What happens after Closing Disclosure?

What happens after signing closing disclosure? After the lender receives the signed Closing Disclosure from all borrowers, they can begin preparing loan documents. Once the loan documents are prepared, they are delivered to the escrow company. Signing. Signing typically takes place 1-2 days before closing.

Who fills out the closing settlement statement?

The settlement statement is prepared by an impartial third party to the transaction, usually an officer with the title or escrow company that performs the closing. In California, both the buyer and the seller sign the HUD-1 settlement statement at closing.

Is the settlement statement the same as a closing statement?

Yes, a settlement statement is the same as a closing statement, though “settlement” is the formal term most likely to be used by the real estate industry. What’s the difference between a Closing Disclosure and settlement statement?

How early are you sending the Closing Disclosure?

The Closing Disclosure must be delivered to the borrower at least three business days prior to the consummation of the loan. If the Closing Disclosure is hand delivered, a waiting period commences which we’ll discuss further in a later post. If the Closing Disclosure is delivered by mail, email, courier, or fax a delivery period of three ...

Is a closing disclosure the same as settlement statement?

Closing Disclosure When you are in the process of closing, you will receive a settlement statement. They arrive three days before closing from your lender. This document is commonly known as the “closing disclosure.” Essentially, this is for buyers to review in advance before closing.

Is there another name for a closing disclosure?

Prior to these rules, home buyers received two documents: the HUD-1 Settlement Statement and the Truth in Lending Disclosure Statement (instead of the Closing Disclosure).

What is final settlement statement?

A settlement statement is a document summarizing all costs owed by or credits due to the homebuyer and seller (or borrower if refinancing). The document also includes the purchase price of the property, loan amount and other details.

What appears on the closing disclosure?

A Closing Disclosure is a five-page form that provides final details about the mortgage loan you have selected. It includes the loan terms, your projected monthly payments, and how much you will pay in fees and other costs to get your mortgage (closing costs).

Is closing Disclosure final approval?

The Closing Disclosure is the final document you'll see in the mortgage loan process just before that massive pile of paperwork you'll face at closing. Here's what the five-page document is and how to use it.

How many days before the closing must the closing disclosure be delivered?

three business daysYour lender is required to send you a Closing Disclosure that you must receive at least three business days before your closing. It's important that you carefully review the Closing Disclosure to make sure that the terms of your loan are what you are expecting.

Is a settlement date the same as a closing date?

"Settlement date" and "closing date" are synonymous terms referring to the date when a property's seller and buyer meet to finalize the deal. At this time, the deed to the property is transferred from the seller to the buyer and all pertinent paperwork is completed.

Is a closing disclosure the same as a HUD-1?

The HUD-1 form, listing all closing costs, is given to all parties involved in reverse mortgage and mortgage refinance transactions. Since late 2015, a different form, the Closing Disclosure, is prepared for the parties involved in all other real estate transactions.

Where do I find closing statements?

If you find at a later time you need a copy of your closing statement, contact the settlement agent for the home purchase. Other parties that may have copies of the settlement documents include your real estate agent, or the financial institution that holds the loan for the property.

Can a loan be denied after closing disclosure?

Can a mortgage be denied after the closing disclosure is issued? Yes. Many lenders use third-party “loan audit” companies to validate your income, debt and assets again before you sign closing papers. If they discover major changes to your credit, income or cash to close, your loan could be denied.

On which page of the closing disclosure would you find the final costs?

Page 3: This is where you'll see a breakdown of the amount of cash you will need at closing. The final figure reflects adjustments and other credits, plus outstanding costs.

What triggers a new 3 day waiting period for closing disclosure?

12 CFR § 1026.19(f)(2)(i). If the overstated APR is inaccurate under Regulation Z, the creditor must ensure that a consumer receives a corrected Closing Disclosure at least three business days before the loan's consummation (i.e., the inaccurate APR triggers a new three-business day waiting period).

What is the difference between loan estimate and closing disclosure?

The Loan Estimate and Closing Disclosure are two forms that you'll receive during the homebuying process. The Loan Estimate comes at the beginning, after you apply, while the Closing Disclosure comes at the end, before you sign the final paperwork for your mortgage.

What is a closing statement?

A closing statement is a form used in a real estate transaction that includes an itemized list of all the buying or selling costs associated with that transaction. It's a standard element of home sales, especially those that involve mortgages, and refinancings.

What does respa stand for?

Real Estate Settlement Procedures ActReal Estate Settlement Procedures Act. RESPA seeks to reduce unnecessarily high settlement costs by requiring disclosures to homebuyers and sellers, and by prohibiting abusive practices in the real estate settlement process.

Does initial disclosure mean I'm approved?

Initial disclosures are the preliminary disclosures that must be acknowledged and signed in order to move forward with your loan application. These disclosures outline the initial terms of the mortgage application and also include federal and state required mortgage disclosures.

Is the closing disclosure more accurate than the loan estimate?

In the meantime, the Closing Disclosure is given to you three days prior to your closing date and includes information similar to the Loan Estimate...

Does closing disclosure mean final approval?

Closing Disclosure is a final accounting of the interest rate and rates of your loan, the closing costs of your mortgage, your monthly mortgage pay...

Is a closing disclosure a commitment to lend?

Once you have selected a lender and executed the gantlet of the mortgage underwriting process, you will receive the Closing Disclosure. It provides...

What comes first close or closed disclosure?

Once you are free to close, you will receive a Closing Disclosure to sign from your provider. You will receive this letter three days before your s...

What is a closing disclosure for buyer?

Closing Disclosure is a five-page form that describes in detail the critical aspects of your mortgage loan, including the purchase price, loan rate...

Does receiving a Closing Disclosure mean the loan is approved?

The loan is approved prior to a lender issuing a Closing Disclosure. However, you’ll want to make sure your credit, income and debt are in check du...

Who gets a copy of the Closing Disclosure?

Typically, buyers and lenders will receive a copy of the Closing Disclosure. It’s recommended that buyers share a copy of their Closing Disclosure...

What happens after signing the Closing Disclosure?

After you sign the Closing Disclosure, you and your lender are not allowed to make any changes to the mortgage information.

Do I have to take on the loan after signing the Closing Disclosure?

No, signing the Closing Disclosure only signifies that you’ve reviewed the mortgage information sent by your lender. If you change your mind about...

What happens if I don’t receive a Closing Disclosure?

Your mortgage lender is required to send you a Closing Disclosure. If you haven’t received the document, reach out to your lender immediately.

What to do if you make a mistake in closing disclosure?

Mistakes happen, so don’t be afraid to ask questions or seek clarification before you sign the paperwork at closing. If it is a major mistake, the buyer can obtain an explanation, and even negotiate a deal or walk away from the loan.

When did the HUD-1 change to the closing disclosure?

The Consumer Financial Protection Bureau (CFPB) took over administration from HUD and replaced the HUD-1 with the Closing Disclosure in October of 2015. It is similar to the HUD-1 in that it details the loan terms and costs, including the interest rates, closing costs, taxes, monthly payments, and more.

What is RESPA disclosure?

RESPA requires different disclosures during different parts of the home closing process and also offers protection to consumers in areas including: Limiting the amount put into escrow for real estate charges. Allowing buyers to use their own title company and title insurance.

What is the real estate settlement procedure act?

1974: The Real Estate Settlement Procedures Act (RESPA) was created to help protect consumers from foul practices, forcing lending institutions to disclose settlement costs upfront. This act is enforced by the Consumer Financial Protection Bureau (CFPB) and includes all types of mortgages. RESPA requires different disclosures during different parts of the home closing process and also offers protection to consumers in areas including: 1 Limiting the amount put into escrow for real estate charges 2 Allowing buyers to use their own title company and title insurance 3 Prohibiting lenders from receiving a fee in exchange for a referral

How long does a loan estimate need to be in the hands of the buyer before closing?

These two documents must be in the hands of the buyer at least 3 days prior to the closing date in order to find any errors or issues before closing. If certain changes are made to the disclosure, the 3-day waiting period starts over. This is one big change with the new TRID rules.

What happens if a buyer makes a mistake in closing?

The progress of settlement procedures and laws for consumer protections in real estate transactions have come a long way, making it safer now than ever to go through the process of closing on a home.

Why was the HUD-1 Settlement Statement required in 2010?

The reason behind all of these amendments and changes was to create more transparency and progress in consumer protection, which leads us into the 1986 HUD-1 Form.

Is the closing disclosure more accurate than the loan estimate?

In the meantime, the Closing Disclosure is given to you three days prior to your closing date and includes information similar to the Loan Estimate. This may interest you : Does closing disclosure mean loan is approved?. However, the numbers and details on the Disclosure Closing are much more accurate.

Does closing disclosure mean final approval?

Closing Disclosure is a final accounting of the interest rate and rates of your loan, the closing costs of your mortgage, your monthly mortgage payment and the grand total of all payments and installments. financial burdens. The form is issued at least three days before signing the mortgage documents.

Is a closing disclosure a commitment to lend?

Once you have selected a lender and executed the gantlet of the mortgage underwriting process, you will receive the Closing Disclosure. It provides the same information as the Loan Estimate but in final form. This means that you include the closing costs of your loan and the specific amount that you will have to pay in the end.

What comes first close or closed disclosure?

Once you are free to close, you will receive a Closing Disclosure to sign from your provider. You will receive this letter three days before your scheduled closing date. As a buyer, it is important to acknowledge this disclosure immediately, or your closing date may be delayed.

What is a closing disclosure for buyer?

Closing Disclosure is a five-page form that describes in detail the critical aspects of your mortgage loan, including the purchase price, loan rates, interest rate, estimated property taxes, and insurance. , closing costs and other expenses.

What is closing disclosure?

The Closing Disclosure is a five-page form that describes, in detail, the critical aspects of your mortgage loan, including purchase price, loan fees, interest rate, estimated real estate taxes and insurance, closing costs and other expenses. It’s important that you review it thoroughly – in fact, it’s one of the most important steps you can take ...

How long do you have to give closing disclosure?

Your lender is required by law to give you the standardized Closing Disclosure at least 3 days before closing. This is what is known as the Closing Disclosure 3-day rule. This requirement is thanks to the TILA-RESPA Integrated Disclosures guidelines, which went into effect on October 3, 2015.

What to do if you find a discrepancy between closing disclosure and loan estimate?

If you find a discrepancy between the Loan Estimate and the Closing Disclosure, the first step is to contact your lender or real estate agent immediately to correct the errors. These mistakes can be as minor as misspelled names or as serious as a change in the interest rate.

Why is it important to read the closing disclosure?

The reason for this is that once you sign, you’re committing to the conditions presented, regardless of whether there are any mistakes in the paperwork. That means it’s crucial that you carefully read the Closing Disclosure your lender sends you.

How long does it take to get a loan estimate?

It should look similar to the Loan Estimate. You’re required by law to receive the Loan Estimate 3 days after you submit a loan application. Take the time to look over both your Loan Estimate and Closing Disclosure in detail to make sure everything you see makes sense.

What documents were used before the HUD-1 settlement?

Prior to these rules, home buyers received two documents, the HUD-1 Settlement Statement and the Truth in Lending Disclosure Statement (instead of the Closing Disclosure). There were two problems with these previous documents: they were confusing, and they were only provided at closing – which offered home buyers very little opportunity to review and make sense of them.

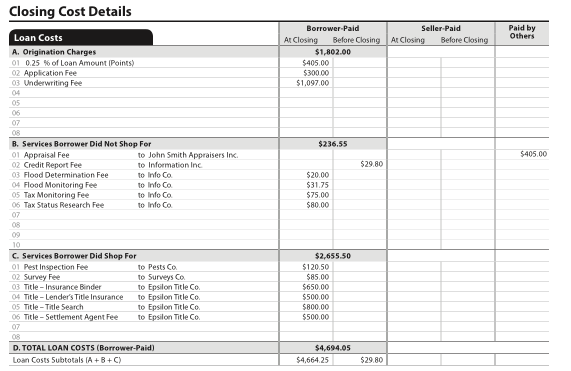

How much is closing cost?

Closing costs will typically be about 2% – 5% of your loan amount. Included at the bottom of the itemized costs, you’ll find the cash to close amount, which is the full amount of money you’ll need to have on hand at closing.

What is closing disclosure?

The closing disclosure is a type of settlement statement that was created and is regulated for the mortgage lending market. The closing disclosure is provided by the lender, closing attorney or title company to a borrower about three days before the closing on real estate. It outlines the final version of the loan terms and costs. Items in the closing disclosure include clauses like:

What are disclosures regarding escrow accounts?

Disclosures regarding escrow accounts and if the lender will collect and distribute property taxes and insurance, total payments and finance charges, as well as appraisals, and lack of payment.

What is a HUD-1 settlement statement?

Both settlement statements, including HUD-1 settlement statements, and closing disclosures are a statements prepared by the closing attorney or title company giving a complete breakdown of costs involved in a real estate transaction. While closing disclosures provide information about a borrower’s loan, settlement statements do not include loan information.

Who can review a reverse mortgage settlement?

Most buyers and sellers review the settlement statement or the closing disclosure form with a real estate agent, attorney, or settlement agent because it is important that the terms and costs are correct including spelling of the parties’ names, loan types, amounts to close the transaction, the loan term and amount, and estimated costs for closing, payments, and insurance. If you are obtaining either a reverse mortgage, buying or selling real estate the attorneys at Smith-Weiss Shepard & Spony, P.C. can assist you in reviewing these documents to ensure your financial interests are protected.

How long before closing do you have to give closing disclosure?

In the wake of the subprime crisis, the Consumer Financial Protection Bureau requires that buyers receive the Closing Disclosure, outlining loan costs among other fees and information pertinent to the borrower, no later than 3 days before closing for review.

What is a settlement statement?

A settlement statement is an itemized list of fees and credits summarizing the finances of an entire real estate transaction. It serves as a record showing how all the money has changed hands line by line.

Is a settlement statement the same as a closing statement?

Yes, a settlement statement is the same as a closing statement, though “settlement” is the formal term most likely to be used by the real estate industry.

What is an ‘excess deposit’ at closing?

A particular line item that causes confusion on the seller’s settlement statement is the “Excess Deposit.” What is an excess deposit, and who will receive the funds listed on that line?

What does an impound account do at closing?

At closing the buyer sets up an impound account that allows them to bundle the cost of their mortgage principal, taxes, mortgage insurance, and other monthly costs into one payment. The lender likes this because they can make sure the new owner will keep up to date with all the payments associated with the home.

What information is needed to complete a closing document?

At the top of the document (before you get to the portion that looks like a spreadsheet) you’ll see a few boxes for inputting information that records basic details about the transaction, such as the names of the buyer and seller, the property address, and the closing date.

What is a seller's net sheet?

The seller’s net sheet is not an official document but an organizational worksheet that your agent will fill out to estimate how much you’ll pocket from your home sale after factoring in expenses like taxes , your real estate agent’s commission, your remaining mortgage, and escrow fees.

How does the final settlement statement differ from the closing disclosure (CD)?

The closing disclosure (CD) is a document provided by the lender to detail all the final costs associated with obtaining the mortgage loan, such as the loan terms, payment schedule, interest rate, how much buyers will pay over the life of their loan and any additional costs like points or processing fees.

After the Transaction Closes

A lot of numbers go into the closing process. The closing settlement statement is your document of truth for all the charges related to your closing. Final settlement statements can be accessed in the Modus platform, under the “Closed” tab.

What is closing disclosure?

The Closing Disclosure is a five-page form that helps you understand the key features, costs, and risks of your mortgage loan. If you applied for a loan on or after October 3, 2015, the Closing Disclosure will replace the HUD-1 Settlement Statement and Final Truth-In-Lending (TIL) forms for most mortgages.

How long before closing do you get a closing disclosure?

After you’ve shopped around for a mortgage and requested at least three Loan Estimates, compared the offers, and picked your loan, for most mortgages you’ll get a Closing Disclosure, at least three business days before closing. The Closing Disclosure is a five-page form that helps you understand ...

The History of Real Estate Settlement Procedures

HUD-1 Settlement Statement

- 1986-2015:Prior to October 2015, the Settlement Statement was known as the HUD-1, which is a standard government form issued by the Closing Agent that lists all credits, charges and home loan terms for both the buyer and the seller in all real estate transactions that required a mortgage. The charges for both the borrower and seller were listed on ...

The Current Closing Disclosure

- 2015-today: Now let’s get down to the nitty gritty on what is expected in the here and now. The Consumer Financial Protection Bureau (CFPB) took over administration from HUD and replaced the HUD-1 with the Closing Disclosurein October of 2015. It is similar to the HUD-1 in that it details the loan terms and costs, including the interest rates, closing costs, taxes, monthly payments, a…

A Couple Tips

- Take the time to read through these documents to look for mistakes, and ask your lender and Real Estate Agent to help you what you don't understand. Don’t assume that the Closing Disclosure is correct. Mistakes happen, so don’t be afraid to ask questions or seek clarification before you sign the paperwork at closing. If it is a major mistake, the buyer can obtain an explanation, and even …