlement account in full. This is the easiest and fastest way to deal with the debt, assuming you’ve received a legitimate settlement offer.

Is it good to accept a settlement offer?

It is not in your best interest to accept a settlement offer without speaking with an attorney. The initial settlement offer from the insurance company is probably not fair. The offer may be much lower than the value of your damages. If the insurance company sends you a check, do not cash the check.

What is an insurance settlement?

Insurance settlement. The payment of proceeds by an insurance company to the insured to settle an insurance claim within the guidelines stipulated in the insurance policy.

What happens if you decline an insurance offer?

If you reject the insurance settlement, you retain your right to seek full damages through the legal system. Rejecting the settlement protects your rights to maximum compensation under California personal injury law and allows you to fight for a fair settlement that covers your medical expenses.

Why would an insurance company want to settle?

When an insurance company offers you a settlement, they are essentially acknowledging their client's fault in the accident. They want you to settle to avoid litigation or going to court. Insurance companies usually do not want to get legal help involved.

Should I accept first offer of compensation?

Unless you have taken independent legal advice on the whole value of your claim, you should not accept a first offer from an insurance company.

How is a settlement amount calculated?

Settlement amounts are typically calculated by considering various economic damages such as medical expenses, lost wages, and out of pocket expenses from the injury. However non-economic factors should also play a significant role. Non-economic factors might include pain and suffering and loss of quality of life.

How do you respond to a low ball settlement offer?

Steps to Respond to a Low Settlement OfferRemain Calm and Analyze Your Offer. Just like anything in life, it's never a good idea to respond emotionally after receiving a low offer. ... Ask Questions. ... Present the Facts. ... Develop a Counteroffer. ... Respond in Writing.

How do you reject and respond to a low insurance settlement offer?

Countering a Low Insurance Settlement OfferState that the offer you received is unacceptable.Refute any statements in the adjustor's letter that are inaccurate and damaging to your claim.Re-state an acceptable figure.Explain why your counteroffer is appropriate, including the reasons behind your general damages demands.More items...•

How do insurance companies negotiate settlements?

Let's look at how to best position your claim for success.Have a Settlement Amount in Mind. ... Do Not Jump at a First Offer. ... Get the Adjuster to Justify a Low Offer. ... Emphasize Emotional Points. ... Put the Settlement in Writing. ... More Information About Negotiating Your Personal Injury Claim.

Do insurance companies want to settle quickly?

Insurance companies want to settle cases right away, because they don't want you to have an opportunity to speak to a personal injury lawyer. If an insurance company is offering you any money, it is always advisable that you at least have a consultation with an attorney.

Do insurance companies try to get out of paying?

Insurance companies will seek to decrease payments or deny claims for injuries caused by an insured person's actions. After becoming injured, victims of accidents want nothing more than to move on from the traumatizing experience.

How long do insurance companies take to settle a claim?

The time that it takes an insurance claim to finalise could be anywhere between a week, a month or even a year. It depends on a number of factors, such as the type of claim, the complexity of the situation, how severe the damage is and how many people are involved in the process.

How do settlements work?

A settlement agreement works by the parties coming to terms on a resolution of the case. The parties agree on exactly what the outcome is going to be. They put the agreement in writing, and both parties sign it. Then, the settlement agreement has the same effect as though the jury decided the case with that outcome.

What is a settlement value?

The settlement value of a variable payout contract is the amount of contract value remaining, based on whether it was bought or sold. The difference between the price at which the contract was bought or sold, and the settlement value, determines the profit or loss (excluding any applicable exchange fees).

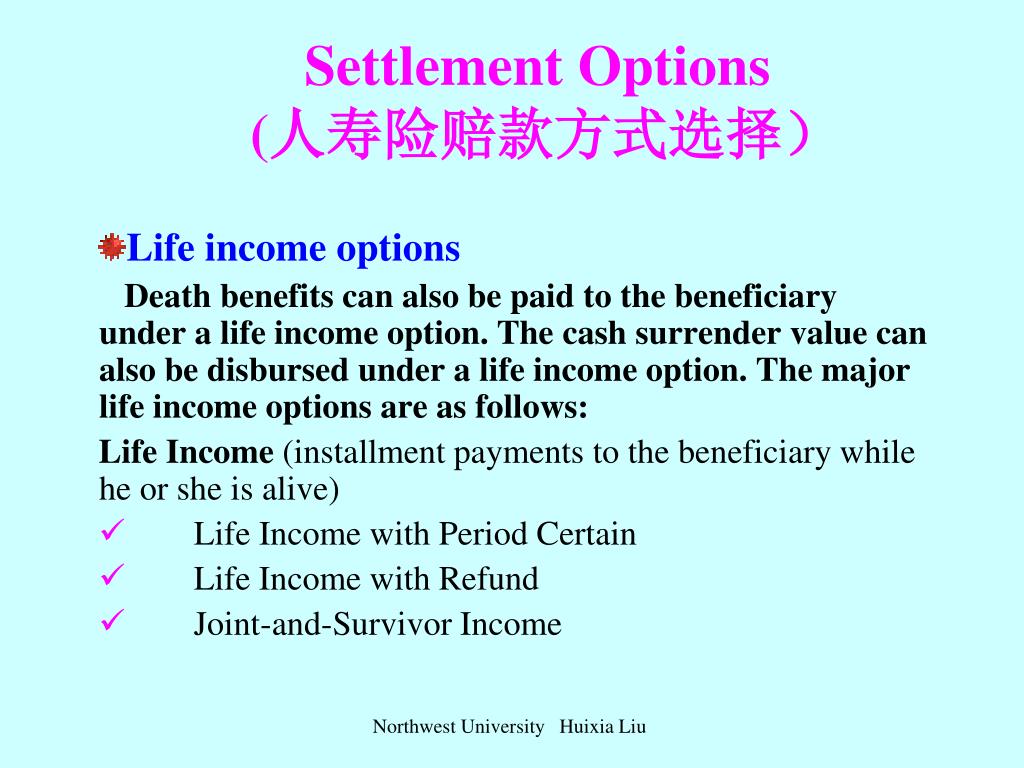

What is a settlement option?

Settlement Options — in life insurance, how proceeds are paid to the designated beneficiaries. Most life insurance policies provide for payment in a lump sum.

What reduces the amount paid in a claims settlement?

Car insurance coverage The insurance company pays up to the policy limits. They also reduce the settlement by the amount of any applicable deductible. Car insurance coverage can limit the amount of a settlement even if the damages are greater than the policy limits.

What percentage of settlement is offered?

For example, the insurer may require that the first offer be 40% of the value of the case. There is no industry-wide standard on this. Different insurers have different procedures. Learn more about factors that determine personal injury settlement value.

What is a claim adjuster?

If you're negotiating a personal injury claim with an insurance company, you'll probably be dealing with a "claims adjuster.". It may be helpful to understand how the adjuster typically operates before you put together a written demand letter, and certainly before you accept (or reject and counter) a personal injury settlement offer.

What do adjusters think about in a personal injury case?

In order to value the case, the adjuster has to think about two things: 1) what are the claimant's chances of winning at trial if a personal injury lawsuit is filed in court, and 2) how much might a jury award the plaintiff in damages?

What does an insurance adjuster do?

Just like an attorney, an insurance adjuster will want to investigate and get a full understanding of the facts of the underlying accident and the claimant's injuries and other losses (called " damages " in legalese).

What documents do you need to file a personal injury claim?

The adjuster will usually request documents such as medical bills, proof of earnings, tax returns, and proof of property damage.

What is a third party claim?

If you're making a claim with the insurance company of the person you think is responsible for your accident, you're making a "third party" claim. The first thing the adjuster will want to find out is what the policyholder (that's the person you're saying is at fault for the accident) has to say about what happened. Besides talking to the insured person to hear his or her story firsthand, the adjuster will read any police report or accident report related to the incident.

Is there an industry wide standard for personal injury settlements?

There is no industry-wide standard on this. Different insurers have different procedures. Learn more about factors that determine personal injury settlement value. One very important point is that adjusters often have leeway to adjust the first offer depending on who they are dealing with.

What is a low ball settlement?

A low-ball settlement occurs when an insurance company comes back with a settlement amount that is well below reasonable.

How many times does an adjuster multiply medical special damages?

The adjuster will multiply the medical special damages number by one and a half to three times if the injury is minor and up to five or more times if the injury is especially deliberating and long-term. After this number is calculated, any income lost as a result of the injury will be added.

What happens if you are injured by someone else's negligence?

If you’ve been injured because of someone else’s negligent acts, you may be able to file a personal injury claim and collect a settlement from the liable party’s insurance company. The settlement is designed to pay for any damages that your injury has caused.

How to contact a personal injury lawyer in Chicago?

To avoid being stuck with a low-ball settlement and ensure an insurer treats you fairly, you should consult our personal injury attorneys in Chicago at (312) 236-2900.

Can an insurance adjuster tell you what formula they used to come up with the value of your claim?

Keep in mind that an insurance adjuster will not inform you of what formula they used to come up with the worth of your claim. In addition, understand that the damages formula serves as a way for insurers to arrive at a starting point for reaching a settlement amount.

The First Settlement Offer from an Insurance Company

It is important to note that when an insurance company offers a settlement, the first offer is not cast in stone but typically no more than an attempt by the insurance company to settle quickly and cheaply. Victims should remember that insurance companies work in their own best interests and will try to preserve their profits.

Negotiating with the Insurance Company

Once an insurance company offers a settlement and you or your attorney provided a counter-offer, the negotiation phase begins. This is where things can become challenging and complex, resulting in many phone calls and letters going back and forth between you and the insurance company.

Mistakes to Avoid When Negotiating with Insurance Companies

Knowing how to negotiate when an insurance company offers a settlement in a way that does not compromise your legal rights can be difficult. However, there are some mistakes you should avoid at all costs as they can have an impact on your final settlement figure.

Giving a Recorded Statement

Insurances often use manipulative tricks and tactics designed to try and trip up accident victims. A recorded statement can provide the insurance company with ammunition that they may try to use against you in an effort to minimize your settlement offer.

Thinking You Do Not Need Legal Advice

Individuals who only suffered minor injuries and property damage can sometimes recover adequate compensation from their own insurer without too much struggle. However, those who have significant medical bills and other losses should consider seeking legal assistance promptly.

Consider Visiting With Our Experienced Attorneys Regarding Your Insurance Company Settlement

Consider visiting with an attorney to learn more about your possible legal protections, especially if the insurance company has already offered you a settlement and you are unsure whether to accept. Accepting a first settlement offer can be a mistake as it may not cover all your damages in the future.

Why do insurance companies offer settlements?

Insurance companies are in business to make money, so they act to protect themselves financially, which means they try to pay as little as possible. So the initial settlement offer you receive is likely to be much lower than your demanded amount and may not be close to covering all of your expenses and damages from the accident.

Why are settlements so common?

Here’s Why Settlements Are So Common. Insurance companies exist to protect their policyholders by paying claims against them. Unless the insurance representative has a solid reason not to pay the claim, you can almost always expect a settlement offer after filing a claim with an insurance company. Of course, the insurance adjuster will start by ...

How do insurance companies determine your damages?

The insurance company will start to determine your expenses and damages by asking a lot of questions. They’ll talk to their policyholder and they’ll want you to go on record about the details of the accident, like the time of day, weather, what you were doing, and so forth.

Why do you hire an attorney for insurance?

Sometimes, just by hiring an attorney, you show the insurance company you’re serious about getting the amount of money you deserve and won’t back down. This opens up insurance settlement negotiations that may work out in your favor.

How to understand the value of an insurance company's initial offer?

The best way to understand the value of the insurance company’s initial offer is for you and your attorney to accurately value the claim. This can be a complex undertaking when all types of compensation are considered, including the monetary value of personal losses associated with your accident.

What is the need to prove in a personal injury case?

Proving need is squarely on the shoulders of the victim in a personal injury case. An insurance company will require clear evidence of expenses and damages before agreeing to a settlement.

What to expect from insurance company after an accident?

Expect the insurance company to try to uncover evidence and statements about the accident that may jeopardize your claim. We repeat: Don’t provide statements until you speak to your attorney!

How to receive a settlement offer?

You may receive a settlement offer in a phone call or email, which will be followed by a letter. Once you have the settlement offer letter, you have the right to make a counter demand if you find the offer unacceptable. Compare what the insurance company has offered to your record of costs and losses, and the maximum payment provided by ...

What should an insurance settlement account for?

An insurance settlement should account for all of these losses as they apply to you and your situation, up to the limits of the applicable insurance coverage.

How to prepare for an insurance company offering less than you deserve?

Prepare for the real possibility that the insurance company will offer less than you deserve by keeping a record of your costs and losses related to your accident and injury. Save copies of all bills and receipts and keep a journal of your recovery.

What to do if your insurance is disputed?

You could benefit from the assistance of an experienced personal injury lawyer if your insurance claim is disputed after an accident. Sometimes, just a letter on a law firm’s letterhead helps an insurance company get more serious about responding to a claim.

How do claims adjusters follow up on a claim?

A claims adjuster should follow up on your claim by contacting you and investigating your case. The investigation may include reviewing your medical records, obtaining vehicle repair estimates, reviewing police accident reports, interviewing you and reviewing your initial claim documents.

What to do if insurance company is using delay tactics?

You must also consider how slowly negotiations are going.If the insurance company is using delay tactics, you will need to keep in mind the statute of limitations for filing a personal injury lawsuit. You do not want to let the time limit expire.

What to do after an accident?

After suffering an injury in an accident, you may be able to turn to insurance for coverage of medical costs and other losses. You might file a claim under a policy you hold (e.g., auto collision insurance, homeowners’ insurance, health insurance) or through another person’s liability insurance if he or she was at fault.

How to Figure Out What Is a Good Settlement Amount

When you’ve been injured in a car crash, slip and fall at a store, or another dangerous mishap, consider how much your injuries have affected your day-to-day life. Very serious injuries such as spinal fractures or traumatic brain injuries, for example, impact people’s lives in serious and potentially long-term ways.

How to Increase Your Chances of a Good Settlement Offer

You want to be fairly paid for the damages you’ve suffered. However, insurance companies look at one thing when negotiating settlement offers—their own bottom line. They will try to give you the lowest offer they possibly can.

Contact a Skilled Personal Injury Lawyer to Learn Options for Your Settlement Amount

Knowing how much to ask for in an injury claim is often confusing. This is especially true if your injuries are serious enough that you need medical treatment and other care into the future. You don’t want to ask for too little or accept a lowball offer from the insurance company or you could end up paying a severe financial price.

Investigating The Claim

Investigating The Claimant

Gathering Claim Documentation

Determining Settlement Value

Determining The Value of A Pain and Suffering Claim

The First Settlement Offer

- Once the insurer has arrived at a settlement figure, they must decide what to offer. The first offer is going to be a percentage of what the insurer thinks is the final value of the case. For example, the insurance company may require that the first offer be 40% of the value of the case. There is no industry-wide standard on this. Different insurer...

How A Lawyer Can Help You Negotiate The Settlement

Next Steps in The Injury Settlement Negotiation Process