What details are included in A HUD-1 Settlement Statement?

A HUD-1 settlement statement, also referred to simply as a settlement statement, details every charge associated with your new loan . It also outlines who is responsible for each of those charges - the buyer or the seller - as well as any credits you may receive for things like taxes, insurance or deposits.

Does the rebate appear on the hud-1/settlement statement?

Does the rebate appear on the HUD-1 Settlement Statement? Yes, we work with the closing attorney and your lender from the beginning of the transaction to make sure that your rebate is accounted for properly.

Is HUD 1 statement required for refinancing?

What is a HUD-1 Settlement Statement? The HUD-1 Settlement Statement is a document that lists all charges and credits to the buyer and to the seller in a real estate settlement, or all the charges in a mortgage refinance. If you applied for a mortgage on or before October 3, 2015, or if you are applying for a reverse mortgage, you receive a HUD-1.

How to properly record a HUD settlement?

- Deposit made by the buyer

- The loan amounts

- The amount owed by the seller to the buying party is a credit entry and must record. ...

- Property tax and assessment pro-ration credits from seller to the buyer of the HUD Settlement Statement

- Lastly, any additional credits to the buyer will be entered here from any source, if not from the seller

Who provides HUD-1 Settlement Statement?

A settlement agent, or closing agent, will prepare a HUD-1 settlement statement at the closing of a real estate loan. The final version will explicitly state all costs involved with the real estate loan and to whom the individual charges and fees will be paid to.

What happened to the HUD-1 Settlement Statement?

The HUD-1 Settlement Statement is a standard government real estate form that was once used by settlement agents, also called "closing agents," to itemize all charges imposed upon a borrower and seller for a real estate transaction. The statement is no longer used, with one exception: reverse mortgages.

Is a settlement statement the same as a HUD-1?

What Is a HUD-1 Form? A HUD-1 form, also called a HUD-1 Settlement Statement, is a standardized mortgage lending document. Creditors or their closing agents use this form to create an itemized list of all charges and credits to the buyer and to the seller in a consumer credit mortgage transaction.

Is the HUD-1 Settlement Statement the same as the closing disclosure?

Another big distinction between the Closing Disclosure and the HUD-1 is where the HUD-1 listed all terms, charges and credits for both the buyer and the seller, the Closing Disclosure has a separate form for the buyer as it does for the seller. This provides for more consumer protection at the closing table.

How do I get my HUD payoff statement?

Requests for payoff statements, subordinations, releases, and other documentation specific to these programs can be submitted to:Payoff Requests: [email protected] Requests: [email protected] Requests: [email protected] Partial Claim document submittal: [email protected] items...

What replaced the HUD-1 Settlement?

The Closing Disclosure combines and replaces the HUD-1 Settlement Statement and the final Truth-in-Lending (TIL) statement. The form mirrors the information provided on the Loan Estimate.

Is a settlement statement the same as a closing statement?

A settlement statement is a document listing the terms and conditions of a settlement agreement and details all related costs or credits due to each party. A mortgage loan settlement statement is commonly known as a closing statement.

What is the primary purpose of the settlement statement?

A settlement statement provides a breakdown of all the closing costs and credits involved in a real estate transaction or refinance.

Is closing disclosure the same as closing statement?

A closing statement or credit agreement is provided with any type of loan, often with the application itself. A seller's Closing Disclosure is prepared by a settlement agent and lists all commissions and costs in addition to the net total to be paid to the seller.

What is a final HUD statement?

The HUD-1 Settlement Statement is a document that lists all charges and credits to the buyer and to the seller in a real estate settlement, or all the charges in a mortgage refinance.

What is a HUD closing disclosure?

The Closing Disclosure (CD - formerly the HUD-1 Uniform Settlement Statement) is a three-page, government-mandated form that details the costs associated with a real estate transaction. The borrower should receive a copy of the CD at least one day prior to the closing.

What is a HUD-1 settlement statement?

A HUD-1 settlement statement, also referred to simply as a settlement statement , details every charge associated with your new loan. It also outlines who is responsible for each of those charges — the buyer or the seller — as well as any credits you may receive for things like taxes, insurance or deposits.

What is the first page of a HUD settlement statement?

The first page of the settlement statement has a transaction overview, including the amount of cash you need to bring to closing. The sections below are highlighted so you can have an idea of what they look like on the HUD-1 settlement statement you’ll receive.

How long do you have to give a closing disclosure?

In contrast, lenders must give you a closing disclosure three days before closing. Everyone taking out a HELOC, reverse mortgage or manufactured home loan should ask their lender for the HUD-1 document at least a day before closing to allow time to review the contents, fix errors and raise questions with the lender.

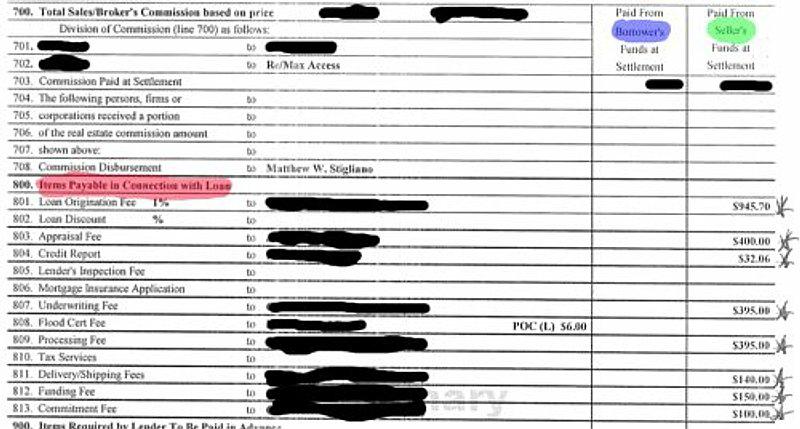

What is section 300?

No. 5 (Section 300): Cash at settlement from/to borrower. This section explains if you need to bring cash to the settlement. In most cases, the closing costs for a reverse mortgage refinance or HELOC will be subtracted from the loan, so you don’t need to bring funds to the closing.

How long does it take to pay down a HELOC?

You can borrow as much as you need up to your maximum loan amount, then pay it down to zero as many times as necessary during a set draw period that usually ends after 10 years.

How long does a HELOC loan last?

This revolving product has a set draw period that usually ends after 10 years. After the draw period is over, you pay the remaining balance in fixed payments until it is paid in full.

How many sections are there in a settlement statement?

The settlement statement lists charges in three sections. The first section shows charges that cannot change. The next section outlines charges that cannot change by more than 10%, while the final section outlines charges that may change.

What is HUD-1 Settlement Statement?

Janet Wickell. Updated January 29, 2020. The HUD-1 Settlement Statement is a standard government real estate form that was once used by settlement agents, also called closing agents, to itemize all charges imposed upon a borrower and seller for a real estate transaction.

What is HUD-1 form?

The statutes of the Real Estate Settlement Procedures Act (RESPA) required that the HUD-1 form be used as the standard real estate settlement form in all transactions in the United States that involved federally related mortgage loans. 2.

When Is a HUD-1 Used in 2020?

The HUD-1 settlement statement is still used in 2020 for reverse mortgages. These types of mortgages are very popular with sellers over the age of 62 who want to pull equity out of their homes. 4

When Is the HUD-1 Distributed?

Before October 3, 2015, RESPA stated that borrowers should be given a copy of the HUD-1 at least one day prior to settlement. 5 However, entries could easily still be coming in, right up until a few hours before closing.

What is line 902 on a mortgage?

Line 902 shows mortgage insurance premiums that are due at settlement. Escrow reserves for mortgage insurance are recorded later. It should be noted here if your mortgage insurance is a lump sum payment that's good for the life of the loan.

When did the closing disclosure change?

Borrowers began receiving a form called the Closing Disclosure instead of a HUD-1 for most kinds of mortgage loans after October 2015. The change was in response to the TILA RESPA Integrated Disclosures, or simply TRID, which overhauled the way mortgages are processed and disclosed. 3.

What is tabulated before being brought forward to page 1 in Section L or page 2?

Many entries are tabulated before being brought forward to page 1 in Section L or page 2. Columns contain charges that are paid from either the borrower's or the seller's funds. Your closing statement probably won't have entries in all these lines.

What is HUD-1 Settlement Statement?

The HUD-1 Settlement Statement is a standardized mortgage lending form in use in the United States of America on which creditors or their closing agents itemize all charges imposed on buyers and sellers in consumer credit mortgage transactions.

When do you need to inspect a HUD-1?

The settlement agent must permit the borrower to inspect the HUD-1 or HUD-1A settlement statement, completed to set forth those items that are known to the settlement agent at the time of inspection, during the business day immediately preceding settlement. Items related only to the seller's transaction may be omitted from the HUD-1.

What is a HUD-1?

The HUD-1 (or a similar variant called the HUD-1A) is used primarily for reverse mortgages and mortgage refinance transactions. The reference to 'HUD' in the form's name refers to the Department of Housing and Urban Development . Federal regulations require that unless its use is specifically exempted, either the HUD-1 or the HUD-1A, ...

What is the HUD-1A used for?

Federal regulations require that unless its use is specifically exempted, either the HUD-1 or the HUD-1A, as appropriate, must be used for all mortgage transactions that are subject to the Real Estate Settlement Procedures Act.

Is a HUD-1 exempt from the Truth in Lending Act?

The TRID rule mandates the use of a Closing Disclosure form instead. The use of the HUD-1 or HUD-1A is also exempted for open-end lines of credit (home -equity plans) covered by the Truth in Lending Act and Regulation Z. A HUD-1 or HUD-1A Settlement Statement is prepared by a creditor or, more typically, by the settlement agent who conducts ...

What is HUD-1 statement?

The settlement agent shall use the HUD-1 settlement statement in every settlement involving a federally related mortgage loan in which there is a borrower and a seller. For transactions in which there is a borrower and no seller, such as refinancing loans or subordinate lien loans, the HUD-1 may be utilized by using the borrower's side of the HUD-1 statement. Alternatively, the form HUD-1A may be used for these transactions. The HUD-1 or HUD-1A may be modified as permitted under this part. Either the HUD-1 or the HUD-1A, as appropriate, shall be used for every RESPA-covered transaction, unless its use is specifically exempted. The use of the HUD-1 or HUD-1A is exempted for open-end lines of credit (home-equity plans) covered by the Truth in Lending Act and Regulation Z.

Who completes HUD-1?

The settlement agent shall complete the HUD-1 or HUD-1A, in accordance with the instructions set forth in appendix A to this part. The loan originator must transmit to the settlement agent all information necessary to complete the HUD-1 or HUD-1A. (1) In general. The settlement agent shall state the actual charges paid by ...

Who must state the actual charges paid by the borrower and seller on the HUD-1?

The settlement agent shall state the actual charges paid by the borrower and seller on the HUD-1, or by the borrower on the HUD-1A. The settlement agent must separately itemize each third party charge paid by the borrower and seller.

Can HUD-1 be modified?

The HUD-1 or HUD-1A may be modified as permitted under this part. Either the HUD-1 or the HUD-1A, as appropriate, shall be used for every RESPA-covered transaction, unless its use is specifically exempted.

When to use HUD-1?

The HUD-1 must be used in any transaction where a federally regulated mortgage (deed of trust) is involved. In your case, because you are selling for cash, you don’t need to use that form. Inman Connect.

What does HUD stand for?

HUD stands for the Department of Housing and Urban Development. When Congress enacted the Real Estate Settlement Procedures Act (RESPA) many years ago, it authorized HUD to prepare and implement a uniform settlement statement.

Is it a good idea to withhold rent?

My experience tells me that it is not a good idea to withhold the rent — regardless of the reason. Judges that handle landlord-tenant cases hear all kinds of excuses — some legitimate and some wildly fictitious. Judges sometimes believe that the tenant just does not have the money and is thus fabricating an excuse not to pay.

What is HUD-1 statement?

When you buy a home or other piece of real estate property, your escrow or title company will prepare a HUD-1 Settlement Statement. This standardized form outlines all the costs included in your transaction as well as who is responsible for paying for each. When you receive your HUD-1 statement, you’ll know exactly how much you’ll need to bring ...

What is the real estate settlement procedure?

The Real Estate Settlement Procedures Act is a set of laws that helps to protect consumers from unfair practices during the settlement process of real estate transactions. Among the laws are regulations limiting what settlement service providers can charge for their services and how they can work with other settlement providers. RESPA also requires that the HUD-1 Settlement Statement is given to all parties of the transaction no later 24 hours prior to the scheduled closing of the transaction.

What to do if you don't receive HUD?

If you don't receive your HUD-1 at least 24 hours prior to closing, or if you have any issues regarding the charges outlined, speak with your settlement officer or lender. If there is a simple mistake on the HUD-1, these professionals should be able to solve the issue.

How long does it take to get a clarification from a lender?

Under RESPA, lenders have 20 days to acknowledge the inquiry and 60 days to resolve the issue.